The Home Inspector Report: What Insurers Look For in Your Pre-Purchase Inspection

Buying a home is one of the most significant investments you'll make. A pre-purchase home inspection serves as your essential safeguard, providing a clear picture of the property's true condition. Insurers pay close attention to these reports during underwriting because they directly impact risk assessment and coverage eligibility. Understanding what insurers look for helps you navigate the process smoothly and secure the right home insurance protection.

Get Insured After Your Home Inspection – Call Now!

This comprehensive guide explains the underwriting relevance of inspection reports, highlights common red flags, and offers practical steps to address findings before binding coverage. With the right preparation, you can move forward confidently.

The Role of Pre-Purchase Inspections in Home Insurance

A professional home inspection evaluates the structural integrity, systems, and overall condition of a property. Insurers request inspection reports to verify that the home meets their underwriting standards and to identify potential hazards that could lead to claims.

Underwriting relevance is straightforward: insurers use the report to quantify risk. A clean inspection supports standard premiums and broad coverage. Issues flagged in the report may result in higher deductibles, exclusions, or even declination of coverage until resolved.

Many insurance carriers require a copy of the inspection report as part of the application process, especially for older homes or properties with visible maintenance concerns. This practice protects both the insurer and the homeowner by ensuring known risks are managed proactively.

What Insurers Scrutinize in Inspection Reports

Insurers focus on items that pose significant liability or repair costs. Here are the primary areas they evaluate:

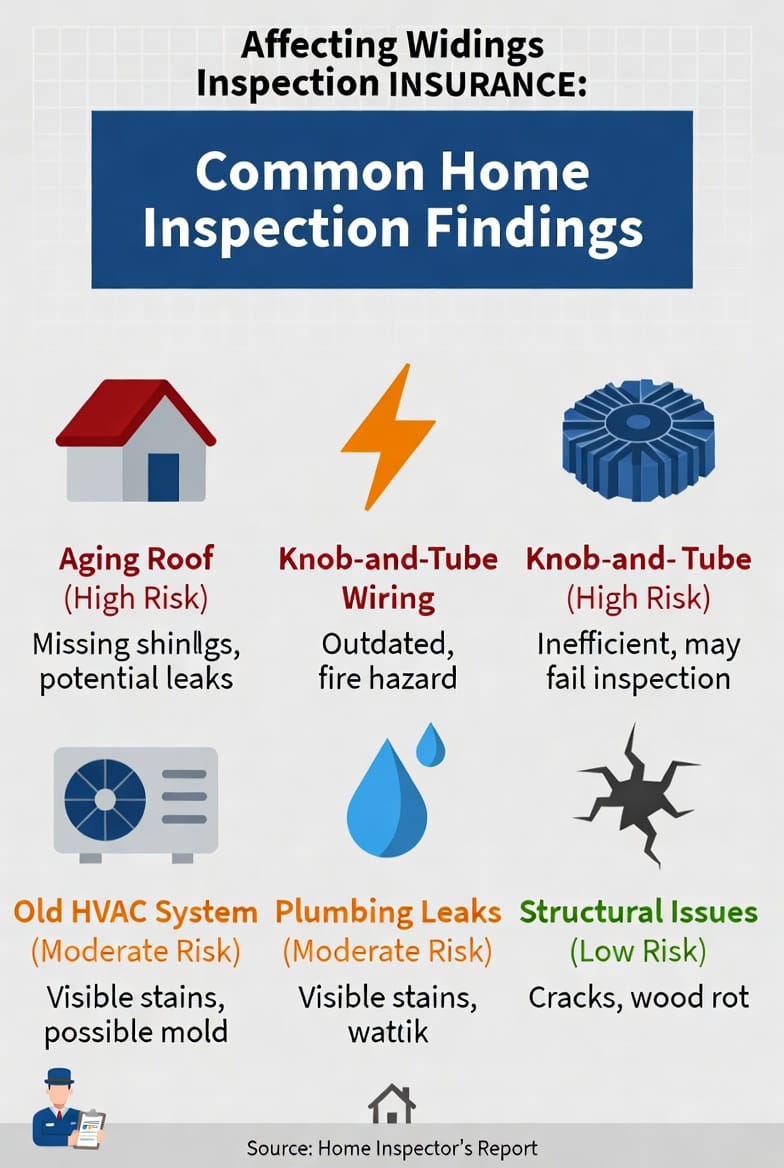

Roof Condition and Longevity

The roof is one of the most critical components. Insurers often flag roofs older than 20 years, as they are more prone to leaks and storm damage.

