The Rideshare Insurance Gap: Protecting Uber and Lyft Drivers

In today’s fast-paced gig economy, millions of drivers rely on Uber and Lyft to earn reliable income while enjoying flexible schedules. Yet one critical risk often goes unnoticed until it’s too late: the rideshare insurance gap. This modern coverage challenge can leave even the most careful drivers exposed to massive financial and legal liabilities during everyday trips.

Protect Your Rides While You Drive – Call for Rideshare Insurance

At its core, the rideshare insurance gap exists because standard personal auto policies and the limited protections offered by rideshare platforms do not fully align during every moment a driver is active. Without the right solution, a single incident could jeopardize your savings, your vehicle, and your future driving career.

The good news? Rideshare endorsements close this gap completely. These specialized add-ons deliver seamless, comprehensive protection tailored to the unique demands of Uber and Lyft driving. In this authoritative guide, we explain exactly how the gap forms, the three critical periods of rideshare activity, and why adding a rideshare insurance endorsement is the smartest move any platform driver can make.

Why this matters more than ever

Rideshare driving has exploded since 2020. More families, professionals, and side-hustlers are logging in daily. Yet insurance rules have not kept pace with technology. Understanding your exposure—and filling it proactively—lets you focus on what you do best: delivering safe, friendly rides while building your income.

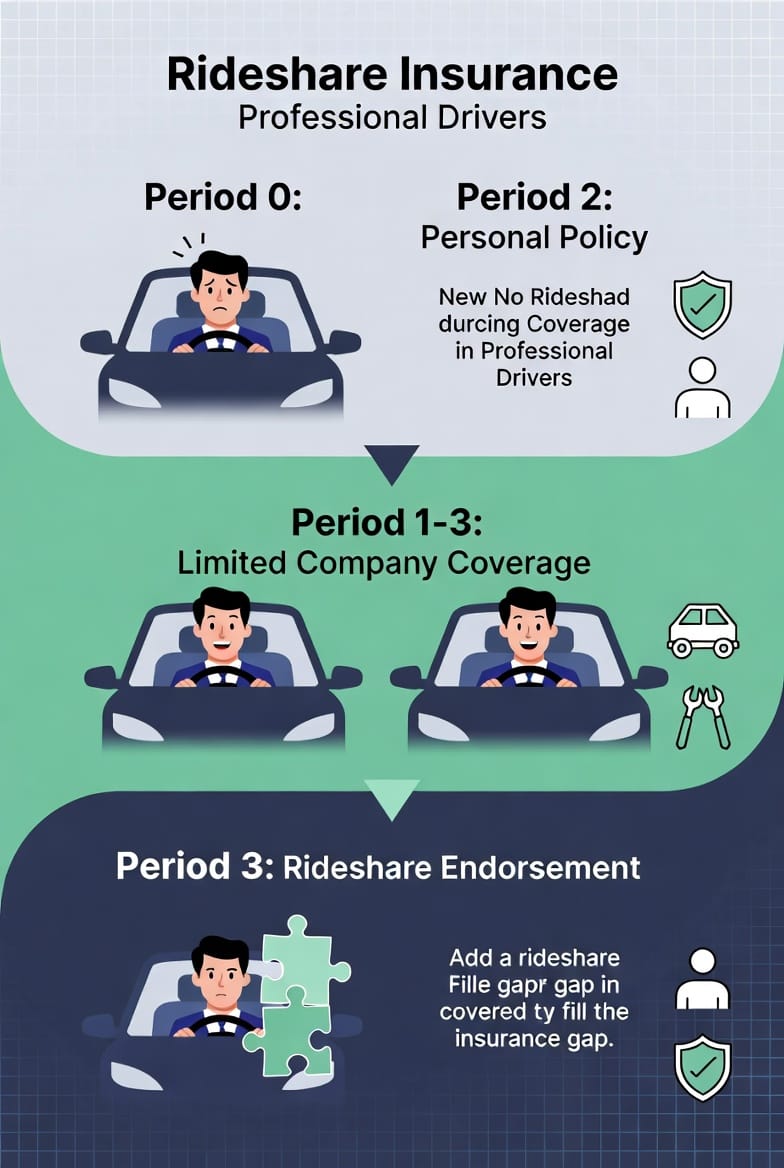

Understanding the Three Periods of Rideshare Driving

Rideshare companies and insurers divide every trip into distinct phases, each with different coverage responsibilities. Knowing these three periods is the first step toward protecting yourself.

- Period 0 – App Off (Personal Use Only): Your phone is not logged into the Uber or Lyft app. You are driving for personal errands, commuting, or simply parked. At this stage, your regular personal auto insurance policy remains fully active. This is the only time standard coverage applies without question.

- Period 1 – App On, Waiting for a Request: You have opened the app and are available for rides. No passenger has been matched yet. This is where the first coverage gap appears. Most personal policies explicitly exclude commercial use the moment you turn the app on, leaving you with little or no protection.

