The Personal Liability Umbrella: How It Protects Beyond Home and Auto

In today's unpredictable world, liability risks lurk around every corner. A simple accident can quickly escalate into a financially devastating lawsuit. While homeowners insurance and auto insurance provide essential baseline protection, their liability limits often fall short when major claims arise. This is where a personal liability umbrella policy steps in as your ultimate safety net.

Protect Your Assets Today – Get Umbrella Coverage Now!

Umbrella insurance extends coverage far beyond standard policies, safeguarding your assets, savings, and peace of mind. In this comprehensive guide, we'll explore what umbrella insurance entails, how it functions, who benefits most, and why it represents one of the smartest investments for responsible homeowners and drivers.

Understanding Umbrella Insurance: Your Extra Layer of Security

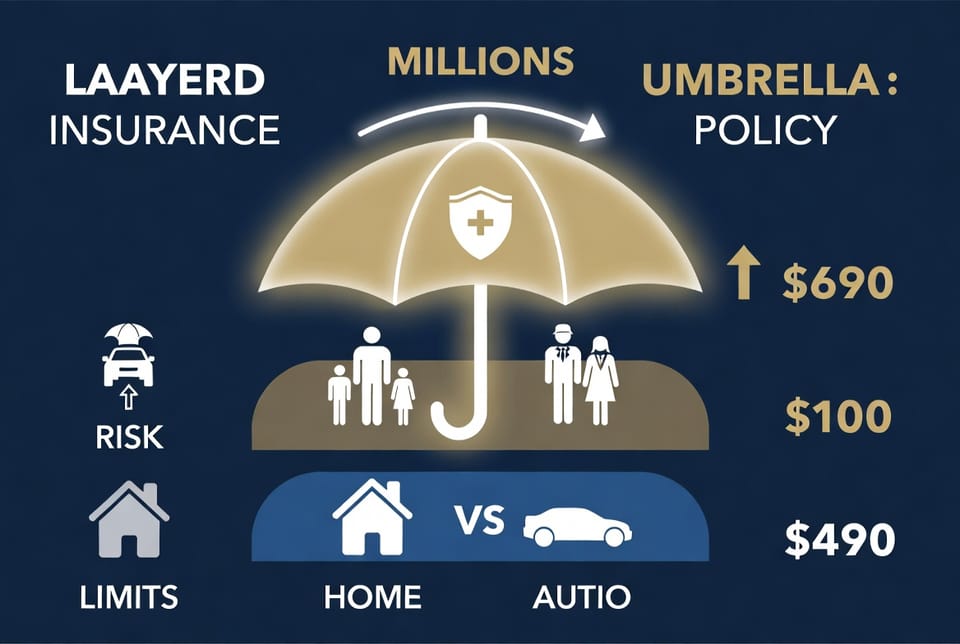

Umbrella insurance, also known as excess liability insurance, is a specialized policy that provides additional liability coverage once the limits of your underlying home, auto, or other personal policies are exhausted. It acts like an oversized umbrella, shielding you from the "rain" of high-dollar claims that could otherwise force you to liquidate assets or face wage garnishment.

Unlike primary policies, umbrella coverage is broad and flexible. It kicks in seamlessly after your base insurance pays out its maximum, covering legal defense costs, settlements, and judgments that exceed those limits.

Key features include:

- High coverage limits — Typically starting at $1 million and increasable in $1 million increments.

- Broad protection — Encompassing bodily injury, property damage, and certain personal injury claims.

- Household-wide coverage — Protecting you, your spouse, children, and sometimes other relatives living in your home.

This policy doesn't replace your home or auto insurance — it builds upon them, requiring you to maintain adequate underlying limits (often $250,000–$500,000 for auto and $300,000 for homeowners).

How Umbrella Insurance Actually Works in Practice

Imagine you're involved in a serious incident. Your auto policy has a $300,000 bodily injury limit per accident. If a judgment reaches $800,000, your insurer covers the first $300,000. Your umbrella policy then activates to handle the remaining $500,000 (assuming you have at least $1 million in umbrella coverage).

The process is straightforward:

- Underlying policies exhaust — Home or auto pays up to its limit.

- Umbrella activates — Covers excess damages, including legal fees.

- You stay protected — Assets like your home equity, retirement accounts, and future earnings remain secure.

Many policies also cover scenarios not fully addressed by standard insurance, such as libel, slander, or liability from rental properties you own personally.

Who Needs Personal Liability Umbrella Coverage?

Umbrella insurance isn't just for the wealthy — it's for anyone with assets worth protecting or a lifestyle that increases liability exposure.

