The Aftermarket Parts Clause: OEM vs. Aftermarket Repairs

In today’s complex auto insurance landscape, understanding the aftermarket parts clause is essential for every vehicle owner. When an accident occurs, your insurer’s decision on repair parts can affect everything from safety to resale value. This authoritative guide explains the clause in clear terms, reveals how insurers typically handle repairs, and shows you exactly how to secure OEM parts when they matter most.

Protect Your Car with OEM Parts – Call Now!

OEM (Original Equipment Manufacturer) parts are produced by the same company that built your vehicle. Aftermarket parts are made by independent manufacturers. While both options can repair your car, the differences in quality, fit, and performance are substantial.

Understanding the Aftermarket Parts Clause

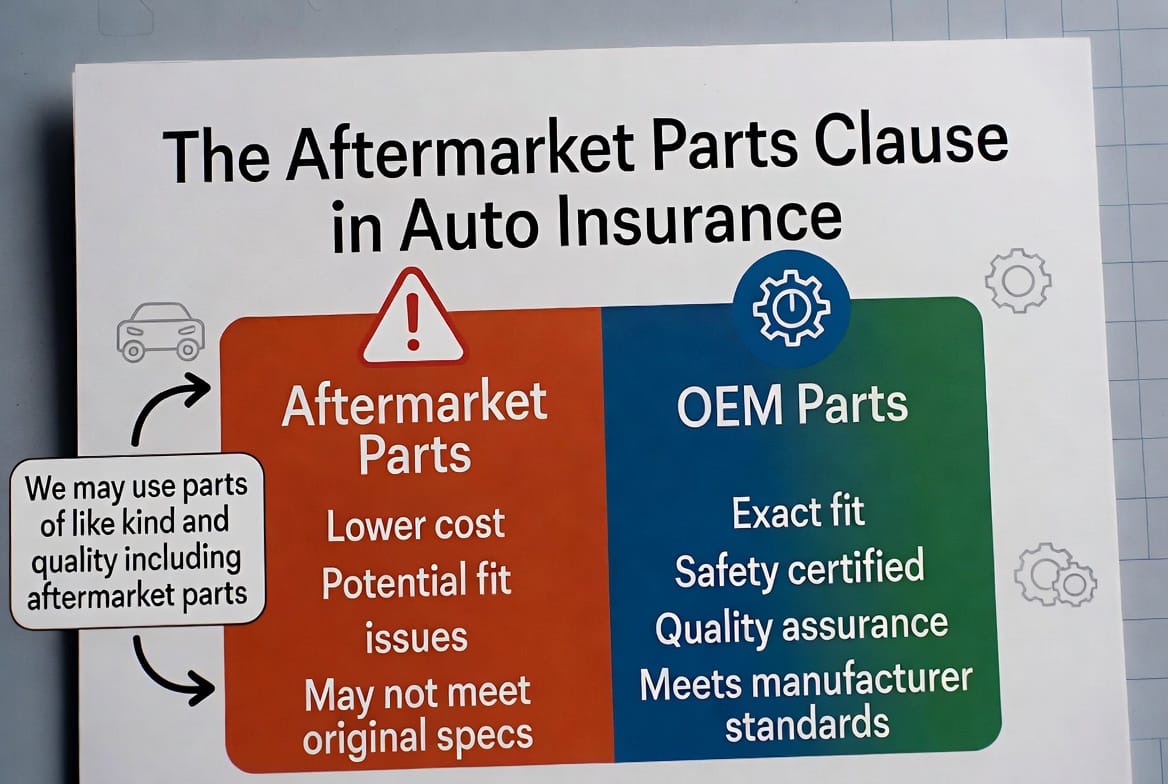

The aftermarket parts clause is a standard provision found in most collision coverage policies. It grants insurers the right to use non-original parts during repairs as long as they meet a basic standard of “like kind and quality.”

This clause helps insurers manage costs, but it can leave policyholders with repairs that don’t match factory standards. Knowledge is your best protection — knowing when and how to challenge this clause can make a meaningful difference in your claim outcome.

Key point: Most policies do not automatically guarantee OEM parts. You must either have specific OEM endorsement coverage or actively request it during the claims process.

How Insurance Policy Language Works

Typical policy wording often reads:

“We will repair or replace damaged property with property of like kind and quality.”

