The Building Codes Upgrade Coverage: Paying for Code Changes After Loss

In the world of home insurance, unexpected events like fires, storms, or other covered perils can disrupt lives and properties. While standard policies help repair or replace damaged areas, many homeowners are surprised by additional costs when local building codes require upgrades. This is where Ordinance or Law coverage—also known as building codes upgrade coverage—steps in as a vital endorsement.

Protect Your Home from Code Upgrade Costs – Call Now!

This important add-on protects you from paying out of pocket for mandatory improvements that bring your home up to current standards. In this comprehensive guide, we'll explore how it works, what it covers, who needs it most, and why adding it to your policy brings peace of mind.

Understanding Ordinance or Law Coverage

Ordinance or Law coverage is an optional endorsement that addresses gaps in standard homeowners insurance. Local governments regularly update building codes to enhance safety, energy efficiency, accessibility, and structural integrity. These updates often mandate changes that weren't required when your home was originally built.

Standard policies typically cover repairs to restore your home to its pre-loss condition using materials of "like kind and quality." However, they exclude costs associated with complying with new ordinances or laws. Without this coverage, you could face thousands—or even tens of thousands—of dollars in unexpected expenses after a claim.

Key benefit: It reimburses the increased costs of repair, reconstruction, or demolition needed to meet current codes, up to your policy limits (often a percentage of your dwelling coverage, such as 10%, 25%, or more).

What Does Ordinance or Law Coverage Typically Include?

This endorsement is often structured in three main parts (commonly referred to as Coverages A, B, and C in policy language):

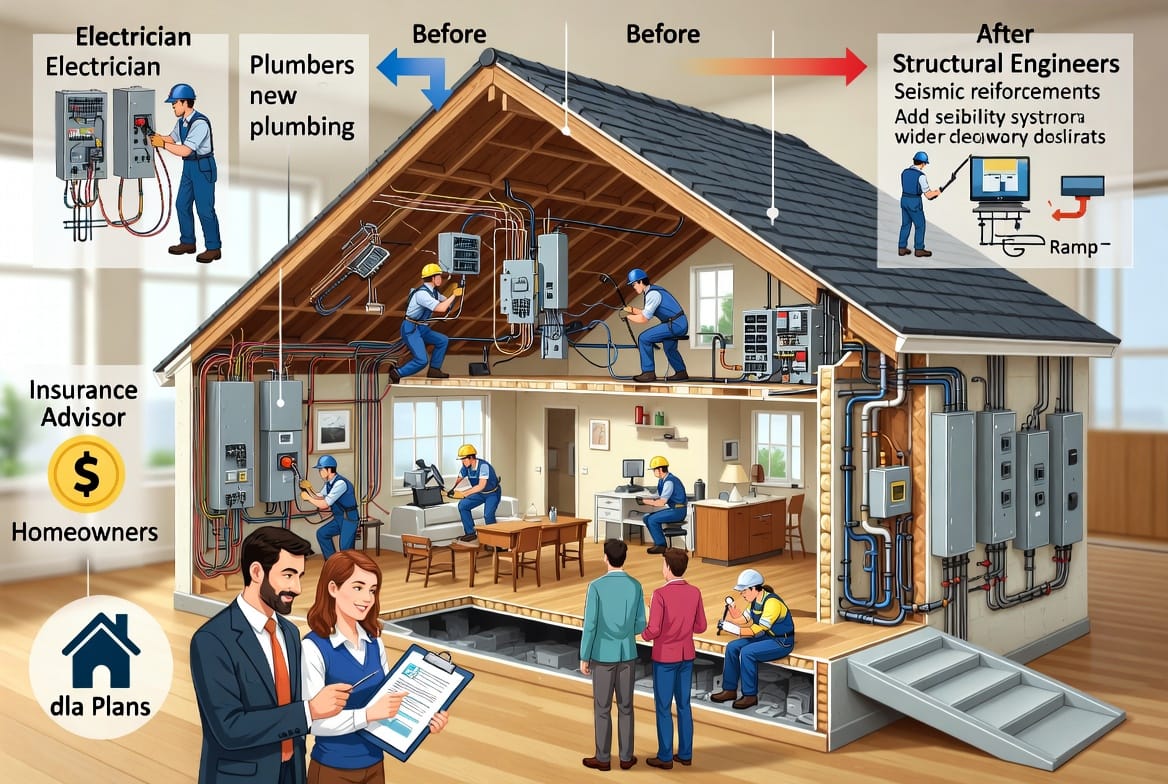

- Loss to the Undamaged Portion of the Building: Pays for demolishing or repairing parts of your home that weren't directly damaged but must be altered to comply with codes. For example, if a fire damages one wing but codes require the entire structure to meet new standards.

