The Home Sharing Liability: What Airbnb Hosts Need to Know

As an Airbnb host, you’ve turned your spare room or vacation property into a rewarding side income. But beneath the five-star reviews and extra cash lies a critical reality: short-term rental liability can expose you to financial risks that standard homeowners insurance simply won’t cover.

Protect Your Airbnb Today – Call Now!

At its core, hosting strangers creates a business activity inside what your insurer sees as a personal residence. This single shift can leave massive gaps in protection. Understanding these risks—and the specialized solutions available—lets you host confidently while safeguarding your biggest asset.

The Rising Popularity of Home Sharing and Its Hidden Dangers

Home sharing has exploded, offering flexibility and income for millions. Yet every booking introduces variables outside your control: guest behavior, accidental damage, or unexpected injuries.

Key risks include:

- Guest injuries on your property (slips, trips, or pool-related incidents)

- Property damage from parties or careless use

- Theft of your belongings or neighbor complaints

- Liability for third-party claims when guests interact with neighbors or the public

Without proper coverage, a single claim could cost tens or hundreds of thousands of dollars—potentially forcing you to sell your home to settle it.

Bold truth: Your standard homeowner’s policy was never designed for this. Treating your listing as a passive rental ignores how insurers classify short-term hosting as a business use exclusion.

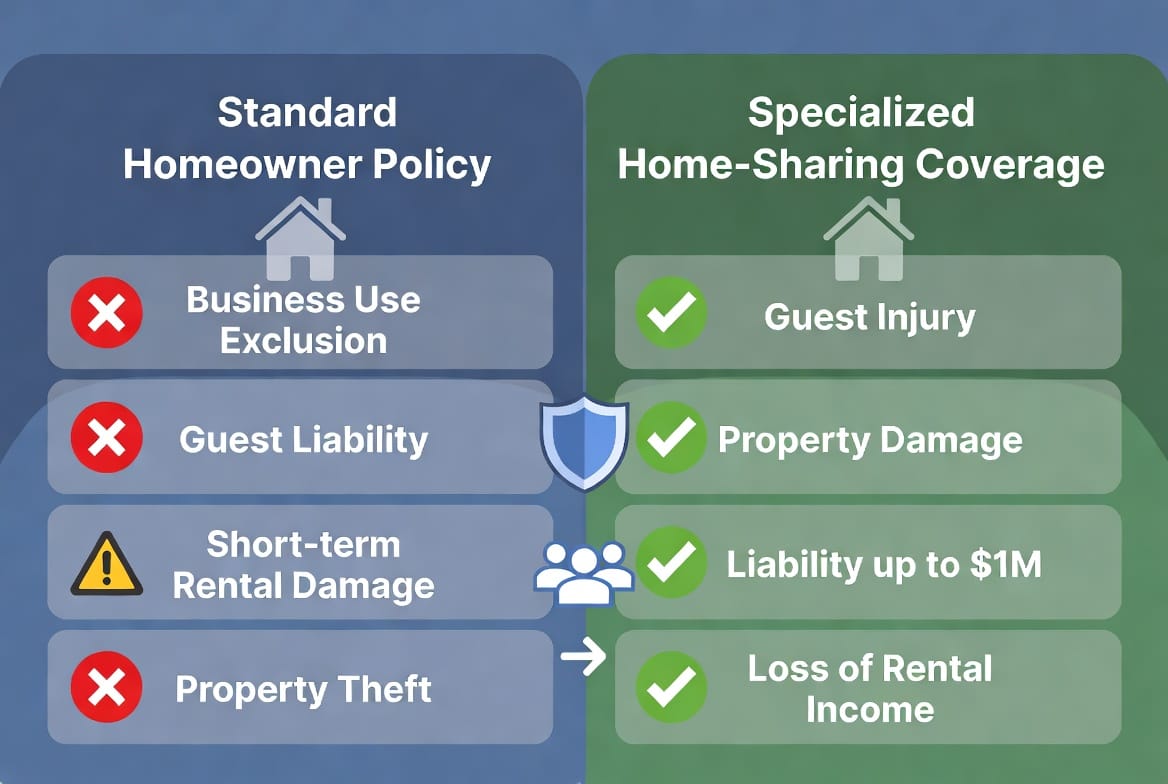

Why Standard Homeowner’s Insurance Falls Short

Most traditional homeowners policies contain explicit business use exclusions. Once you regularly rent your property—even for a few nights—you step outside personal-use coverage.

