The Stored Vehicle Coverage: Reducing Insurance on a Car in Storage

In an era where every expense matters, stored vehicle coverage stands out as a smart, legitimate way to reduce insurance on a car in storage without sacrificing essential protection. If your vehicle sits idle for months—whether it’s a seasonal car used only for summer adventures or a college student’s vehicle parked during the academic year—standard full-coverage premiums can quietly drain your budget.

educe Your Car Insurance Today – Call Now!

Stored vehicle coverage lets you temporarily scale back to comprehensive coverage only, eliminating unnecessary liability insurance while your car remains safely off the road. This money-saving option is designed precisely for situations where the vehicle poses no risk to other drivers or public roads.

Rest assured, this adjustment is fully supported by most insurers when proper storage conditions are met. You maintain peace of mind against theft, fire, vandalism, and other non-collision perils, yet you stop paying for liability you simply don’t need.

This authoritative guide explains exactly how stored vehicle coverage works, who benefits most, the strict requirements you must follow, and the simple steps to switch coverage and reactivate it later. By the end, you’ll understand how to confidently reduce insurance on a car in storage while keeping your asset fully protected.

Understanding Stored Vehicle Coverage

Stored vehicle coverage is a specialized insurance endorsement that recognizes your car is not being driven. Instead of a full policy that includes both liability coverage (protecting you if you cause an accident) and comprehensive coverage (protecting against theft, fire, hail, vandalism, and falling objects), you reduce to comprehensive only.

Liability insurance becomes irrelevant when the vehicle is stored because it cannot be operated on public roads. Insurers acknowledge this reality and offer substantial premium reductions—often 40-60% depending on your location, vehicle value, and driving history.

The coverage remains active for the perils that could still affect a parked car. Comprehensive coverage continues to guard against garage fires, break-ins, or severe weather events. This balance delivers real value: you pay only for risks that actually exist.

Many policyholders are surprised to learn this option has been available for years. It is not a loophole but a standard, responsible feature insurers provide to responsible owners who store vehicles properly. With stored vehicle coverage, you avoid overpaying for protection you cannot possibly use.

Who Benefits Most from This Money-Saving Option

Two groups benefit enormously: owners of seasonal cars and families with college students.

Seasonal vehicles—classic convertibles, boats-on-trailers, or winter-only SUVs—spend months in storage between uses. Paying full premiums year-round for a car that never leaves the garage is simply unnecessary. Stored vehicle coverage slashes costs during downtime while keeping the car insured against the threats it actually faces.

College students often leave cars at home during the school year. Parents face the same dilemma: full coverage on a vehicle sitting idle for eight or nine months. By switching to storage coverage, families can redirect hundreds of dollars toward tuition, books, or living expenses.

Other beneficiaries include military families with overseas deployments, snowbirds who winter in warmer climates, and anyone who travels extensively for work. In each case, the car remains secure and protected, but liability exposure disappears.

The reassurance is real: your insurer understands your situation and rewards responsible behavior with lower rates. No more wasting money on coverage you cannot use.

Requirements for Qualifying for Stored Vehicle Coverage

Insurers maintain clear, non-negotiable requirements to prevent misuse. Meeting these ensures your policy remains valid and your savings legitimate.

- The vehicle must be off public roads at all times—no occasional drives to the store or quick errands.

- It must be stored in a secure garage or fully enclosed private structure, not a driveway or open carport.

- The garage must have a locking door and, ideally, an alarm or security system.

- You must retain comprehensive coverage—liability can be suspended, but protection against theft and fire stays in place.

- The storage period is typically a minimum of 30 consecutive days; some insurers require 60 days.

- You must notify your insurer in writing before the storage period begins and provide proof of storage location.

Bold risk alert: Failing to meet these conditions can void the storage endorsement and leave you exposed in the event of a claim. Always document everything—photographs of the garaged vehicle, dated correspondence with your insurer, and mileage verification if requested.

These rules exist for your protection and the insurer’s. When followed precisely, they deliver worry-free savings.

