The Uninsured Motorist Puzzle: Why This Coverage Protects You Even If You're at Fault (Sort Of)

In the complex world of auto insurance, few topics confuse drivers more than uninsured motorist (UM) and underinsured motorist (UIM) coverage. Often overlooked or misunderstood, this protection serves as a critical safety net when the unexpected happens. Contrary to common myths, UM/UIM coverage isn't just for accidents where the other driver is clearly at fault and uninsured—it can safeguard you and your passengers in scenarios where recovery from the at-fault party becomes impossible or inadequate.

Safeguard Against Uninsured & Underinsured Drivers – Call Now

Why does this matter now more than ever? Recent data shows that approximately 15.4% of U.S. motorists—more than one in seven drivers—were uninsured in 2023, with trends indicating persistence or slight increases into recent years. In some states, the figure exceeds 20% or even 28%. These statistics highlight a growing risk on the roads: You could be a careful, insured driver, yet still face devastating financial consequences from someone else's irresponsibility.

This guide demystifies UM/UIM coverage, explains its true value, addresses common misconceptions (including the "even if you're at fault" nuance), and empowers you to make informed decisions for better protection.

What Exactly Is Uninsured/Underinsured Motorist Coverage?

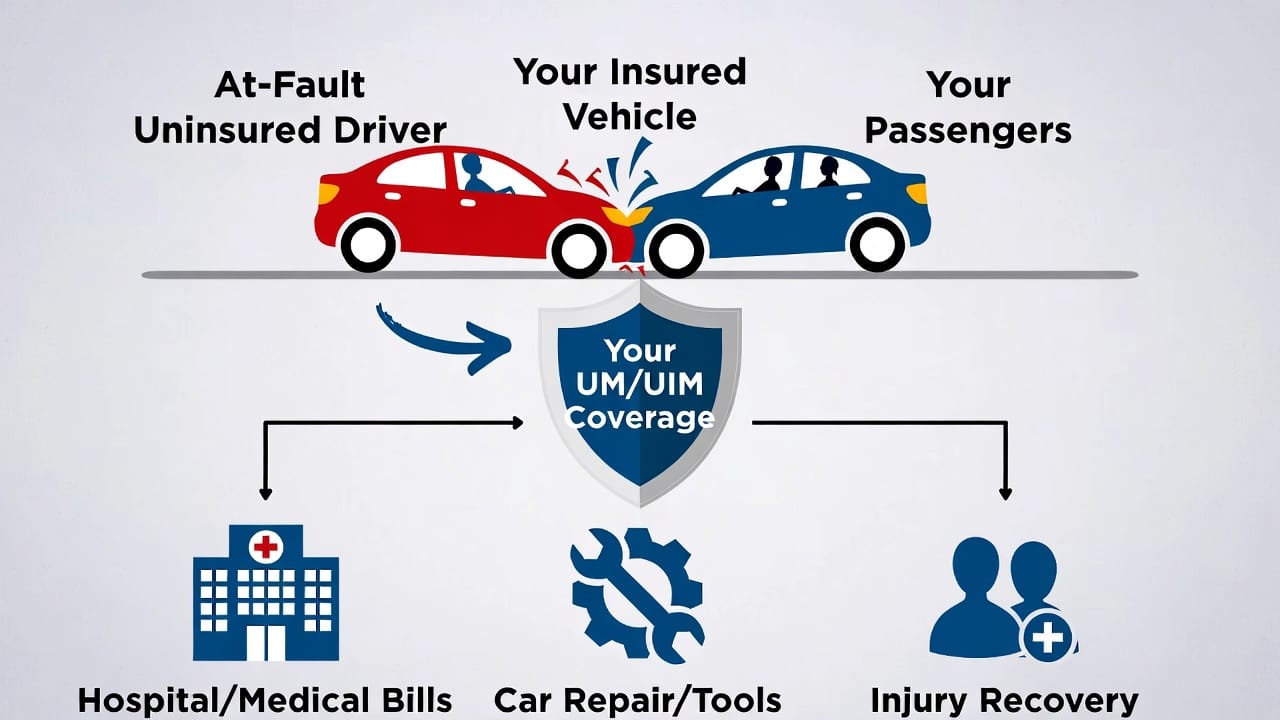

Uninsured Motorist (UM) coverage pays for your medical expenses, lost wages, pain and suffering, and—in many policies—vehicle repairs or replacement when you're involved in an accident caused by a driver with no insurance at all.

