The Landlord Insurance Differences: What Renting Changes in Your Coverage

When you decide to rent out your property, everything about your insurance needs shifts. Standard homeowners insurance is built for owner-occupied homes, not investment properties. Renting introduces new risks, new responsibilities, and entirely different coverage requirements. Understanding these landlord insurance differences is essential to protecting your investment, your income, and your peace of mind.

Protect Your Rental Property Now – Call for a Free Quote

Many landlords discover too late that their existing homeowners policy simply does not apply once tenants move in. The good news? Specialized landlord insurance is designed precisely for this situation. It fills the critical gaps and gives you the comprehensive protection you deserve as a rental property owner. In this guide, we break down exactly what changes when you rent, what a true landlord policy covers, and why these distinctions matter more than ever.

Why Standard Homeowners Insurance Falls Short for Rental Properties

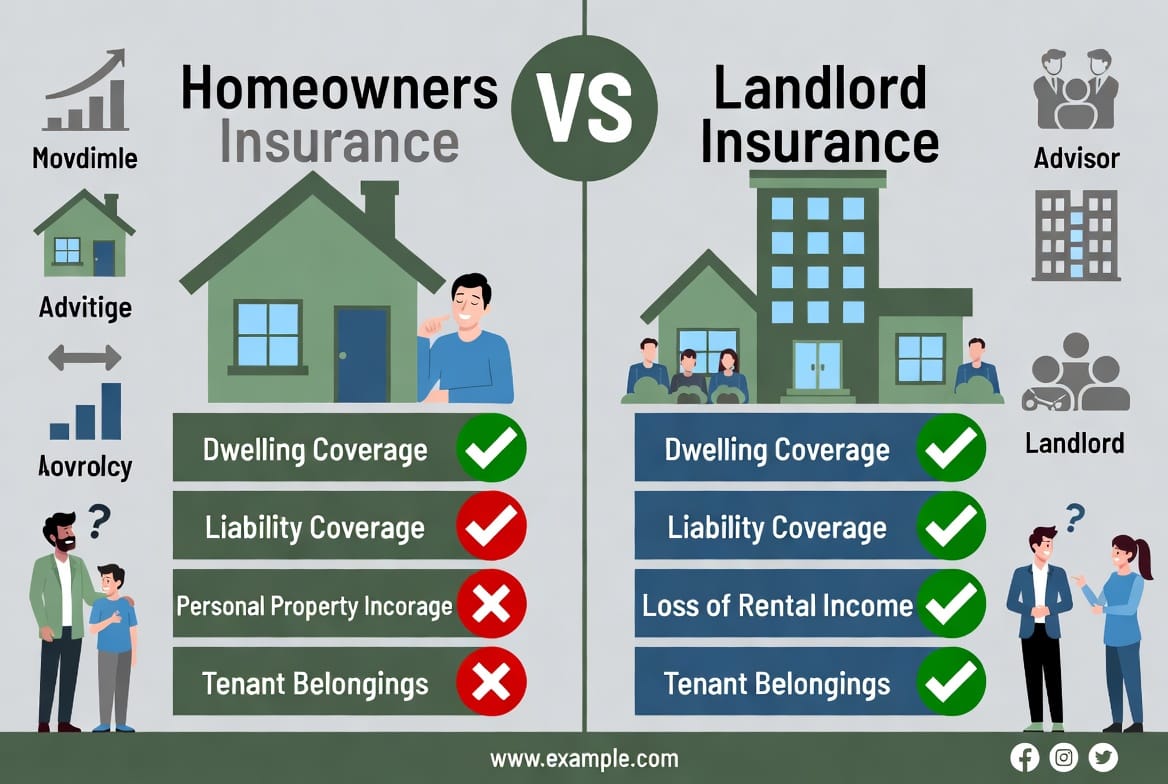

A standard homeowners insurance policy assumes you live in the home. Once you convert the property to a rental, the insurer views it as a business activity. This single change triggers important exclusions.

Key limitations of homeowners coverage on rental properties include:

- No protection for loss of rental income if the property becomes uninhabitable

- Limited or zero liability coverage for incidents involving tenants or guests

- Exclusion of coverage for damages related to tenant activities or business use

- No reimbursement for repairs needed after covered perils if the home is rented

These exclusions leave landlords exposed to significant financial risk. A burst pipe, storm damage, or even a slip-and-fall incident on your rental property could result in thousands of dollars in uncovered costs. Renting fundamentally changes your risk profile, and your insurance must change with it.

