The Umbrella Policy: Why an Extra Million in Liability Coverage is a Smart Investment for Modern Life

In today's fast-paced world, where accidents can happen in the blink of an eye, protecting your assets and future has never been more crucial. Umbrella insurance emerges as a powerful safeguard, offering an extra million in liability coverage that extends beyond the limits of your standard home, auto, or personal policies. This article explores why investing in an umbrella policy is not just wise but essential for modern households. We'll break down how standard liability limits can fall short, what umbrella policies cover, their affordability, and the prerequisites for obtaining one. Rest assured, with the right coverage, you can navigate life's uncertainties with confidence.

Don’t Risk Everything – Add Umbrella Insurance Now

Understanding Standard Liability Limits: Why They're Often Not Enough

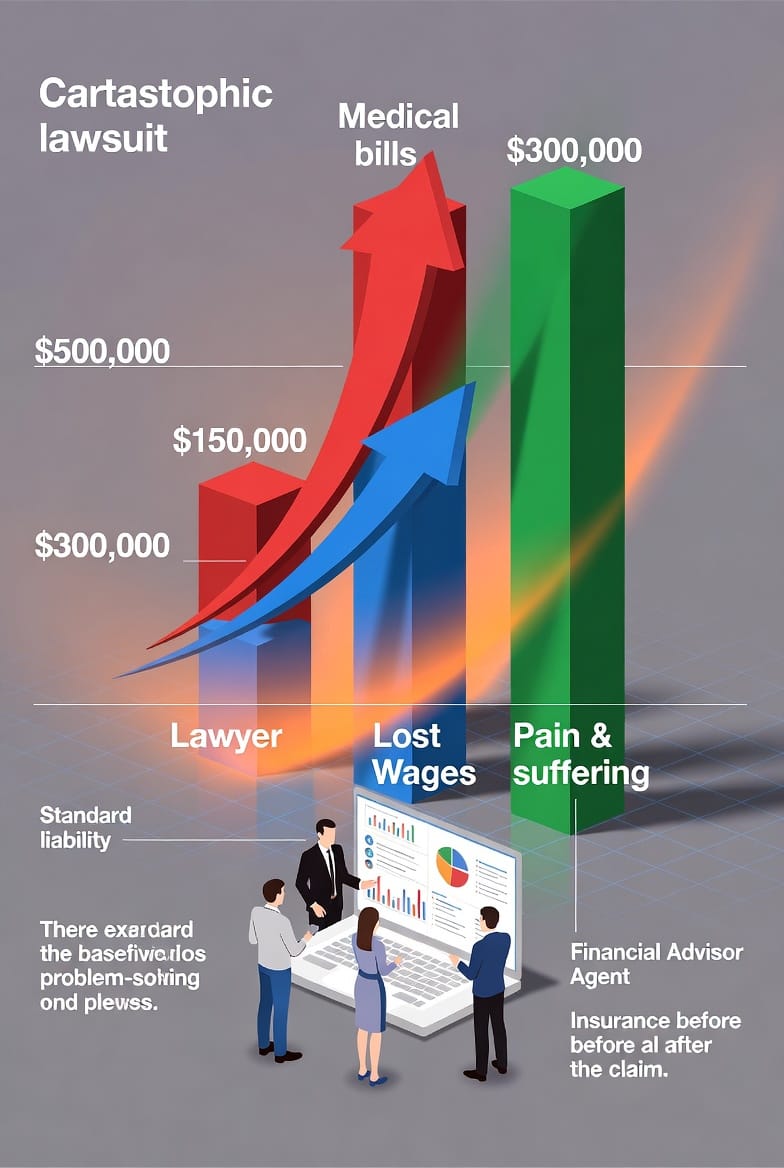

Most homeowners and auto insurance policies come with liability limits ranging from $300,000 to $500,000. These figures might seem substantial at first glance, but in the event of a serious accident or lawsuit, they can be depleted astonishingly quickly. Consider a scenario where a guest slips and falls at your home, sustaining severe injuries. Medical bills alone could soar into the hundreds of thousands, not to mention lost wages, rehabilitation costs, and compensation for pain and suffering.

- Medical Expenses: Emergency care, surgeries, and ongoing therapy can easily exceed $200,000 for a single incident.

- Lost Income: If the injured party is unable to work, claims for future earnings could add another $100,000 or more.

- Legal Fees and Settlements: Court battles often push totals over $500,000, leaving you personally liable for the remainder.

The reality is stark: according to industry data, the average cost of a bodily injury claim has risen by over 20% in the last decade due to increasing healthcare costs and more aggressive litigation. Without additional protection, a single mishap could jeopardize your savings, home, or even retirement funds. But here's the reassuring part – umbrella policies step in precisely where standard coverage ends, providing that vital buffer.