Consider these common profiles:

- Homeowners with significant assets — If your net worth exceeds your policy limits, a lawsuit could target your savings or property.

- Families with high-risk features — Swimming pools, trampolines, or certain dog breeds elevate the chance of claims.

- Frequent drivers or commuters — The more time on the road, the higher the risk of multi-vehicle accidents.

- Professionals and business owners — Even if personal, activities like hosting events or traveling can lead to suits.

- Parents and pet owners — Children’s playdates or energetic dogs introduce variables outside your control.

If you have a home, vehicles, or investments to safeguard, umbrella coverage offers reassuring peace of mind at a surprisingly affordable price.

The True Cost: Affordable Protection That Pays for Itself

One of the most compelling aspects of umbrella insurance is its value. A $1 million umbrella policy typically costs between $150 and $300 per year, or roughly $12–$25 monthly. Additional millions of coverage often cost even less per unit.

This low premium provides exponential protection. Compared to the potential cost of an uncovered judgment — which can reach millions — it's one of the highest-return insurance purchases available.

Factors influencing your rate include:

- Underlying policy limits and deductibles.

- Your claims history and credit.

- Specific risks like pool ownership or dog breeds.

- Total coverage amount selected.

Many insurers bundle umbrella policies with home and auto for discounts, making it even more economical.

Real-World Scenarios Where Umbrella Insurance Saves the Day

Life's unexpected moments highlight the need for robust liability protection. Here are key examples:

- Dog Bite Lawsuits — Your friendly dog accidentally injures a visitor or neighbor. Medical bills, scarring, and emotional distress claims can exceed $500,000 quickly. Umbrella coverage handles the excess after homeowners insurance.

- Severe Car Accidents — A multi-vehicle collision with serious injuries, lost wages, and long-term care needs. If damages total $1.5 million and your auto limit is $500,000, the umbrella steps in to cover the difference, preventing personal financial ruin.

- Pool or Home Accidents — A guest slips by the pool or a child is injured during a backyard gathering. Premises liability claims often surpass standard homeowners limits, especially with medical complications.

These situations underscore a vital truth: accidents happen to responsible people. Umbrella insurance ensures you're prepared without panic.

Additional Benefits and What Umbrella Insurance Typically Covers

Beyond basic liability, many policies include:

- Defense costs — Attorney fees even if the claim is groundless.

- Personal injury — Libel, slander, wrongful eviction (in some cases).

- International incidents — Coverage while traveling abroad.

- Uninsured/underinsured motorist protection — In many policies.

It does not cover your own injuries, property damage to your belongings, or professional/business liabilities (those require separate coverage).

Always review policy details with your agent to confirm inclusions and exclusions.

Choosing the Right Coverage Amount

Experts recommend starting with at least $1 million in umbrella coverage. Higher-net-worth individuals or those with substantial risks may opt for $2–$5 million. Evaluate your total assets (home equity, investments, retirement funds) plus potential future earnings.

Pro tip: Increase underlying auto and home liability limits first to qualify for umbrella policies and maximize value.

How to Obtain and Implement Umbrella Coverage

- Review current policies — Ensure home and auto meet minimum requirements.

- Shop with trusted providers — Compare quotes from multiple insurers.

- Consult an independent agent — They can tailor recommendations to your situation.

- Bundle for savings — Combine with existing home and auto for discounts.

- Understand the fine print — Ask about claims process and any special conditions.

Implementation is simple and often takes just days. The reassurance it brings is immediate.

Common Myths About Umbrella Insurance Debunked

- "It's only for rich people" — False. Affordable premiums make it accessible for middle-class families protecting their future.

- "My standard policies are enough" — Medical costs and jury awards have risen dramatically; limits that seemed sufficient years ago often aren't today.

- "It's complicated to add" — Most insurers streamline the process, especially with existing customers.

Why Umbrella Insurance Represents Smart Financial Planning

In an era of rising litigation and healthcare costs, proactive protection is essential. An umbrella policy not only covers financial gaps but also provides authoritative peace of mind, allowing you to live confidently knowing your family's assets are secure.

By investing a modest annual premium, you protect against catastrophic losses that could derail years of hard work. It's insurance that truly works when you need it most.

Protect Your Assets Today

Don't wait for an incident to reveal the gaps in your coverage. Umbrella insurance offers essential protection beyond home and auto, fortifying your financial future against the unexpected.

Ready to explore your options? Contact our experts to review your liability limits and discuss personalized umbrella coverage.

Don’t Risk Everything – Add Umbrella Coverage Now!