Rest assured, this is a common transition. Thousands of property owners successfully switch to proper landlord insurance every year and sleep better knowing their investment is truly protected.

What Landlord Insurance Actually Covers – And What It Doesn’t

Landlord insurance (sometimes called dwelling fire or rental property insurance) is specifically engineered for income-producing properties. It addresses the unique risks landlords face while providing targeted protections.

Core Coverages Included in Most Landlord Policies

- Dwelling Coverage: Protects the physical structure of your rental property – walls, roof, foundation, and built-in systems – against fire, wind, hail, vandalism, and other covered perils. This is often the largest and most important part of your policy.

- Liability Coverage for Premises: Shields you from legal and medical expenses if someone is injured on your rental property. Whether it’s a tenant, guest, or delivery person, premises liability is crucial when you no longer occupy the home yourself.

- Loss of Rental Income: If a covered event (such as fire or storm damage) makes the property unlivable, this coverage reimburses you for the rent you would have collected while repairs are completed. This feature alone can save landlords from devastating cash-flow disruptions.

Importantly, landlord insurance does not cover your tenants’ personal belongings. Tenants are responsible for their own possessions and should purchase separate renters insurance. This clear distinction prevents confusion and ensures everyone understands their responsibilities.

Real-World Impact: How These Differences Protect Your Investment

Consider a typical scenario. A severe windstorm damages the roof of your rental home. Under a standard homeowners policy, you might receive nothing because the property is rented. With proper landlord insurance, the dwelling coverage pays for repairs, liability protection handles any guest injuries during the storm, and loss-of-rental-income coverage keeps your mortgage payments on track while the unit is being fixed.

These protections turn potential disasters into manageable events. Landlords who understand and secure the right policy report greater confidence, smoother tenant relationships, and stronger long-term returns on their real estate investments.

Optional Enhancements That Add Even More Value

Many landlord insurance policies allow you to customize coverage with valuable endorsements:

- Contents coverage for appliances and fixtures you own (refrigerators, washers, dryers, etc.)

- Ordinance or law coverage for increased costs due to building code upgrades after a loss

- Flood or earthquake endorsements where needed

- Vacancy coverage during tenant turnover periods

Working with an experienced agent ensures your policy matches your specific property and risk profile. The result is tailored, comprehensive protection rather than a one-size-fits-all approach.

Common Misconceptions About Landlord Insurance

One frequent myth is that homeowners insurance can simply be “adjusted” for rentals. In reality, most insurers require a completely separate landlord policy once the property is no longer owner-occupied. Another misconception is that tenant renters insurance replaces the need for landlord coverage – it does not. Tenants protect their belongings; you protect the building, your liability, and your rental income.

By addressing these misconceptions early, you avoid unpleasant surprises at claim time. Knowledge truly is your best defense.

Choosing the Right Landlord Insurance Policy for Your Property

Selecting the proper coverage starts with an honest assessment of your rental. Consider property value, location-specific risks, tenant profile, and your own financial goals. An independent insurance professional can compare options from multiple carriers and design a policy that delivers maximum protection at a competitive price.

Remember, the goal is not just to meet minimum requirements but to build a safety net that lets you focus on growing your rental portfolio with confidence.

Frequently Asked Questions

Does landlord insurance cost more than homeowners insurance?

Typically yes, because it covers additional risks such as loss of rental income and higher liability exposure. However, the added protections often prove invaluable.

Can I get landlord insurance if the property is currently vacant?

Many policies offer vacancy coverage or short-term options while you prepare the property for tenants.

What if my tenant causes damage?

Landlord insurance covers many accidental damages. Intentional damage by tenants may fall under your ability to recover costs through security deposits or legal action.

Is flood coverage included?

Standard policies usually exclude flood damage. Separate flood insurance is available and highly recommended in applicable areas.

Protecting What You’ve Built

Renting out your property is a smart financial move – but only when paired with the right insurance. The landlord insurance differences are not just technical details; they represent the line between financial security and potential loss.

By choosing a policy designed specifically for rental activities, you protect the dwelling, secure your liability, and safeguard your rental income. You also gain the freedom to manage your investment without constant worry.

Protect your rental investment properly. Our team is ready to review your current coverage and design a customized landlord insurance solution that gives you complete confidence in your rental property.

Secure Your Rental Income & Property – Call Now