The Replacement Cost vs. Market Value: What Your Home is Really Insured For

In the world of home insurance, one of the most common misconceptions can leave homeowners vulnerable at the worst possible time. Many assume their policy covers their home up to its market value — the price it might fetch if sold today. But that's not how most policies work.

Protect Your Home’s True Rebuild Cost – Call Now

Replacement cost is what your insurance truly focuses on: the amount needed to rebuild your home from the ground up if it's destroyed. This distinction matters more than ever amid rising construction costs, changing building codes, and unpredictable events like storms or fires. Understanding this difference empowers you to make informed decisions and avoid being underinsured.

This comprehensive guide clarifies the concepts, highlights real-world examples, and provides actionable steps to ensure your coverage aligns with reality. Whether you're a first-time buyer or a seasoned homeowner in the Dallas area, knowing these fundamentals can safeguard your biggest investment.

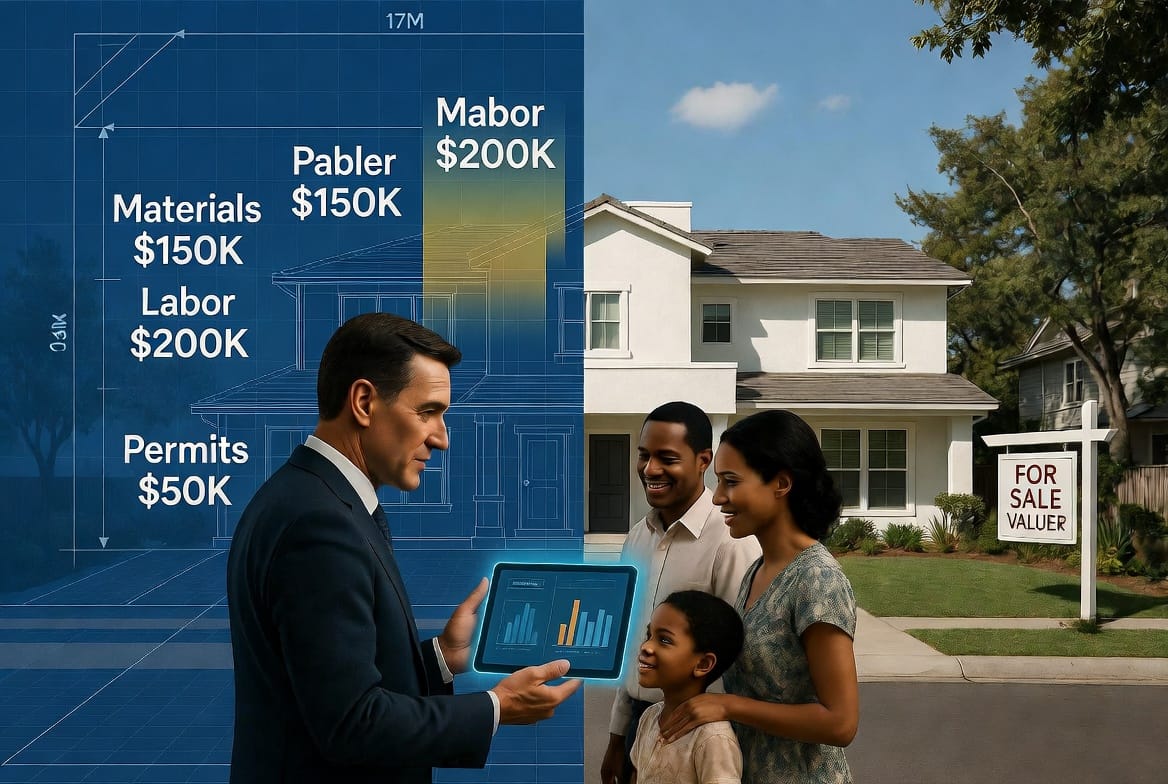

What Is Replacement Cost in Home Insurance?

Replacement cost refers to the estimated expense of reconstructing your home exactly as it was — or better — using current materials and labor rates, without factoring in the land value. It accounts for the physical structure, built-in features, and any upgrades that meet today's standards.

Insurance companies calculate this based on detailed assessments rather than real estate market trends. Why? Because after a total loss, you need funds to rebuild, not to replicate what a buyer might pay for the location.

Key components typically include:

- Square footage and layout of the home.

- Construction materials (roofing, siding, flooring, etc.).

- Labor costs in your local area.

- Current building codes and permits.

- Features like built-in appliances, plumbing, electrical systems, and architectural details.

Reassuring note: Policies offering guaranteed replacement cost or extended coverage go even further, paying whatever it takes to rebuild, even if costs exceed your policy limit — providing invaluable peace of mind.

