The Credit Score and Insurance: How Your Credit Affects Premiums

In today's complex insurance landscape, credit-based insurance scores play a significant role in determining your home insurance premiums. Many homeowners are surprised to learn that their credit history can influence rates as much as property characteristics or claims history. This practice remains one of the more debated topics in insurance, yet it stems from decades of data showing clear statistical correlations between financial responsibility and claim likelihood.

Improve Your Credit, Lower Your Premiums – Call Now!

At its core, insurers aim to price policies fairly based on risk. A strong credit profile often signals lower risk, potentially leading to more affordable premiums. The good news? Understanding this connection empowers you to take control and potentially lower your costs. This comprehensive guide explains exactly how it works, what factors matter most, where restrictions apply, and actionable steps you can take today.

Why Insurers Consider Credit in Home Insurance

Home insurance protects one of your largest assets — your property and belongings. Insurers evaluate multiple risk factors when setting premiums, and credit-based insurance scores have become a key tool in that assessment for most states.

These scores differ from your standard FICO credit score used for loans or mortgages. Insurers develop specialized models that predict the likelihood of filing claims rather than defaulting on debt. Extensive actuarial studies support this approach, demonstrating that individuals who manage finances responsibly tend to file fewer and less costly claims.

This isn't about judging character. It's about using proven statistical patterns to create equitable pricing. Responsible financial habits often align with careful home maintenance, prompt claims reporting, and overall lower risk profiles.

How Credit-Based Insurance Scores Work

Insurers do not pull your regular credit score. Instead, they generate a credit-based insurance score using specific data from your credit report. This customized metric focuses on elements most predictive of insurance risk.

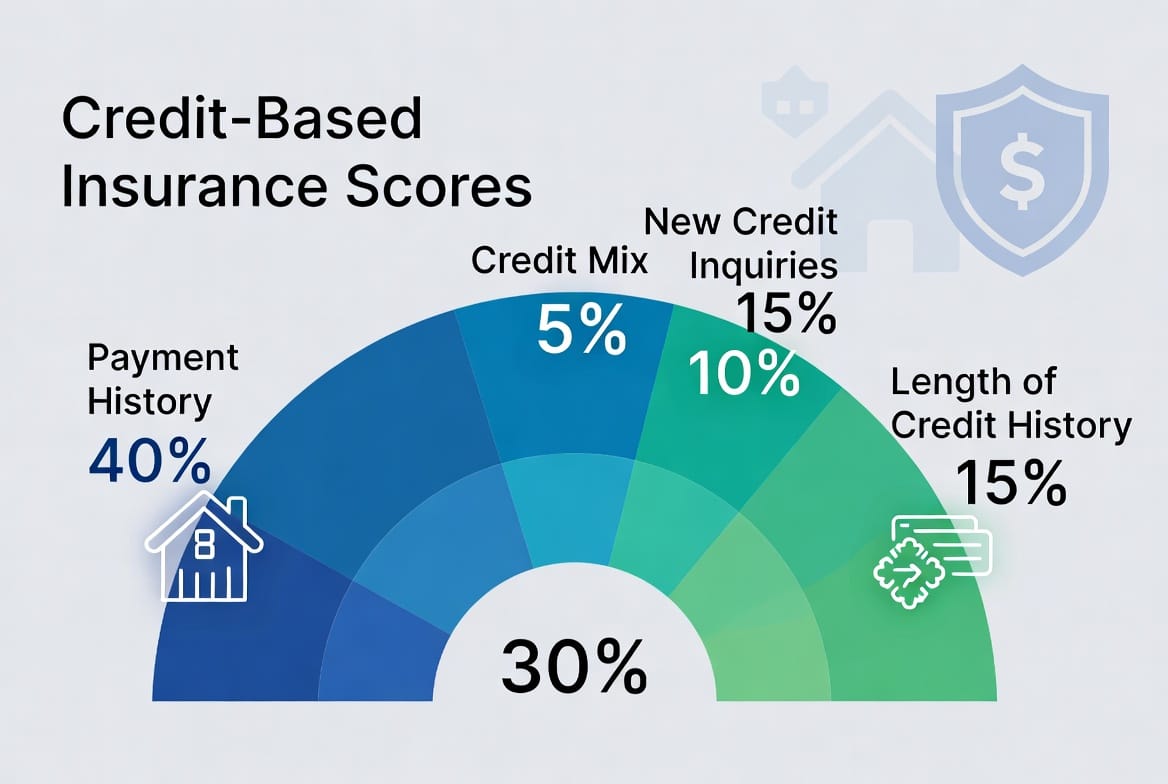

Key factors typically include:

- Payment History (often ~40% weight): Consistent on-time payments demonstrate reliability — the strongest predictor in most models.