- Periods 2 and 3 – En Route to Pickup and With Passenger: Once a ride is accepted, you are either heading to the passenger or already transporting them. Rideshare companies provide contingent liability coverage during these windows, but it is limited in scope, has high deductibles in many cases, and often excludes physical damage to your own vehicle.

These periods create a dangerous mismatch. Your personal policy drops out exactly when the app activates, and the company’s backup coverage does not fully replace what you lose. The result? A rideshare insurance gap that can cost tens or even hundreds of thousands of dollars in an accident.

Bold reality check: An at-fault collision during Period 1 could leave you personally responsible for medical bills, vehicle repairs, and lawsuits—none of which your standard policy will touch.

Why Personal Auto Insurance Falls Short for Rideshare Drivers

Most drivers assume their existing policy “covers everything.” Unfortunately, that assumption is costly.

Personal auto insurers classify Uber and Lyft driving as commercial activity the instant the app turns on. Many policies contain clear exclusions for “for-hire” or “ridesharing” use. Even if you disclose your side gig, standard policies rarely extend the same limits or protections you enjoy during personal driving.

Key risks drivers face without additional coverage include:

- Liability exposure far beyond personal policy limits

- Zero coverage for your own vehicle (collision or comprehensive) while the app is active

- Denial of claims because the insurer discovers commercial use after an incident

- License and registration complications if an uncovered accident occurs

These are not theoretical dangers. Every day, unprotected drivers learn the hard way that “I thought I was covered” is not a defense in court or with repair shops.

How Rideshare Companies Provide Coverage—and Where the Gaps Remain

Uber and Lyft do offer insurance, but only during Periods 1–3 and only at minimum state-required liability levels in most markets. Their policies are contingent, meaning they activate only after your personal coverage ends.

Even during active rides, company coverage typically:

- Caps liability well below what a serious accident demands

- Excludes physical damage to your car entirely

- Leaves you responsible for any deductible or out-of-pocket costs

- Does not protect against uninsured motorists or comprehensive events like theft or vandalism while you are logged in

This partial safety net creates the exact rideshare insurance gap that leaves drivers vulnerable precisely when they are working.

Reassuring truth: You do not have to accept these limitations. A simple rideshare endorsement added to your personal policy bridges every gap, providing continuous, higher-limit protection from the moment you log in until you log off.

The Solution: Rideshare Insurance Endorsements That Deliver Real Protection

A rideshare insurance endorsement is the professional driver’s answer to the coverage gap. This specialized add-on, available through most major insurers, extends your personal policy to include commercial ridesharing use without forcing you to buy an expensive standalone commercial policy.

Once added, the endorsement seamlessly:

- Activates the moment your app turns on (Period 1)

- Supplements company coverage during Periods 2 and 3

- Restores full personal coverage when you log off (Period 0)

No more worrying about which period you are in. Protection is automatic, continuous, and tailored to your driving reality.

What Rideshare Endorsements Typically Cover

When you add this endorsement, you gain targeted protections that address the exact weaknesses in both personal and company policies.

- Gap liability coverage that steps in between your personal policy and the rideshare company’s limits

- Physical damage protection for your vehicle (collision and comprehensive) while logged in

- Higher liability limits that truly shield your assets in serious incidents

- Uninsured/underinsured motorist coverage that follows you during rideshare hours

- Medical payments or personal injury protection extended to commercial use

These coverages work together to create a safety net that feels invisible—until you need it. Then it becomes priceless.

Real Benefits Drivers Experience After Closing the Gap

Drivers who secure rideshare insurance report immediate peace of mind. They no longer second-guess every ping or hesitate to accept longer trips. Instead, they drive confidently, knowing that:

- Accidents are handled quickly and fairly

- Repair costs do not come out of their own pocket

- Legal defense is included at robust limits

- Their personal assets stay protected

Many also enjoy lower overall premiums because the endorsement is far more affordable than switching to full commercial insurance.

Before-and-after perspective: Before the endorsement, a fender-bender during a waiting period could mean thousands in uncovered repairs and weeks without income. After the endorsement, the same incident is resolved within days, with the driver back on the road earning money—stress-free.

Choosing the Right Rideshare Insurance Partner

Not all endorsements are created equal. Look for a provider that understands the gig economy, offers fast online quoting, and works with your existing personal policy rather than forcing a full rewrite.

Key questions to ask:

- Does the endorsement cover my specific city and state requirements?

- Are there any waiting periods or restrictions?

- Will my rates stay stable even as I log more miles?

The right partner makes the process simple, transparent, and reassuring from the first call.

Take Action Today – Fill Your Coverage Gap

Drive for Uber or Lyft? Do not leave your future to chance. The rideshare insurance gap is real, but it is also 100% preventable.

A quick conversation with an experienced agent can secure the endorsement you need and give you the confidence to keep driving safely and profitably.

Your next ride could be the one that proves how valuable full protection truly is. Protect yourself, protect your passengers, and protect the income you’ve worked hard to build. The solution is simple, affordable, and available right now.

Fill the Coverage Gap Instantly – Call Now for Peace of Mind