- Demolition and Debris Removal Costs: Covers the expense of tearing down and removing undamaged sections when required by law, plus associated cleanup.

- Increased Cost of Construction: The core protection—reimburses the extra money needed to rebuild using upgraded materials and methods that meet today's codes, such as enhanced electrical systems, energy-efficient windows, or stronger roofing.

These elements work together to ensure a full recovery without financial strain.

Common Upgrades Covered After a Loss

Building codes evolve, and post-loss repairs often trigger compliance. Here are frequent areas where Ordinance or Law coverage provides essential support:

- Electrical Systems: Upgrading outdated wiring, panels, and grounding to prevent fire hazards and meet modern safety standards.

- Plumbing and Water Systems: Installing efficient pipes, backflow prevention, or updated fixtures for better performance and code compliance.

- Structural Reinforcements: Adding features for wind, seismic, or flood resistance, depending on your location's requirements.

- Accessibility Improvements: Incorporating ramps, wider doorways, or bathroom modifications to comply with ADA-related standards or local accessibility laws.

- Energy Efficiency and Safety: New insulation, roofing materials, smoke detectors, sprinklers, or HVAC systems that align with updated environmental and fire codes.

Bold reminder: These upgrades enhance your home's safety and value long-term, but they can significantly inflate repair bills without proper coverage.

Who Needs Building Codes Upgrade Coverage Most?

This endorsement is particularly valuable for:

- Owners of Older Homes: Properties built decades ago often fall short of today's codes. A major loss can force extensive (and expensive) modernization.

- Homes in Areas with Strict or Evolving Codes: Regions with frequent updates due to weather risks (hurricanes, earthquakes), urban density, or environmental priorities.

- Properties Undergoing Major Renovations: Any significant work can trigger code compliance for the entire structure.

- Families Prioritizing Long-Term Security: Ensuring your home is rebuilt safer protects your loved ones and investment.

Even newer homes may need it if local ordinances have tightened since construction. Review your policy declarations page—many include limited automatic coverage (e.g., 10% of dwelling), but full protection often requires a higher limit endorsement.

Real-World Scenarios: When Coverage Makes a Difference

Imagine a fierce storm damages your roof and siding. Your insurer pays to replace like-for-like, but inspectors require upgraded wind-resistant materials and reinforced framing per new codes. Without Ordinance or Law, those extras come from your pocket.

Or consider a kitchen fire in an older home: Partial damage leads to full electrical and plumbing overhauls. The difference? Potentially $20,000–$50,000+ in upgrades, depending on scope and location.

These situations highlight why proactive policy review is crucial. Don't assume standard coverage suffices—code compliance is mandatory, not optional.

How to Determine Your Coverage Needs

- Assess Your Home's Age and Condition: Older properties or those with outdated systems warrant stronger consideration.

- Check Local Building Codes: Research your municipality's requirements for repairs and reconstructions.

- Review Your Current Policy: Look for existing Ordinance or Law limits and discuss increases with your agent.

- Consult Professionals: Insurance agents and contractors can provide estimates on potential upgrade costs.

- Calculate Potential Exposure: Factor in your home's replacement cost and local code stringency.

Adding this coverage is typically affordable relative to the protection it offers. Premiums vary by location, home value, and chosen limits, but the security is invaluable.

Potential Limitations and Important Considerations

While powerful, Ordinance or Law coverage has boundaries:

- It applies only after a covered peril causes the initial damage.

- Limits are usually a percentage of your dwelling coverage—ensure it's sufficient for your area.

- It may not cover upgrades unrelated to the loss or certain pollutants/contamination scenarios.

- Always verify exact terms, as policy language varies by insurer.

Pro tip: Pair it with accurate dwelling coverage valuation to avoid underinsurance overall.

The Reassuring Path Forward: Protect Your Investment

Rebuilding after a loss is stressful enough without hidden code-related costs. Ordinance or Law coverage empowers you to restore your home to a safer, more resilient standard—aligning with modern living while safeguarding your family's future.

By understanding and securing this endorsement, you transform potential financial pitfalls into manageable steps toward recovery. Homeownership involves risks, but informed choices minimize them.

Take the time today to evaluate your policy. A quick conversation with your insurance professional can reveal if you're adequately protected against building code surprises.

Don't pay for code upgrades out of pocket. Our team is ready to help tailor a policy that gives you confidence in any scenario.

Upgrade Your Coverage for Building Code Changes – Call Today