The Medical Payments vs. Personal Injury Protection: Understanding the Difference

In the world of auto insurance, navigating medical coverage options can feel overwhelming after an accident. Two common yet often confused protections are Medical Payments Coverage (MedPay) and Personal Injury Protection (PIP). Both help with medical expenses, but they differ significantly in scope, requirements, and availability.

Get Expert MedPay vs PIP Guidance Today – Call Now!

This comprehensive guide breaks down the key differences, benefits, and considerations to help you make informed decisions about your policy. Whether you're a Dallas driver commuting through busy Texas roads or a family prioritizing financial security, understanding MedPay vs. PIP ensures you're prepared for the unexpected.

What Is Medical Payments Coverage (MedPay)?

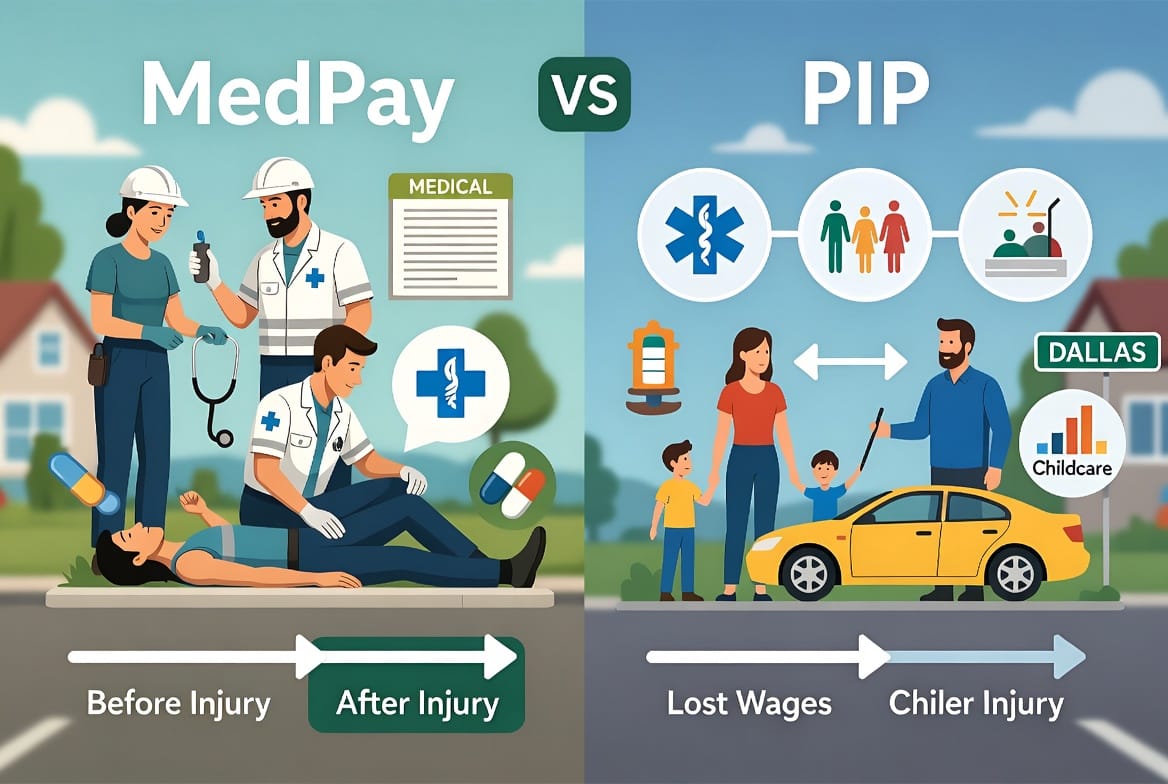

Medical Payments Coverage, commonly known as MedPay, is a vital component of many auto insurance policies. It provides no-fault medical expense coverage for you and your passengers, regardless of who caused the accident.

MedPay steps in quickly to cover immediate medical bills, making it a reassuring safety net during stressful times.

- Key Features of MedPay:

- Pays for reasonable and necessary medical expenses up to your policy limit.

- No deductible in most cases, allowing faster access to funds.

- Covers injuries to the policyholder, family members, and passengers in your vehicle.

- Available in nearly all states, often as an optional add-on.

