The Inventory Imperative: Documenting Your Belongings for a Smoother Home Insurance Claim

Imagine the unthinkable: a burst pipe floods your basement, or a fire ravages your living room. In the aftermath, you're left sifting through the chaos, trying to recall every item lost or damaged. Without proper documentation, your home insurance claim could drag on for months, leading to frustrating delays and potential underpayments. But here's the reassuring truth: creating a comprehensive home inventory is a straightforward step that empowers you to navigate claims with confidence. This guide walks you through why it's essential, how to do it effectively, and the tools that make it seamless. By documenting your belongings now, you're not just preparing for the worst—you're ensuring a smoother path to recovery.

Protect Your Belongings – Get Expert Help Now

Why a Home Inventory Matters for Insurance Claims

Homeowners often underestimate the value of their possessions until disaster strikes. According to industry experts, the average household holds tens of thousands of dollars in personal property, from electronics to heirlooms. Yet, without a detailed record, proving ownership and value becomes a hurdle during a home insurance claim process.

A well-maintained inventory serves as undeniable evidence, accelerating approvals and maximizing reimbursements. Insurers appreciate the clarity it provides, reducing back-and-forth disputes. In fact, policyholders with thorough documentation often see claims settled 20-30% faster, based on common insurer feedback. This isn't about paranoia; it's about practical preparedness. Think of it as your personal safety net, turning a stressful situation into a manageable one.

Key benefits include:

- Faster Payouts: Detailed lists help adjusters verify claims quickly, avoiding prolonged investigations.

- Accurate Valuations: Receipts and photos prevent undervaluation of items like jewelry or antiques.

- Peace of Mind: Knowing your coverage aligns with your assets reduces post-loss anxiety.

Remember, standard homeowners insurance covers personal property, but limits apply—typically 50-70% of your dwelling coverage. A inventory ensures you're not caught off guard by these caps.

Getting Started: Planning Your Home Inventory

Embarking on a home inventory might seem daunting, but breaking it down into steps makes it achievable. Start small to build momentum, focusing on high-value areas first. The goal is completeness without overwhelm.

Choose Your Method: Decide between digital or manual approaches. Digital tools are recommended for their accessibility and ease of updates.

Gather Essential Tools: You'll need a smartphone or camera, notebook or app, and storage for receipts.

Set a Timeline: Dedicate 30-60 minutes per room, aiming to complete the full inventory over a weekend or spread across weeks.

Prioritize rooms based on value density. For instance:

- Kitchen: Appliances and gadgets.

- Living Room: Electronics and furniture.

- Bedrooms: Clothing and jewelry.

This strategic approach ensures you cover the most critical assets early.

Methods for Creating Your Home Inventory

There are several reliable ways to document your belongings, each with unique advantages. Select one that fits your tech comfort level and lifestyle.

Video Walkthroughs: A Visual Storytelling Approach

One of the most effective and user-friendly methods is a video walkthrough. Use your smartphone to narrate a tour of each room, zooming in on items while describing details. This creates a dynamic record that's easy to reference.

Steps to create a video inventory:

- Room-by-Room Filming: Start at the entrance and pan slowly, opening drawers and closets.

- Verbal Annotations: State item names, brands, and estimated values aloud.

- Backup Securely: Upload to cloud storage like Google Drive or iCloud for safekeeping.

Videos are particularly powerful because they capture context—showing how items are stored or grouped—which can be invaluable for claims involving theft or damage.

Cloud-Based Apps: Tech-Savvy Organization

For a more structured option, leverage cloud-based inventory apps such as Sortly, Encircle, or HomeZada. These platforms allow you to catalog items digitally, attaching photos and documents.

Advantages include:

- Searchability: Quickly find items by keyword or category.

- Automatic Backups: Data syncs across devices, protecting against loss.

- Value Tracking: Some apps integrate with market data for real-time valuations.

To use an app effectively:

- Scan barcodes for automatic entry of product details.

- Upload receipts directly from your email or photos.

- Categorize items (e.g., electronics, furniture) for easy reporting.

These tools transform inventorying from a chore into an efficient process, often with reminders for updates.

Traditional Lists: Simple Yet Effective

If digital isn't your preference, a manual list in a spreadsheet or notebook works well. Use columns for item description, purchase date, cost, and location.

Enhance it by:

- Attaching printed photos.

- Storing in a fireproof safe or digitally scanning for backups.

While less automated, this method is accessible and customizable.

No matter the method, consistency is key. Update your inventory annually or after major purchases to keep it current.

