The Windstorm Deductible: Percentage vs. Dollar Amount Explained

Windstorms can strike with little warning, leaving homeowners facing significant repairs and tough financial decisions. Understanding your windstorm deductible is one of the most important steps in protecting your property and your peace of mind. Many homeowners are surprised to learn that their windstorm coverage often comes with a percentage-based deductible rather than a simple flat dollar amount.

Understand Your Windstorm Deductible – Call Now!

This comprehensive guide explains exactly how windstorm deductibles work, the critical differences between percentage and dollar-amount options, real-world examples, and practical steps to manage this key policy feature. Being informed helps you avoid unexpected out-of-pocket costs when storms hit.

What Is a Windstorm Deductible?

A windstorm deductible is the amount you must pay out of pocket before your homeowners insurance begins covering damage from high winds, hurricanes, tornadoes, or related events. Unlike standard deductibles that apply to many types of claims, windstorm deductibles are often separate and can be substantially higher.

Insurers use these deductibles to share risk with policyholders, especially in areas prone to severe weather. This approach keeps premiums more affordable while encouraging homeowners to prepare their properties.

Key risks if you overlook this detail: You could face thousands of dollars in unexpected expenses right when your home needs repairs the most.

Percentage Deductibles vs. Dollar-Amount Deductibles

The main distinction lies in how the deductible is calculated:

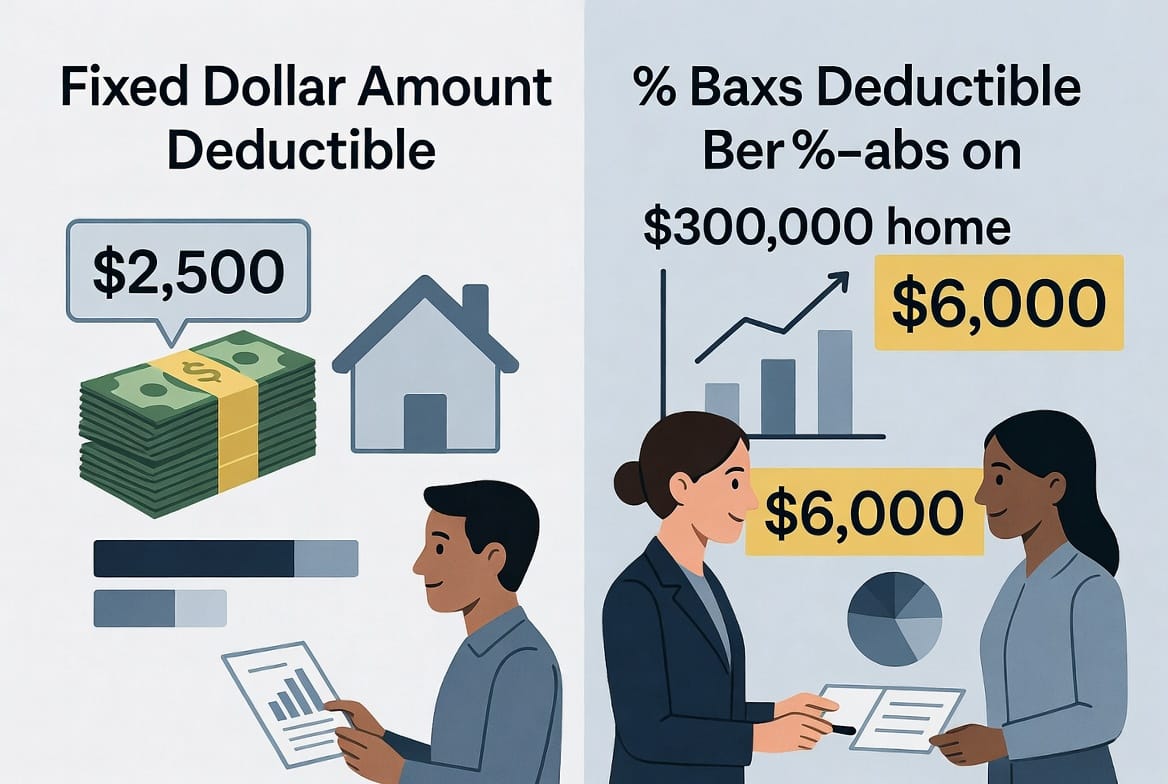

- Dollar-amount deductible: A fixed sum, such as $1,000 or $2,500, that you pay regardless of your home’s value.

- Percentage deductible: A percentage of your home’s insured value (replacement cost), commonly ranging from 1% to 5%.

Percentage deductibles are more common in wind-prone regions. For example, a 2% deductible on a $300,000 home equals $6,000 out of pocket before insurance kicks in. A 5% deductible on the same home would require $15,000.

Why the difference matters: A percentage deductible scales with your property value. While it may seem high initially, it provides clarity in high-value homes and helps insurers manage catastrophic losses from widespread storms.

Many policies allow you to choose between options at purchase or renewal, often with premium adjustments. Selecting the right one depends on your budget, risk tolerance, and local weather patterns.