Understanding Market Value: The Real Estate Perspective

Market value, on the other hand, represents what your property might sell for in the current real estate market. This figure includes:

- The land beneath your home.

- Location desirability (proximity to schools, jobs, amenities).

- Neighborhood appeal and comparable sales.

- Overall condition and curb appeal.

- Economic factors like interest rates and buyer demand.

A home in a prime Dallas suburb might have a high market value due to its location, but rebuilding it after a disaster wouldn't require purchasing new land. This is where confusion often arises. Homeowners seeing high appraisal values assume their insurance matches that amount — a risky assumption that can lead to significant shortfalls.

Key Differences: Replacement Cost vs. Market Value

The gap between these two values can be substantial. Consider a typical 2,500-square-foot home in suburban Dallas:

- Market Value: $450,000 (including land valued at $150,000 and strong location premiums).

- Replacement Cost: $320,000 (focused purely on rebuilding the structure with current materials and codes).

In this scenario, insurance based on market value might seem sufficient, but a claim would only cover rebuilding costs. If underinsured, you'd personally cover the difference — potentially tens or hundreds of thousands of dollars.

Real-world example: After a major hailstorm or fire, a homeowner relying on market value might discover their policy falls short by 20-40% due to surging lumber prices and updated energy-efficient building requirements. Conversely, in a declining market, market value could drop while replacement costs continue climbing.

This mismatch underscores why independent insurance reviews are essential.

Why This Distinction Matters More Than Ever

Rising inflation in the construction industry has pushed replacement costs upward significantly in recent years. Labor shortages, supply chain issues, and stricter building codes for energy efficiency and disaster resistance all contribute to higher figures.

Failing to account for these realities risks:

- Underinsurance penalties that reduce claim payouts proportionally.

- Out-of-pocket expenses during recovery that strain finances.

- Delayed rebuilding due to insufficient funds.

- Emotional stress on top of the trauma of losing your home.

On the positive side, proper replacement cost coverage ensures you can rebuild stronger and safer, incorporating modern upgrades without additional financial burden. Many policies now offer options to bridge gaps, such as inflation guard endorsements that automatically adjust coverage annually.

Factors That Influence Your Home's Replacement Cost

Several variables determine accurate replacement cost estimates. Understanding them helps you communicate effectively with your insurer.

- Square Footage and Design Complexity: Larger homes or those with custom features require more materials and specialized labor.

- Material Quality: High-end finishes, durable roofing, or eco-friendly options increase costs compared to basic builder-grade materials.

- Local Labor Rates: Areas like Dallas with strong demand for skilled trades may see elevated pricing.

- Building Codes and Permits: Newer regulations for wind resistance, flood protection, or accessibility can add substantial expenses.

- Site-Specific Considerations: Foundation type, accessibility, and local environmental factors.

- Age and Condition of the Home: Older structures may need updates to meet current codes.

How to Determine the Right Coverage for Your Home

Start with a professional replacement cost appraisal rather than relying on tax assessments or online estimators. Many insurers provide free or low-cost tools, but for precision, consult a licensed appraiser familiar with local conditions.

Steps to take:

- Gather detailed home specifications, including recent improvements.

- Request a dwelling coverage review from your agent.

- Compare quotes from multiple providers specializing in actual cash value vs. replacement cost policies.

- Consider endorsements like ordinance or law coverage for code upgrades.

- Re-evaluate annually or after major renovations.

For Dallas homeowners, factoring in regional risks like severe weather makes this process even more critical.

Common Pitfalls and How to Avoid Them

Even savvy homeowners can fall into traps:

- Assuming market value equals insurance needs.

- Neglecting to update coverage after home additions or improvements.

- Choosing the cheapest policy without reviewing limits.

- Overlooking personal property and other coverages that complement dwelling protection.

Authoritative advice: Treat your insurance as a living document. Regular reviews catch discrepancies early, offering reassurance that your family and investment remain protected.

Benefits of Proper Replacement Cost Coverage

When aligned correctly, this approach delivers:

- Financial security knowing rebuild costs are covered.

- Faster recovery with funds available when needed most.

- Enhanced home value through compliance with modern standards.

- Peace of mind for you and your loved ones.

Many policyholders who switched to adequate replacement cost protection report significant savings on premiums over time by avoiding gaps and shopping competitively.

Taking Action: Secure the Coverage Your Home Deserves

Don't leave your home's future to chance. The difference between replacement cost and market value isn't just terminology — it's the foundation of true protection.

Make sure you're insured for what it costs to rebuild. Our experienced team helps Dallas-area homeowners and beyond optimize policies for complete confidence.

Whether facing potential risks or simply seeking clarity, proactive steps today prevent costly regrets tomorrow. Your home is more than an asset — it's your sanctuary. Protect it accordingly.

Don’t Be Underinsured – Get Your Free Coverage Check