Typical expenses covered include emergency room visits, hospital stays, surgeries, X-rays, and ambulance services. Limits usually range from $1,000 to $10,000 per person, though higher amounts are available.

MedPay offers simplicity and speed. It doesn't require proving fault, which can accelerate claims processing and reduce out-of-pocket stress for families dealing with injuries.

What Is Personal Injury Protection (PIP)?

Personal Injury Protection (PIP) provides broader coverage than MedPay. Often called "no-fault" insurance, PIP is mandatory in certain states and covers more than just medical bills.

PIP addresses the full financial impact of an injury by including:

- Medical and rehabilitation expenses

- Lost wages due to inability to work

- Childcare or household services replacement costs

- Funeral expenses in tragic cases

- Sometimes even non-economic damages like pain and suffering (depending on state laws)

This makes PIP particularly valuable for those with families or variable incomes. Coverage limits are typically higher, often starting at $10,000 and going up to $250,000 or more per person.

PIP shines in scenarios where injuries lead to extended recovery periods. For example, a fractured bone might heal medically in weeks but prevent work for months – PIP helps bridge that gap.

Key Differences Between MedPay and PIP

While both coverages operate on a no-fault basis, their differences are substantial. Here's a clear comparison:

MedPay is more limited and focused solely on medical bills. It acts as primary or secondary coverage and is generally cheaper to add to a policy.

PIP, on the other hand, is more comprehensive. It includes economic losses beyond medical care and is often required in no-fault states.

- Fault Determination: Both ignore fault for initial claims, but PIP may have thresholds for suing at-fault parties in some states.

- Coverage Scope: MedPay = medical only. PIP = medical + wages + additional expenses.

- Availability: MedPay widely optional. PIP mandatory in about a dozen states.

- Premium Cost: MedPay is typically more affordable; PIP costs more due to broader protection.

- Claim Process: MedPay claims process faster with fewer documentation needs.

Understanding these nuances helps drivers choose coverage that matches their lifestyle and risk profile.