Common gaps include:

- No protection for commercial liability arising from guest activities

- Denial of claims if damage occurs during a paid booking

- Limited or zero coverage for lost rental income after a covered event

- Exclusions for high-value items frequently used by guests (electronics, furniture, decor)

Imagine a guest slips on a wet floor and files a lawsuit. Or a rowdy group causes thousands in repairs. Your insurer may investigate the booking history and deny the claim entirely, leaving you personally responsible.

This isn’t hypothetical. Hosts across the country have faced devastating out-of-pocket expenses because they assumed “my home insurance will handle it.” The reassuring news? Targeted solutions exist that restore peace of mind without complicating your hosting.

What Specialized Home-Sharing Coverage Actually Provides

Modern home-sharing insurance bridges the gaps left by traditional policies. These specialized endorsements or standalone policies treat your Airbnb activity as the business it is, while protecting your personal residence.

Core benefits typically include:

- Guest liability coverage up to $1 million or more for injuries or accidents

- Property damage protection specific to short-term rental use

- Theft and vandalism coverage during guest stays

- Loss of rental income if your property becomes uninhabitable after a claim

- Legal defense costs for lawsuits arising from hosting

Many policies also cover host-specific risks such as guest-caused mold issues, key duplication liability, or even cyber incidents related to booking platforms.

The tone here is reassuring: You don’t need to stop hosting. You simply need the right layer of protection that works alongside your existing homeowner’s policy.

Airbnb’s Platform Protection vs. Supplemental Insurance

Airbnb offers its own Host Guarantee and Host Protection Insurance, which sound comprehensive. However, these have important limitations that many hosts overlook.

Platform coverage typically:

- Applies only after your personal insurance pays (secondary coverage)

- Excludes certain high-risk incidents or personal belongings

- Caps protection and may not cover all liability scenarios

- Ends when the guest leaves or the booking period expires

Supplemental home-sharing policies act as primary or true excess coverage. They fill voids Airbnb leaves and provide proactive protection before, during, and after stays.

Savvy hosts combine both: Airbnb’s program for baseline support plus a dedicated policy for robust, customized safeguards. This layered approach delivers maximum security without overpaying.

Real-World Scenarios: How Coverage Makes the Difference

Consider Sarah, a host in a popular tourist city. A guest threw an unauthorized party, causing $8,000 in damages and neighbor complaints. Her standard policy denied the claim due to business use. A specialized home-sharing endorsement covered repairs and legal fees, allowing her to continue hosting profitably.

Or Mike, whose guest suffered a minor injury on stairs. The resulting claim exceeded $150,000. His supplemental policy handled defense costs and settlement, preserving his savings and home equity.

These stories highlight why proactive coverage isn’t an expense—it’s an investment in your hosting business’s longevity.

Choosing the Right Home-Sharing Coverage for Your Needs

Selecting appropriate protection requires evaluating several factors:

- Your property type (urban apartment, suburban house, vacation rental)

- Booking frequency and average guest count

- Unique features (pool, hot tub, valuable art/electronics)

- Local regulations and short-term rental laws in your area

- Desired liability limits based on your risk tolerance

Work with an independent insurance advisor experienced in home sharing. They can review your current policy, identify exact gaps, and tailor a solution that integrates seamlessly.

Pro tip: Review your coverage annually or after major platform policy changes. Hosting rules and risks evolve quickly—your protection should too.

Additional Risk Management Strategies for Smart Hosts

Insurance forms the foundation, but smart practices reduce claims and premiums:

- Install smart locks, security cameras (with guest privacy notices), and clear house rules

- Use professional cleaning services between stays

- Document property condition with detailed photos before every booking

- Require guests to acknowledge safety guidelines in writing

- Maintain strong communication to prevent misunderstandings

These steps demonstrate responsible hosting to both guests and insurers, often qualifying you for better rates.

The Bottom Line: Protect Your Hosting Side Gig Today

Home sharing offers tremendous opportunity, but only when you address the liability realities head-on. By understanding standard policy gaps, embracing specialized home-sharing coverage, and layering it with platform protections, you create a resilient foundation for sustainable income.

Don’t let fear of the unknown limit your potential. The right coverage lets you focus on delivering exceptional guest experiences while knowing your home, finances, and future remain secure.

Protect your hosting side gig. Our team specializes in tailoring policies that fit your unique Airbnb business—quick, affordable, and comprehensive.

Start hosting with confidence. Your property deserves nothing less.

Don't Risk Your Home – Get Protected Now