Underinsured Motorist (UIM) coverage kicks in when the at-fault driver's insurance limits are too low to fully cover your losses. For example, if their policy caps at $25,000 per person but your damages reach $100,000, UIM bridges the gap up to your chosen limits.

Together, UM/UIM acts as a stand-in for the liability coverage the other driver should have had. It's typically offered in bodily injury form (covering injuries to you and passengers) and sometimes property damage (though not all states require or allow this).

Key benefits include protection in scenarios such as:

- Being struck by an uninsured or underinsured driver.

- Hit-and-run accidents where the responsible party flees the scene (treated as uninsured in most states).

- Injuries sustained as a pedestrian or while riding as a passenger in someone else's vehicle (depending on policy and state rules).

This coverage follows you—the insured—in many cases, extending protection beyond just your own vehicle.

Clearing Up the Confusion: Does UM/UIM Apply When You're "At Fault"?

Here's where the puzzle often trips people up. UM/UIM coverage is designed for situations where another driver is primarily at fault but lacks sufficient (or any) insurance. It does not cover damages if you are the at-fault driver in a standard single-vehicle or your-fault accident.

However, the "sort of" in the title refers to nuanced, multi-vehicle scenarios:

- In rare comparative fault states, if you're partially at fault (e.g., 20% responsible) but the other driver is mostly at fault and uninsured/underinsured, UM/UIM may still apply to cover your share of damages after offsets.

- More commonly, it protects innocent passengers in your vehicle if you're hit by an uninsured driver—even if fault debates arise.

The bottom line: UM/UIM is your protection against others' lack of coverage. It doesn't excuse your own negligence but shields you from bearing the full burden when someone else fails to meet their legal responsibilities.

How UM/UIM Claims Actually Work in Real Life

When an accident occurs:

- Confirm the at-fault driver's status (no insurance, insufficient limits, or hit-and-run).

- Notify your insurer promptly and provide evidence (police report, photos, witness statements).

- Your policy's UM/UIM limits determine payout—often matching or close to your liability limits for balanced protection.

- In hit-and-run cases, most states treat the fleeing driver as uninsured, triggering coverage (though prompt reporting is essential).

- For pedestrians or non-occupied scenarios, coverage often extends if you're listed on the policy.

Important note: Always review your declarations page—UM/UIM is optional in many states but required in others. Choosing limits too low can leave significant gaps.

State Variations: Stacking and Other Rules

Auto insurance rules vary significantly by state, especially regarding stacking—the ability to combine UM/UIM limits from multiple vehicles or policies for higher available coverage.

In states that permit stacking, if you insure two vehicles with $100,000/$300,000 UM limits each, you could access up to $200,000 per person in severe cases. Other states restrict or prohibit stacking unless specifically elected (often at extra cost). Some treat inter-policy (multiple policies) and intra-policy (multiple vehicles on one policy) stacking differently.

Pedestrian and hit-and-run protections also differ—most states cover these under UM, but confirm locally.

Risks of Skipping or Underinsuring UM/UIM

Without adequate UM/UIM:

- Medical bills pile up quickly, even with health insurance gaps.

- Lost income from injuries can strain finances long-term.

- Vehicle replacement costs fall entirely on you in total losses.

- Hit-and-run victims face complete uncertainty without this layer.

The reassuring truth? Adding or increasing UM/UIM is often affordable compared to the risks—especially with rising uninsured rates.

Final Advice: Protect Yourself from the Unprotected

The roads are shared with millions of uninsured or underinsured drivers. Uninsured/underinsured motorist coverage isn't an optional luxury—it's essential financial armor for you, your passengers, and even your pedestrian self.

Review your policy today. Ensure your UM/UIM limits match or exceed your liability coverage for optimal protection. If you're unsure about your options, stacking rules in your state, or how to adjust coverage, reach out to a trusted insurance professional.

Peace of Mind on Every Drive – Get Covered Today