How Percentage Windstorm Deductibles Are Calculated

Calculation is straightforward but requires knowing your home’s insured value:

- Determine your dwelling coverage amount (insured replacement cost of the structure).

- Apply the percentage stated in your policy.

- Pay that amount for eligible windstorm claims.

Example:

Your home is insured for $400,000 with a 2% windstorm deductible.

Calculation: 2% of $400,000 = $8,000.

You pay the first $8,000 of repairs; the insurer covers the rest (minus any other applicable deductibles or limits).

Important note: This applies per occurrence. If you have multiple claims in one event, the deductible typically applies only once.

Factors that influence your specific rate include:

- Location — Coastal or tornado alley areas often require higher percentages.

- Construction quality — Impact-resistant roofing or fortified homes may qualify for lower percentages.

- Insurer policies — Some companies offer “buy-down” options to reduce the percentage for an additional premium.

Real-World Scenarios and Financial Impact

Consider these practical examples:

- Scenario 1: Moderate Wind Damage

A $300,000 home with a 3% deductible suffers $12,000 in roof and siding damage.

Out-of-pocket: $9,000 (3% = $9,000). Insurance pays $3,000. - Scenario 2: Major Storm

Same home, $80,000 in total damage from a hurricane.

Out-of-pocket: Still only $9,000. Insurance covers $71,000. - Scenario 3: Dollar vs. Percentage

A $500,000 home with a $2,500 flat deductible vs. 2% ($10,000). The flat option saves money on smaller claims but may cost more in premiums.

These examples highlight why understanding your deductible provides reassurance. It prevents sticker shock and allows better financial planning, such as setting aside an emergency fund.

Bullet-point advantages of knowing your deductible:

- Enables accurate budgeting for potential repairs.

- Helps compare policies effectively during shopping.

- Supports decisions on home fortifications that may lower your percentage.

- Reduces stress during claims by setting clear expectations.

States Where Percentage Deductibles Are Common

Percentage-based windstorm deductibles appear most frequently in states vulnerable to hurricanes and severe thunderstorms.

Common states include coastal areas in the Southeast, Gulf Coast, and parts of the Midwest and Plains states. Homeowners in these regions should review policies carefully, as regulations and standard practices vary.

Even in lower-risk states, carriers may apply percentage deductibles for specific wind or hail coverage. Always check your declarations page.

Benefits and Potential Drawbacks of Percentage Deductibles

Reassuring perspective: Percentage deductibles help stabilize the insurance market by distributing costs of large-scale events. This often results in more available coverage and potentially lower base premiums.

Benefits:

- Predictable scaling with home value.

- Incentivizes mitigation — Stronger homes may qualify for reductions.

- Catastrophic protection — Insurance steps in meaningfully after the initial share.

Drawbacks to consider:

- Higher upfront costs for some claims.

- Complexity in understanding exact exposure.

- Potential impact on cash flow after a storm.

The authoritative approach is proactive preparation. Many homeowners successfully manage these deductibles through smart planning.

Strategies to Manage and Reduce Your Windstorm Deductible Exposure

Here are proven steps:

- Review your policy annually — Confirm the exact percentage and insured value.

- Consider deductible buy-down options — Pay a bit more premium for a lower percentage.

- Fortify your home — Install impact windows, reinforced roofing, or storm shutters to potentially qualify for discounts.

- Build an emergency savings fund — Aim to cover at least your full deductible amount.

- Shop and compare — Get quotes from multiple insurers, paying close attention to windstorm terms.

- Document your property — Maintain updated photos and inventory for faster claims.

- Consult professionals — Work with independent agents who understand local risks.

These actions empower you to face storms with confidence.

Preparing Your Home and Finances for Wind Events

Beyond the deductible, focus on prevention. Secure outdoor items, trim trees, and reinforce weak points. Consider separate windstorm or hurricane policies if your standard homeowners coverage has limitations.

Financial preparedness includes reviewing flood insurance separately, as windstorm policies typically exclude flooding. Layering appropriate coverages creates comprehensive protection.

Common Questions About Windstorm Deductibles

Does my standard deductible apply alongside the windstorm one?

Usually not — the windstorm deductible replaces the standard one for those claims.

Can I change my deductible?

Yes, typically at renewal or by endorsing your policy. Discuss options with your agent.

How does home value affect the percentage?

Higher insured values mean higher absolute deductible amounts. Keep your coverage limits updated to avoid underinsurance.

Will filing a claim raise my premiums?

It depends on the insurer and claim history, but proper preparation minimizes the need for frequent claims.

Take Control of Your Home Insurance Today

Knowledge truly is power when it comes to protecting your largest investment. By fully understanding the windstorm deductible—whether percentage or dollar amount—you position yourself to respond effectively if severe weather occurs.

Don’t wait for the next storm to discover gaps in your coverage.

Know your wind deductible before the storm.

Our experienced team helps homeowners across high-risk areas optimize their insurance, reduce unnecessary expenses, and gain confidence in their protection. Schedule your review now and build a stronger, more resilient plan for your home and family.

Protect Your Home & Wallet – Schedule Policy Review