Underinsured and Overexposed: Why Your Home's Rebuilding Cost is Not Its Market Value

In the world of home insurance, many homeowners fall into a dangerous trap: assuming their property's market value is the same as its rebuilding cost. This misconception can leave you underinsured and financially vulnerable in the event of a disaster. As an authoritative voice in insurance, we're here to clarify this critical difference and guide you toward proper protection. Rest assured, understanding these concepts empowers you to safeguard your most valuable asset—your home—without unnecessary stress.

Stop Guessing Your Coverage – Call for a Replacement Cost Assessment

The Critical Misconception in Home Insurance

At first glance, it might seem logical to base your home insurance coverage on what your house would sell for today. After all, that's the figure real estate agents tout and appraisers calculate. However, this approach overlooks a fundamental truth: market value and replacement cost are not interchangeable. Confusing the two can result in overexposure to financial risks, where a total loss leaves you scrambling to cover rebuilding expenses out of pocket.

Think of it this way: Your home's market value reflects its appeal to buyers in the current economy, influenced by location and demand. In contrast, replacement cost focuses solely on reconstructing the structure as it stands today, using current materials and labor rates. This distinction is vital because disasters like fires, floods, or storms don't discriminate—they can wipe out your home regardless of its resale price.

By addressing this early, you can avoid the pitfalls that affect millions of homeowners annually. Studies from industry leaders show that up to 60% of U.S. homes are underinsured by an average of 20%, leading to devastating gaps in coverage. But don't worry; with the right knowledge, you can bridge that gap confidently.

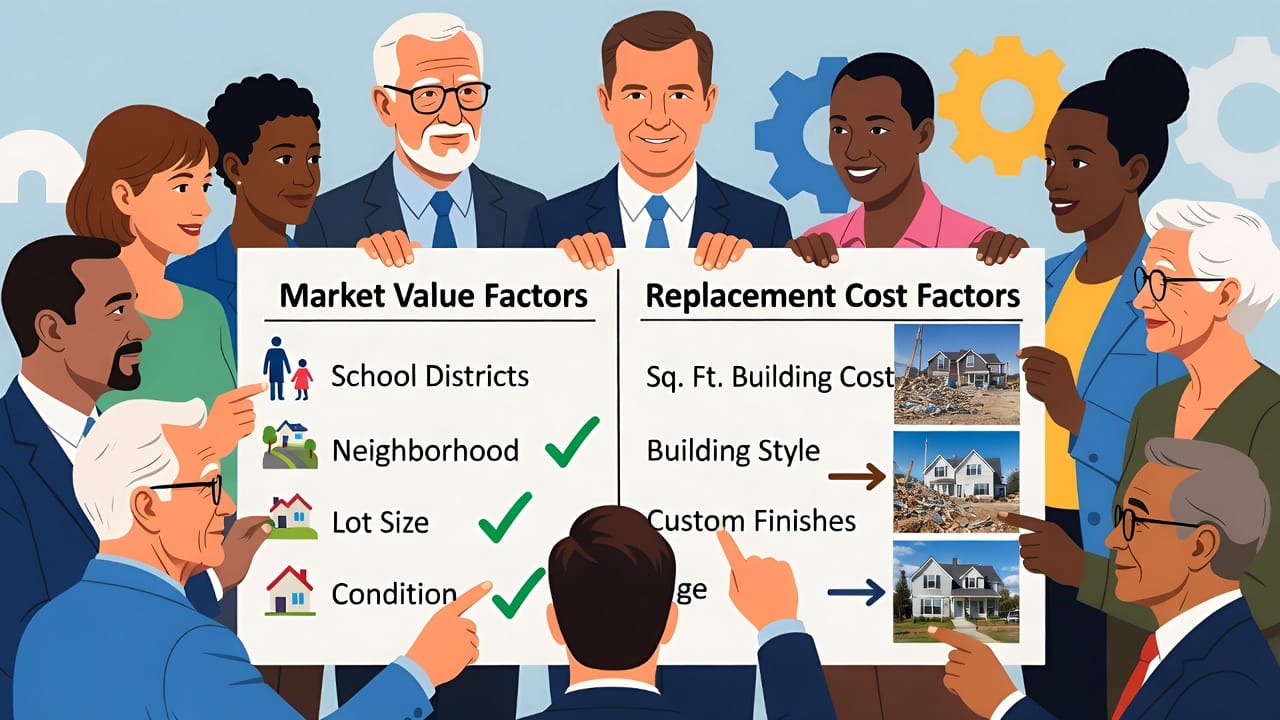

Understanding Market Value: More Than Just the Structure

Market value is the price a willing buyer would pay for your property in its current condition. It's a holistic figure that encompasses not only the building itself but also the land it sits on, plus external factors that drive desirability.