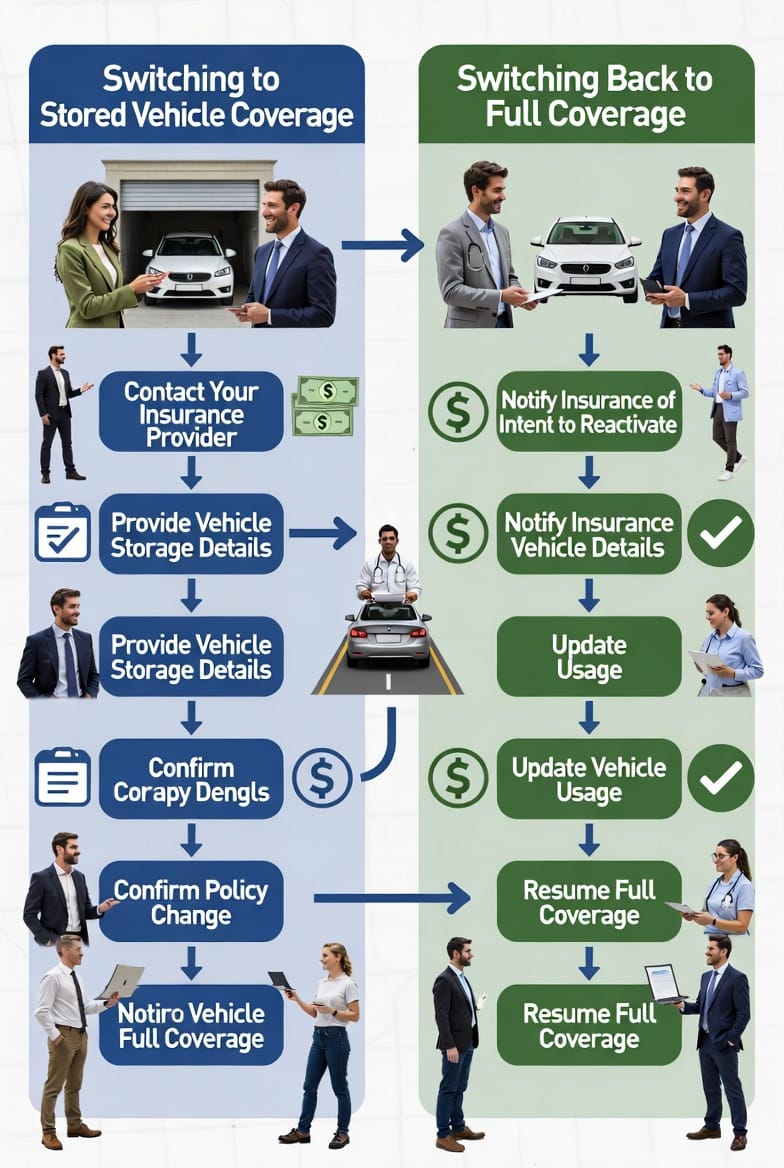

Step-by-Step Guide to Switching to Stored Vehicle Coverage

Making the change is straightforward and can be completed in a single phone call or online portal session.

- Review your current policy – Confirm the vehicle qualifies and note your current premium breakdown.

- Contact your insurer – Explain that the vehicle will be stored off public roads in a secure garage for an extended period.

- Request the stored vehicle endorsement – Ask specifically to suspend liability coverage while retaining comprehensive coverage.

- Provide required documentation – Submit photos of the garage, the covered vehicle, and proof of ownership.

- Receive confirmation – Your insurer will issue an amended declarations page showing the reduced premium.

- Plan reactivation – Note the exact date you intend to return the car to the road so you can schedule reinstatement.

The entire process usually takes less than 48 hours. Most insurers handle these requests routinely and appreciate proactive customers who manage risk responsibly.

Pro tip: Keep a digital folder with all storage-related documents. This simple habit prevents any future disputes and ensures smooth reinstatement when the time comes.

Calculating Your Potential Savings

Savings vary by state, vehicle value, and insurer, yet the numbers are consistently impressive. A typical mid-range sedan with full coverage at $1,800 annually can drop to approximately $800–$1,000 under stored vehicle coverage. That’s a monthly reduction of $65–$80—real money that accumulates quickly over six months.

Luxury or classic cars see even larger absolute savings because their comprehensive premiums are higher to begin with. College-student families often report saving $400–$700 per semester.

These reductions are not temporary discounts; they reflect actual risk elimination. You are not losing protection—you are aligning coverage with reality.

Track your savings by comparing the new declarations page with the old one. Many policyholders are astonished at how much they were previously overpaying for unused liability.

Storage Best Practices and Key Considerations

Proper storage is more than parking the car and walking away. Follow these practices to maximize safety and maintain eligibility for stored vehicle coverage.

- Use a high-quality breathable car cover to protect against dust and minor moisture.

- Disconnect the battery or use a trickle charger to prevent drain.

- Inflate tires to manufacturer specifications and consider tire cradles to avoid flat spots.

- Remove valuables and keep the fuel tank at half capacity to reduce condensation.

- Schedule periodic visual inspections—every 30 days is ideal.

- Install motion-sensor lighting or a basic security camera for added peace of mind.

Reinstating Full Coverage When You’re Ready to Drive Again

Reactivation is just as simple as the initial switch. Contact your insurer 7–14 days before you plan to drive the vehicle. Provide the new mileage reading and confirm the car has been removed from storage. The liability coverage is reinstated immediately, often without additional underwriting.

Keep records of the reactivation date. This ensures continuous protection the moment the car returns to public roads. Most insurers allow seamless transitions with no lapse in coverage when you follow the notification process.

Common Myths About Stored Vehicle Coverage

Myth 1: “My car is safe in the driveway, so I don’t need a garage.”

Reality: Insurers require a fully enclosed structure. Driveway storage does not qualify.

Myth 2: “I can occasionally drive the car and still keep storage rates.”

Reality: Any operation on public roads voids the endorsement and may trigger a claim denial.

Myth 3: “Comprehensive isn’t necessary if the car is garaged.”

Reality: Theft and fire remain real threats. Dropping comprehensive entirely creates dangerous gaps.

Myth 4: “Switching is complicated and time-consuming.”

Reality: The process is quick, paper-light, and customer-friendly.

Clearing these misconceptions empowers you to make informed decisions with confidence.

Final Advice: Stop Overpaying Today

Don’t pay for liability on a stored car. When your vehicle is safely tucked away in a secure garage and off public roads, stored vehicle coverage delivers legitimate savings without compromising protection.

You retain comprehensive coverage for the risks that still matter—theft, fire, vandalism—while eliminating the expense of unused liability. Seasonal car owners, college student families, and anyone with an idle vehicle deserve this smart financial choice.

Take action today. Review your policy, confirm your storage meets every requirement, and contact your insurance provider to activate stored vehicle coverage.

Your car stays protected. Your wallet stays fuller. Peace of mind remains intact. That’s the power of making an informed, responsible insurance decision.

Lower Insurance on Your Stored Car – Get a Quote Now!