This neutral-sounding language gives insurers significant flexibility. In practice, “like kind and quality” frequently means aftermarket parts — especially for vehicles outside the manufacturer’s warranty period.

Important risks associated with aftermarket parts include:

- Inconsistent fit and finish that may lead to wind noise, water leaks, or visible gaps

- Compromised safety performance in structural and crash-related components

- Potential issues with future warranty claims

- Reduced resale value due to non-original parts history

On the other hand, OEM parts deliver exact factory specifications, superior engineering, and manufacturer-backed quality assurance.

When Insurers Typically Use Aftermarket Parts

Insurance companies routinely specify aftermarket parts for:

- Vehicles older than 3–5 years

- Economy and mid-range models

- Non-structural cosmetic repairs

- Claims where cost savings are prioritized

Aftermarket parts are generally 30–60% less expensive than OEM equivalents, making them attractive for insurers focused on controlling payout amounts.

However, there are important exceptions where OEM parts are more commonly approved:

- Newer vehicles still under factory warranty

- Leased vehicles where the leasing company requires original parts

- Luxury and premium vehicles where exact matching is expected

- Safety-critical components such as airbags, structural frame parts, and advanced driver-assistance systems

The Advantages of Choosing OEM Parts

OEM parts offer clear benefits that directly impact your driving experience and vehicle investment:

- Perfect fit and finish — designed specifically for your exact make, model, and year

- Maintained safety ratings — engineered to meet or exceed original crash-test standards

- Preserved manufacturer warranty — no risk of voiding coverage on related components

- Higher long-term durability — superior materials and manufacturing processes

- Better resale value — original parts maintain buyer confidence and market appeal

Pro tip: If you care about keeping your vehicle in factory condition, insisting on OEM parts is one of the smartest decisions you can make after an accident.

How to Request an OEM Endorsement

Fortunately, you don’t have to accept aftermarket parts automatically. Here’s how to secure better coverage:

- Review your current policy — Look for “OEM parts coverage,” “new parts coverage,” or “betterment” endorsements.

- Contact your agent or insurer — Ask specifically about adding OEM endorsement before you need it.

- Document everything — When filing a claim, clearly state in writing that you require OEM parts.

- Be prepared to negotiate — Many insurers will approve OEM parts for newer vehicles or when safety is a concern.

- Consider specialized coverage — Some insurers offer optional riders that guarantee OEM parts for all covered repairs.

Taking these steps early can save you significant stress and expense later.

Special Considerations for Leased and Newer Vehicles

If you drive a leased vehicle, the leasing company almost always requires OEM parts to maintain the car’s original condition and residual value. Using aftermarket parts could violate your lease agreement and result in costly penalties at turn-in time.

For newer vehicles still under warranty, OEM parts are critical to preserving full manufacturer coverage. Many dealership service centers will refuse to honor warranties if aftermarket parts have been installed in key areas.

Smart vehicle owners understand that protecting their investment means being proactive about repair specifications from day one.

Real-World Impact on Your Vehicle and Wallet

Choosing aftermarket parts might seem like a cost-saving measure in the short term, but the long-term consequences can be expensive. Poorly fitting parts often lead to repeated repairs, increased wear on surrounding components, and potential safety concerns that surface months or years later.

In contrast, OEM repairs restore your vehicle to its original condition, maintaining its performance, appearance, and market value. Many independent studies and repair industry experts consistently recommend OEM parts for vehicles less than eight years old or those with high mileage expectations.

Making the Right Choice for Your Peace of Mind

The aftermarket parts clause exists primarily for the insurer’s benefit. As a responsible vehicle owner, you have the right — and the power — to request higher-quality repairs.

Authoritative recommendation: If quality, safety, and long-term value matter to you, insist on OEM parts. Don’t hesitate to discuss your preferences with your claims adjuster and document every conversation.

At the end of the day, your vehicle is a major investment. Protecting it with the right parts after an accident is one of the best ways to safeguard both your safety and your finances.

Final Advice:

Insist on OEM if you care about quality.

Our experienced team can review your current policy, explain your options, and help you secure the coverage you truly need for true peace of mind on the road.

Upgrade to OEM Parts Protection – Speak to Us Today