Key components include:

- Land value: Often the largest portion, especially in high-demand areas. For instance, a home on a prime lot near top-rated schools or urban amenities commands a premium.

- Location-driven factors: Proximity to jobs, transportation, and community features like parks or shopping centers can inflate values.

- Economic influences: Broader trends such as interest rates, job markets, and housing supply play a role. In booming regions, values soar; in slower ones, they stabilize or dip.

- Home improvements and curb appeal: Upgrades like renovated kitchens or landscaping add to the allure but don't always translate directly to rebuilding expenses.

This value is determined through appraisals, comparable sales (comps), and market analyses. It's fluid, changing with economic shifts—for example, during the 2020-2022 housing boom, many homes saw market values spike by 20-30%. Yet, this doesn't account for what it would take to rebuild if disaster strikes. Relying solely on market value for insurance can leave you exposed, as land isn't typically insured against loss (it's still there post-disaster).

Demystifying Replacement Cost: The True Cost to Rebuild

Shifting focus, replacement cost is the amount needed to reconstruct your home from the foundation up, using similar materials and quality. It ignores land value entirely, zeroing in on the physical structure.

Unlike market value, which buyers negotiate, replacement cost is calculated based on:

- Materials and labor: Current prices for lumber, wiring, plumbing, and skilled workers.

- Square footage and design: Larger or complex layouts increase costs.

- Local building codes: Updates required during rebuilding, such as enhanced seismic reinforcements or energy-efficient standards, can add 10-20% to the bill.

- Special features: Custom elements like granite countertops, hardwood floors, or smart home systems must be replicated.

Insurers use specialized tools, like replacement cost estimators, to arrive at this figure. These account for regional variations—rebuilding in coastal California, with its strict codes and high labor rates, costs far more than in the Midwest. Importantly, replacement cost often exceeds market value because it doesn't benefit from economies of scale or buyer negotiations; it's a straightforward reconstruction estimate.

For reassurance, know that accurate replacement cost coverage ensures you're not left paying the difference after a claim. It's about restoring your life, not just a building.