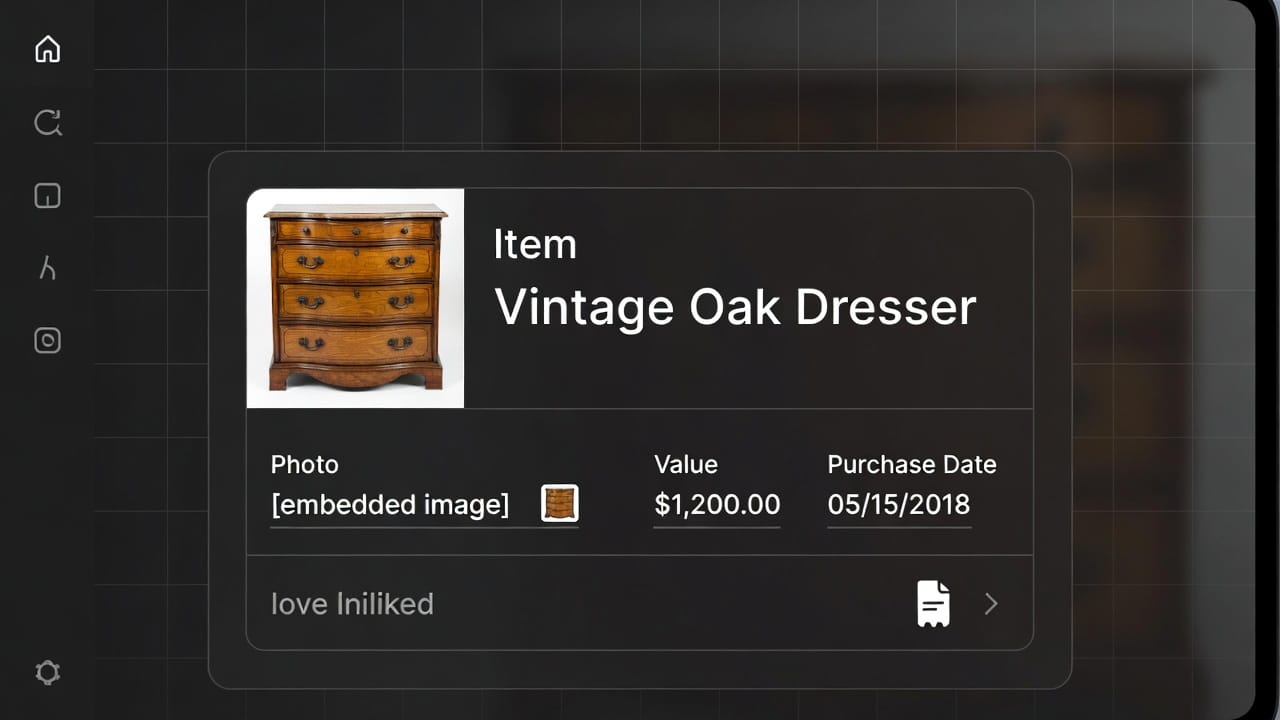

What Details to Record: The Essentials

Accuracy is the cornerstone of a useful home inventory. Focus on specifics that prove ownership and value, making your insurance claim ironclad.

Core details for each item:

- Description: Include make, model, color, and size (e.g., "Samsung 55-inch 4K Smart TV, black").

- Serial Numbers: Crucial for electronics and appliances; locate them on the item or manual.

- Purchase Information: Date, retailer, and original cost—scan receipts for digital copies.

- Current Value: Estimate replacement cost; use apps or online tools for appraisals.

- Photos/Videos: Multiple angles, including any unique features or damage.

For high-value items like art or collectibles:

- Obtain professional appraisals.

- Note any warranties or certifications.

Group smaller items (e.g., kitchen utensils) into categories to avoid exhaustive listing, but itemize valuables over $200.

Risks of incomplete details:

- Denied Claims: Without proof, insurers may reject reimbursements.

- Underinsurance: Forgetting items leads to gaps in coverage.

By recording comprehensively, you mitigate these risks and streamline settlements.

How Documentation Speeds Up Claim Settlements

After a loss, time is of the essence. A thorough inventory transforms the home insurance claim process from chaotic to efficient.

Here's how it works in practice:

- Initial Reporting: Provide your insurer with the inventory list immediately, highlighting affected items.

- Adjuster Review: Photos and details allow quick verification, often remotely.

- Settlement Calculation: Accurate values prevent haggling, leading to fair offers.

Real-world impact: Policyholders without inventories often face delays of weeks or months, while those with documentation resolve claims in days. Insurers like State Farm and Allstate emphasize that pre-loss records reduce fraud suspicions and expedite payouts.

Common pitfalls to avoid:

- Outdated Information: Regular updates prevent discrepancies.

- Insecure Storage: Use encrypted cloud services to protect sensitive data.

- Overlooking Off-Site Items: Include belongings in storage units or vacation homes.

In essence, your inventory acts as a roadmap for recovery, ensuring you receive what you're entitled to without unnecessary stress.

Maintaining and Updating Your Inventory

A one-time effort isn't enough; life changes, and so should your records. Make updating a habit to maintain relevance.

Strategies for maintenance:

- Annual Reviews: Schedule a yearly walkthrough to add new items and remove sold ones.

- Post-Purchase Additions: Snap a photo and log details immediately after buying.

- Life Event Triggers: Update after moves, renovations, or inheritances.

Tools like apps send reminders, making this effortless. Secure storage is vital—opt for password-protected platforms and multiple backups.

If disaster strikes before an update, partial documentation is still better than none. Start today to build a robust foundation.

Integrating Your Inventory with Your Insurance Policy

Align your inventory with your homeowners insurance for optimal protection. Review your policy's personal property limits and consider endorsements for valuables.

Steps to integrate:

- Share with Your Agent: Provide a summary to confirm adequate coverage.

- Adjust Coverage: If inventory reveals gaps, increase limits or add riders.

- Understand Exclusions: Note items like floods (requiring separate policies).

This synergy ensures your documentation supports your coverage, avoiding surprises.

Real-Life Success Stories

Consider Jane, a homeowner whose basement flooded. With her video inventory, she submitted claims for ruined electronics swiftly, receiving full reimbursement in two weeks—versus months for neighbors without records.

Or Mike, who lost jewelry in a burglary. His app-stored appraisals and photos led to a seamless settlement, covering replacement costs entirely.

These stories underscore the transformative power of preparation.

Final Thoughts: Empower Your Protection

Documenting your belongings isn't just a task—it's an investment in your future security. By creating a detailed home inventory, you're equipping yourself for smoother home insurance claims, faster recoveries, and greater peace of mind. Don't wait for a loss to highlight its importance; act now.

Secure Your Assets Today – Free Coverage Review Call