The Broad Protection of Umbrella Insurance: What It Covers

Umbrella insurance acts as a comprehensive overlay, kicking in after your primary policies' limits are exhausted. It's designed to cover a wide array of liabilities, making it indispensable for anyone with assets to protect. Here's a closer look at its key coverages:

Auto-Related Liabilities

Driving incidents are among the most common triggers for large claims. If you're at fault in a multi-vehicle accident causing significant injuries, your auto policy's liability might cap at $300,000 per person. An umbrella policy extends this, covering excess damages up to $1 million or more. This includes property damage, legal defense, and even incidents involving uninsured motorists in some cases.

Home and Property Risks

Your home is your sanctuary, but it also harbors potential liabilities. From dog bites to swimming pool accidents, personal injury claims can escalate rapidly. Umbrella coverage protects against lawsuits related to slander, libel, or invasion of privacy – scenarios increasingly relevant in our digital age. For instance, if a neighbor sues over a social media post you made, your policy could handle the fallout.

Personal Injury and Beyond

Beyond physical spaces, umbrella policies often cover personal liabilities like false arrest or defamation. They're particularly valuable for families with recreational vehicles, boats, or rental properties, where standard policies might not suffice.

In essence, this extra layer ensures that one unfortunate event doesn't unravel your financial stability. It's like having a safety net that catches you when primary ropes fray.

The Cost-Effectiveness of Umbrella Policies: High Value at Low Premiums

One of the most compelling arguments for umbrella insurance is its affordability. For an additional $1 million in coverage, premiums typically range from $150 to $300 annually – a fraction of what you'd pay for equivalent increases in primary policies. Why so reasonable? Because umbrella policies only activate after underlying limits are met, reducing the insurer's risk.

Factors influencing cost include:

- Your Assets and Lifestyle: Higher net worth or ownership of high-risk items (like pools or trampolines) may slightly increase premiums.

- Location and History: Urban areas with higher litigation rates or a clean claims record can affect rates.

- Coverage Amount: Starting at $1 million, you can scale up to $5 million or more for added peace of mind.

Compared to the potential financial ruin of a lawsuit – where judgments can reach millions – this investment yields tremendous returns. Many policyholders find that bundling with existing providers further lowers costs, making it a seamless addition to your insurance portfolio.

Prerequisites for Purchasing an Umbrella Policy: Building on Solid Foundations

To qualify for an umbrella policy, insurers require robust underlying coverage. This ensures the primary policies handle initial claims, allowing the umbrella to focus on excesses. Common requirements include:

- Auto Insurance: At least $250,000 per person/$500,000 per accident in bodily injury liability, plus $100,000 in property damage.

- Homeowners Insurance: Minimum $300,000 in personal liability coverage.

- Other Policies: For boats or rentals, similar elevated limits apply.

Meeting these isn't burdensome; most standard policies can be adjusted affordably. Once in place, your umbrella policy integrates smoothly, often from the same insurer for streamlined claims processing. It's a strategic step that fortifies your overall protection strategy.

Who Benefits Most from Umbrella Insurance?

While everyone with assets should consider it, certain groups stand out:

- Homeowners with Pools or Trampolines: Increased exposure to accidents.

- Families with Teenage Drivers: Higher risk of auto incidents.

- Professionals and Business Owners: Protection against personal liabilities spilling into work.

- High-Net-Worth Individuals: Safeguarding substantial savings and investments.

Rest easy knowing that umbrella insurance isn't reserved for the ultra-wealthy; it's a practical choice for middle-class families aiming to preserve their hard-earned progress.

Common Exclusions: What Umbrella Policies Don't Cover

To set realistic expectations, note that umbrella policies have limitations:

- Intentional Acts: Coverage excludes deliberate harm or criminal behavior.

- Business Liabilities: Professional errors typically require separate commercial policies.

- Certain Properties: Owned aircraft or specific high-risk activities might need endorsements.

Always review your policy details with an agent to ensure comprehensive alignment.

The Peace of Mind Factor: Long-Term Security in an Unpredictable World

In an era of rising lawsuits and unpredictable events, umbrella insurance offers more than financial protection – it delivers peace of mind. Imagine facing a major claim without dipping into personal assets; that's the reassurance it provides. Studies show that insured individuals report lower stress levels during crises, allowing focus on recovery rather than finances.

Integrating an umbrella policy is straightforward and proactive. It's an investment in your family's future, shielding against the "what-ifs" that modern life throws our way.

Final Thoughts: Take Action Today

Don't let a single oversight define your financial trajectory. Umbrella insurance is your ally in building a resilient safety net. With its extensive coverage, low cost, and easy integration, it's a smart move for anyone serious about asset protection.

Protect Your Assets from Lawsuit Surprises – Call Today