- Signs of concern: Missing shingles, sagging areas, or previous patch repairs.

- Impact: May lead to limited wind/hail coverage or required replacement before binding.

Pro tip: Address roof issues early. A newer roof or professional certification of good condition can satisfy underwriters.

Electrical Systems

Outdated or unsafe electrical work raises major red flags. Knob-and-tube wiring, aluminum wiring, or overloaded panels are frequent concerns.

- Why it matters: These systems increase fire risk and may not support modern appliances.

- Common findings: Unpermitted modifications or exposed wiring.

Insurers may require an electrician’s evaluation or upgrades before approving coverage.

HVAC Systems

Outdated HVAC units (typically 15+ years old) often trigger underwriting questions. Leaks, poor ventilation, or inefficient systems can lead to mold or energy-related issues.

- What insurers check: Age, maintenance records, and signs of deterioration.

- Resolution path: Professional servicing or replacement documentation.

Plumbing and Water-Related Issues

Plumbing leaks, polybutylene pipes, or galvanized systems can signal future water damage claims.

- Red flags: Evidence of past leaks, poor drainage, or outdated materials.

- Risk level: High, as water damage is one of the most common insurance claims.

Structural Integrity and Wood Rot

Wood rot, foundation cracks, or termite damage directly affect habitability and long-term stability.

- Insurers look for: Visible rot in crawl spaces, siding, or framing.

- Additional concerns: Settling, improper grading, or moisture intrusion.

Addressing findings such as these before closing or binding coverage demonstrates responsible ownership and strengthens your insurance application.

How to Address Inspection Findings Effectively

Discovering issues in a home inspection report doesn’t have to derail your purchase. Here’s a step-by-step approach:

- Review the Report Thoroughly – Work with your inspector to understand the severity of each item. Distinguish between cosmetic concerns and major defects.

- Negotiate with the Seller – Use the report to request repairs, credits, or price reductions. Focus on items that impact insurability.

- Obtain Specialist Evaluations – For electrical, roofing, or structural issues, hire licensed professionals for detailed assessments and quotes.

- Document Repairs – Keep invoices, permits, and before-and-after photos. This evidence reassures underwriters that risks have been mitigated.

- Consider Insurance-Friendly Upgrades – Prioritize updates that align with carrier preferences, such as modern electrical panels or high-efficiency HVAC systems.

Many buyers successfully resolve concerns and secure favorable coverage. Acting promptly turns potential obstacles into opportunities for a safer, better-protected home.

The Underwriting Process: From Inspection to Coverage

Once you submit the inspection report, underwriters analyze it alongside other application details. They assess:

- Overall risk profile of the property.

- Potential for large claims based on flagged conditions.

- Compliance with building codes and safety standards.

Reassuring note: Most issues are fixable. Transparent communication with your insurance agent helps identify solutions that satisfy both parties.

Some carriers offer home insurance endorsements or adjustments once repairs are complete. Others may bind coverage with temporary higher deductibles for specific risks, transitioning to standard terms later.

Additional Factors Insurers Consider

Beyond major systems, underwriters review:

- Foundation and basement conditions – Moisture, cracks, or flooding history.

- Attic and insulation – Ventilation problems or outdated materials.

- Exterior elements – Siding, windows, and drainage systems.

- Safety features – Smoke detectors, carbon monoxide alarms, and security measures.

Proactive maintenance in these areas enhances insurability and may even qualify you for discounts on premiums.

Tips for Homebuyers to Streamline Insurance Approval

- Choose an experienced inspector familiar with insurance requirements.

- Share the report early with your insurance agent for preliminary feedback.

- Budget for potential repairs as part of your overall homeownership plan.

- Maintain detailed records of all improvements.

- Shop multiple carriers if one is overly restrictive — options exist for various property conditions.

A well-prepared approach minimizes surprises and positions you for competitive home insurance rates.

Protecting Your Investment Long-Term

Understanding what insurers look for in a pre-purchase home inspection empowers you to make informed decisions. By addressing red flags such as an old roof, knob-and-tube wiring, outdated HVAC, wood rot, and other concerns, you not only secure coverage but also enhance the safety and value of your home.

The inspection process, while detailed, ultimately provides peace of mind. With proper attention to findings, most buyers obtain the protection they need without significant delays.

Know what insurers want to see. Our team is ready to review your inspection report and tailor a home insurance policy that fits your needs.

Expert Help with Insurance After Home Inspection – Call Today