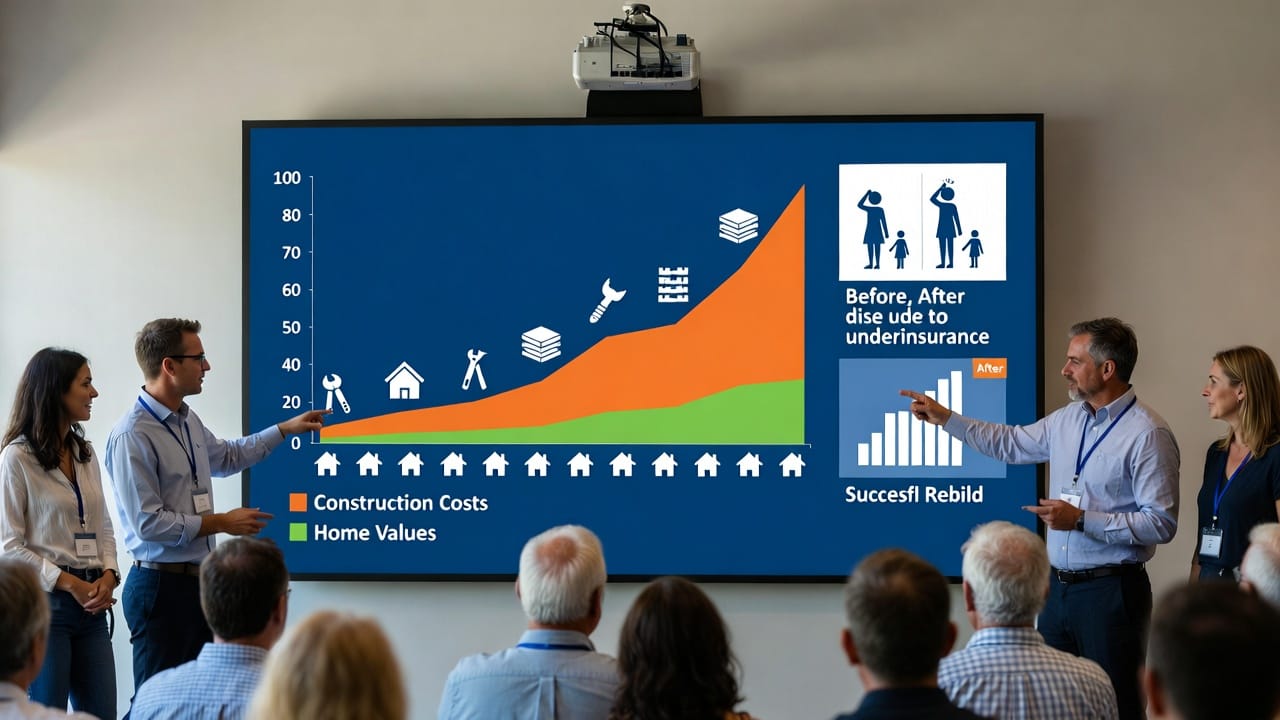

Why Rebuilding Often Costs More Than Expected

One of the most eye-opening aspects of home insurance is realizing that rebuilding costs frequently surpass initial assumptions. This isn't due to inflation alone but a combination of evolving factors that make reconstruction pricier.

Consider these common surprises:

- Rising construction costs: Materials like steel and wood have seen volatility, with lumber prices jumping 300% during supply chain disruptions in recent years.

- Code upgrades and compliance: Post-disaster rebuilds must meet current standards, not those from when your home was built. This could mean adding sprinkler systems or ADA-compliant features, boosting costs by thousands.

- Labor shortages: Skilled tradespeople are in high demand, driving up wages. In disaster-prone areas, competition for workers post-event can double rates.

- Unique architectural elements: Older homes with intricate details, like Victorian moldings or custom stonework, require specialized craftsmanship that's not cheap to replicate.

- Debris removal and site preparation: Clearing rubble and preparing the site adds 5-10% to the total, often overlooked in estimates.

These elements compound, making replacement cost 20-50% higher than market value in many cases. For example, a $500,000 market-value home might need $700,000 to rebuild due to premium materials and code mandates. The good news? Insurance policies with extended replacement cost endorsements can cover surges up to 150% of the stated amount, providing a safety net.

Factors That Drive Up Replacement Costs

To delve deeper, let's explore the specific influences on replacement cost. Awareness of these empowers you to advocate for accurate coverage.

- Geographic variations: Coastal or urban areas face higher costs due to regulations and material transport. In contrast, rural spots might see lower baselines but still require code updates.

- Inflation and economic trends: Construction indices, like the RSMeans data, track annual increases averaging 4-6%, outpacing general inflation.

- Home-specific details: Features such as pools, detached garages, or solar panels add layers of complexity and expense.

- Environmental considerations: In wildfire zones, fire-resistant materials are mandatory, elevating budgets.

- Supply chain impacts: Global events, from pandemics to trade tariffs, can cause sudden spikes in material availability and pricing.

By factoring these in, insurers create tailored estimates. Tools like the Marshall & Swift Valuation Service provide data-driven insights, ensuring your policy reflects reality. Rest easy knowing that regular reviews—every 2-3 years—keep your coverage aligned with these changes.

The Risks of Being Underinsured

Being underinsured isn't just a minor oversight—it's a potential financial catastrophe. Imagine a fire destroys your home, and your policy covers only 70% of the rebuild due to outdated estimates. You're on the hook for the rest, which could mean dipping into savings, taking loans, or even delaying reconstruction.

Common risks include:

- Out-of-pocket expenses: Gaps can reach hundreds of thousands, straining finances during recovery.

- Delayed rebuilding: Insufficient funds mean compromises on quality or prolonged temporary housing.

- Emotional toll: The stress of inadequate coverage compounds the trauma of loss.

- Policy penalties: Some insurers apply coinsurance clauses, reducing payouts if you're underinsured by a certain percentage.

Fortunately, these are avoidable. By prioritizing replacement cost over market value, you mitigate exposure. Industry experts recommend aiming for 100% coverage, with buffers for inflation.

Steps to Ensure Adequate Home Insurance Coverage

Taking action is straightforward and empowering. Start by:

- Reviewing your policy annually: Check the dwelling coverage limit against current estimates.

- Using professional estimators: Work with agents who employ advanced tools for precision.

- Considering endorsements: Add guaranteed replacement cost for unlimited coverage in total losses.

- Documenting your home: Photos and inventories help validate special features.

- Consulting experts: Independent reviews provide unbiased insights.

With these steps, you're not just insured—you're protected.

Final Thoughts: Protect What Matters Most

In summary, distinguishing market value from replacement cost is essential to avoid being underinsured. By understanding the factors at play, from local costs to code upgrades, you position yourself for full recovery. Remember, your home is more than an investment; it's your sanctuary. Our team is here to provide the authoritative guidance you deserve.

Close the Underinsurance Gap – Call for Expert Home Coverage Advice