- Outstanding Debt Levels (~30%): High utilization of available credit or large debts may indicate financial stress that correlates with higher claim frequency.

- Length of Credit History (~15%): Longer, stable credit accounts suggest proven financial management.

- New Credit Inquiries (~10%): Multiple recent applications can signal potential instability.

- Credit Mix (~5%): A balanced, responsibly managed mix of accounts (credit cards, installment loans, etc.) contributes positively.

These models undergo rigorous testing and comply with fair credit reporting laws. Importantly, they exclude prohibited factors like race, gender, or marital status.

The Controversy Surrounding Credit Use in Insurance

Critics argue that using credit information creates unfair barriers, especially for younger consumers, recent immigrants, or those recovering from financial setbacks. They contend it can create a cycle where financial challenges lead to higher insurance costs, further straining budgets.

Proponents, backed by industry data, counter that the correlation holds across diverse demographics. People with stronger credit profiles statistically present lower risk, allowing insurers to offer better rates to the majority of customers while maintaining financial stability for the industry.

This practice remains legal and widely used in most states precisely because regulators have reviewed the underlying data. However, transparency matters. Insurers must notify you if credit information adversely affects your quote or renewal.

States That Restrict or Prohibit Credit Use

Consumer protections vary significantly by location. Several states have enacted strict limitations to address equity concerns.

Notable restrictions include:

- California: Prohibits use of credit information for both auto and home insurance underwriting and rating.

- Massachusetts: Long-standing ban on credit-based scoring for personal lines insurance.

- Maryland: Significant restrictions, particularly on homeowners policies.

- Hawaii and Michigan: Strong prohibitions or limitations on credit use in rating.

Other states like Oregon and Utah also impose notable limits. Always check with your state insurance department for the most current rules, as regulations can evolve.

In unrestricted states, credit remains just one factor among many — not the sole determinant. Your claims history, property condition, location, and coverage choices still carry substantial weight.

Impact on Home Insurance Premiums Specifically

For homeowners, credit-based scores often influence:

- Base premium rates

- Eligibility for certain policy tiers or discounts

- Deductible options

- Bundling advantages with auto coverage

A lower credit-based insurance score might result in premiums 20-50% higher in some cases, though exact impacts vary widely by insurer and other risk factors. Conversely, excellent credit can unlock significant savings — sometimes hundreds of dollars annually on a standard homeowners policy.

Remember that improving your credit benefits multiple areas of life, including mortgage rates and overall financial health.

Practical Steps to Improve Your Credit-Based Insurance Score

The reassuring reality is that you have direct control over most factors. Positive changes can appear on your report relatively quickly.

Actionable strategies include:

- Prioritize on-time payments: Set up autopay or calendar reminders for all bills.

- Reduce debt utilization: Aim to keep credit card balances below 30% of limits.

- Avoid unnecessary new credit applications: Space out inquiries when possible.

- Review your credit reports annually: Dispute any inaccuracies through the major bureaus.

- Build positive history: Maintain older accounts in good standing and consider becoming an authorized user on a well-managed account if appropriate.

Many consumers see meaningful score improvements within 3-6 months of consistent effort. Pair these steps with smart home insurance shopping for maximum savings.

Beyond Credit: Other Factors That Shape Your Home Insurance Rates

Insurers use a holistic approach. Strong credit helps, but you can offset moderate scores through:

- Installing security systems and smoke detectors

- Choosing higher deductibles you can comfortably afford

- Maintaining a claims-free history

- Bundling multiple policies

- Improving your home's resilience features (impact-resistant roofing, etc.)

Professional insurance agents can help balance all these elements for optimal coverage at the best available rate.

Taking Control of Your Insurance Costs

Understanding the relationship between credit and insurance premiums demystifies what might otherwise feel like an opaque process. While the practice generates debate, it reflects insurers' commitment to data-driven, fair pricing for the majority of policyholders.

The most important takeaway: knowledge is power. By actively managing your credit and shopping multiple insurers, you position yourself for the most competitive rates available in your area.

Ready to see how your credit profile affects your home insurance? Our experienced team specializes in finding tailored solutions that consider your full financial picture. We’ll help you understand your options and work toward the coverage and premiums you deserve.

Protecting your home should bring peace of mind — not financial stress. Let us help you navigate the process with clarity and confidence.

Unlock Better Home Insurance Rates Today – Call Now!