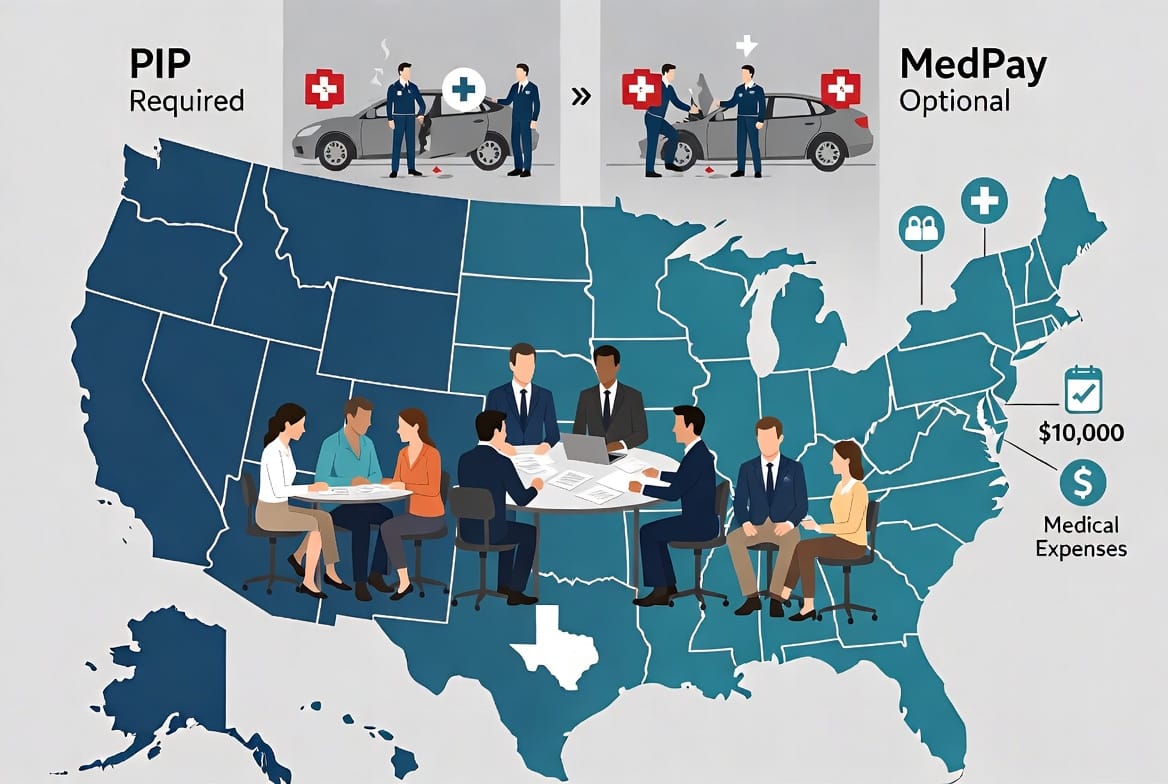

State-by-State Variations in MedPay and PIP

Auto insurance regulations vary significantly across the United States, directly impacting MedPay and PIP availability.

No-Fault States (requiring PIP):

- Florida

- Michigan

- New York

- New Jersey

- Pennsylvania

- And others like Hawaii, Kansas, Kentucky, Massachusetts, Minnesota, North Dakota, and Utah.

In these states, PIP is typically mandatory, with varying minimum limits and thresholds for additional lawsuits.

At-Fault States (MedPay more common as optional):

Most other states, including Texas, operate under tort (at-fault) systems. Here, MedPay is a popular optional coverage, while PIP may be available but less emphasized.

Texas drivers, for instance, often pair MedPay with liability coverage for quick medical support on highways around Dallas and beyond. Some states allow both, letting policyholders stack benefits for maximum protection.

Always check your state's Department of Insurance resources, as laws evolve. Consulting a local expert ensures compliance and optimal coverage.

Benefits of Choosing the Right Medical Coverage

Selecting between MedPay and PIP – or combining them – provides reassurance during recovery.

Advantages of MedPay:

- Lower premiums

- Quick payouts for medical bills

- No need to battle insurance companies over fault initially

- Ideal supplement for health insurance gaps

Advantages of PIP:

- Comprehensive income replacement

- Support for family needs during recovery

- Potential premium discounts in some areas for safe drivers

- Stronger protection in no-fault environments

Many experts recommend reviewing your policy annually. Factors like commuting distance, family size, and existing health coverage influence the best choice.

For Dallas homeowners and drivers, local conditions such as heavy traffic and variable weather make robust medical coverage essential.

Common Misconceptions About MedPay and PIP

Several myths persist around these coverages:

- "My health insurance is enough." Health plans often have deductibles, copays, and exclusions that auto medical coverage can fill.

- "PIP is only for serious injuries." Even minor accidents benefit from PIP's wage replacement.

- "MedPay duplicates health insurance." MedPay coordinates with other policies, often covering what health insurance doesn't.

- "These coverages are too expensive." Add-ons are affordable relative to potential medical costs, which can reach tens of thousands quickly.

By addressing these misconceptions, drivers gain confidence in their protections.

How to Evaluate Your Needs

Assess your situation thoughtfully:

- Do you have dependents relying on your income?

- How comprehensive is your health insurance?

- What are the minimum requirements in your state?

- Are you frequently transporting passengers?

Discuss options with your insurer. Many offer quotes showing side-by-side impacts of adding MedPay or PIP.

Real-world example: A rear-end collision in Dallas traffic leaves a driver with whiplash and two weeks off work. MedPay covers the ER visit, while PIP additionally reimburses lost wages and physical therapy – a significant difference for family budgets.

Steps to Optimize Your Auto Insurance Medical Coverage

- Review Current Policy: Examine declarations page for existing MedPay or PIP limits.

- Compare Quotes: Request personalized options from multiple carriers.

- Understand Coordination of Benefits: Learn how these interact with health insurance.

- Consider Bundling: Combine with other coverages for potential discounts.

- Consult Professionals: Speak with experienced agents familiar with Texas laws.

Taking these steps empowers you to build a policy that truly protects what matters most – your health and financial stability.

The Importance of Being Prepared

Accidents happen unexpectedly. Having the right medical coverage transforms a stressful event into a manageable one. MedPay offers targeted, efficient medical bill relief, while PIP delivers broader support for full recovery.

Knowledge is your strongest ally. Stay informed, review coverage regularly, and don't hesitate to seek expert guidance.

In today's fast-paced world, especially for Texas families navigating urban and suburban driving challenges, proactive insurance decisions provide lasting peace of mind.

Secure the Right Auto Medical Coverage – Call Now!