The Rental Reimbursement Rider: The Low-Cost Coverage That Saves You Money and Hassle After an Accident

In the aftermath of an auto accident, the last thing you want is to be without reliable transportation. While your comprehensive or collision coverage handles repairs to your vehicle, many drivers overlook a simple, affordable add-on that keeps you mobile: the rental reimbursement rider. Often called rental car reimbursement or transportation expense coverage, this optional endorsement provides daily payments for a rental vehicle while your car is in the shop due to a covered loss.

Protect Your Mobility with Rental Reimbursement – Free Quote Now

833) 498-1406

This often-overlooked coverage offers peace of mind and significant savings. For a modest annual premium—typically just $20 to $60 per year—it ensures you're never stranded. In this in-depth guide, we'll explain how rental reimbursement works, its real-world value (especially for single-vehicle households), why it's worth adding, and how to secure it today.

What Exactly Is Rental Reimbursement Coverage?

Rental reimbursement is an optional endorsement to your standard auto insurance policy. It reimburses you for the cost of a rental car (or alternative transportation like rideshares or public transit) when your vehicle is unusable due to a covered claim, such as:

- Collision damage from an at-fault or not-at-fault accident

- Comprehensive losses (theft, vandalism, hail, animal strikes)

- Certain other covered perils that require body shop repairs

Unlike liability coverage, this benefit applies regardless of fault in many cases, as long as the damage triggers a covered repair.

Key features include:

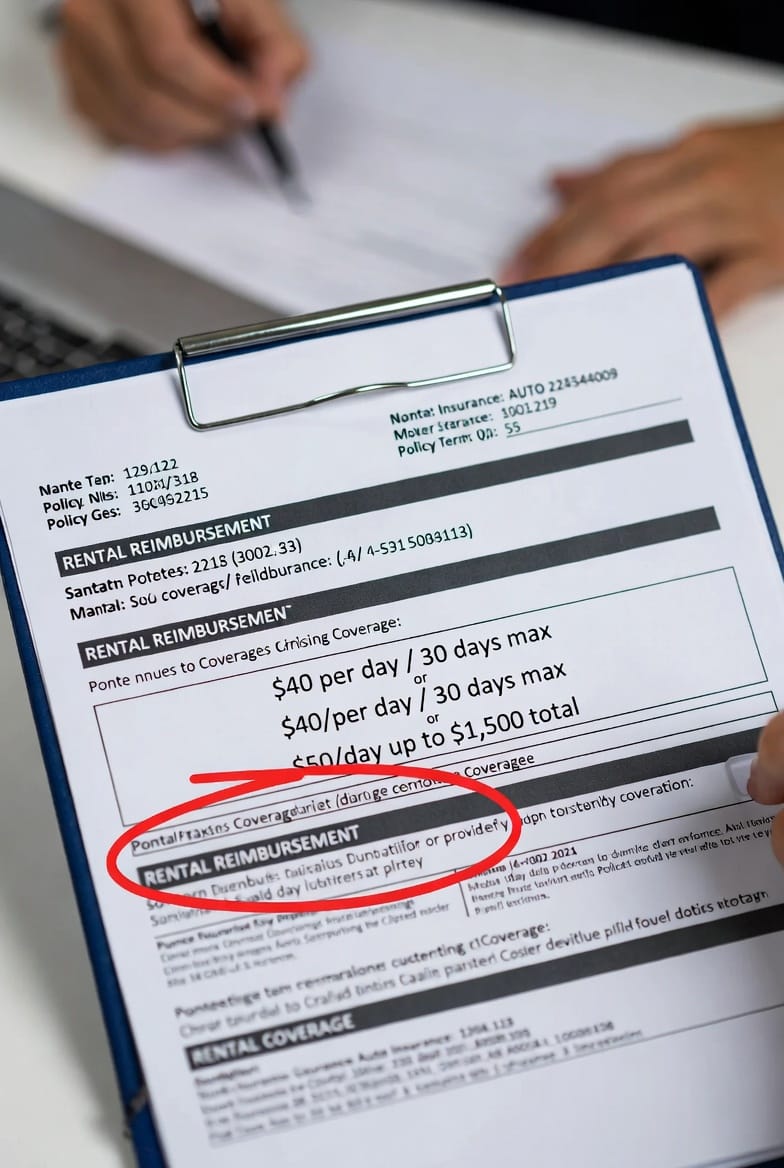

- Daily limit: Typically $30 to $70 per day (common options: $40/day, $50/day)

- Maximum duration or total payout: Often 30 days or a cap like $1,200 to $1,500 per claim

- Eligible expenses: Rental fees, taxes, and sometimes mileage or drop-off charges

This coverage bridges the gap during repairs, which average 10–14 days for moderate collisions but can extend longer for severe damage.

Why This Low-Cost Add-On Delivers High Value

The average daily rental car rate hovers around $50–$80, depending on location, vehicle type, and season. Without reimbursement, a two-week repair could cost you $700–$1,100 out of pocket—far more than the rider's yearly cost.

Consider these scenarios where rental reimbursement proves invaluable:

- No second vehicle: If your household relies on one car, being without wheels disrupts work, school runs, errands, and family life.

- Daily commuters: Missing work due to lack of transport can lead to lost wages or job risks.

- Unexpected long repairs: Modern vehicles with advanced safety features often require specialized parts and labor, extending shop time.

- Not-at-fault accidents: Even when another driver is responsible, their insurance may delay or limit rental assistance—your rider provides immediate backup.

For pennies a day, this coverage eliminates stress and maintains your routine. It's especially beneficial in urban areas with high rental costs or rural spots with limited alternatives.

How Rental Reimbursement Works in Practice

After a covered accident:

- File your claim with your insurer.

- Get your vehicle to an approved repair shop.

- Secure a rental car (your policy often partners with networks for discounted rates).

- Submit receipts for reimbursement up to your daily limit and total cap.

Most policies reimburse actual expenses up to the limit—no need to use a specific rental company unless specified.

Important note: Coverage typically starts when repairs begin and ends when your vehicle is drivable again or the limit is reached.

Understanding Coverage Limits and Choosing the Right Option

Insurers offer flexible tiers to match your needs:

- Basic: $30/day for 30 days (total ~$900) – sufficient for economy cars in lower-cost areas.

- Standard: $40–$50/day for 30–45 days (total $1,200–$1,500) – most popular choice balancing cost and protection.

- Enhanced: $60–$70/day or higher – ideal for families, SUVs, or high-rental-rate regions.

Higher limits cost slightly more but provide better protection against premium rentals or extended repairs. Review your policy declarations to confirm your exact limits—many drivers discover inadequate coverage only after an accident.

Pro tip: If you frequently rent cars for travel, pair this with your credit card's rental benefits for extra layers of protection.

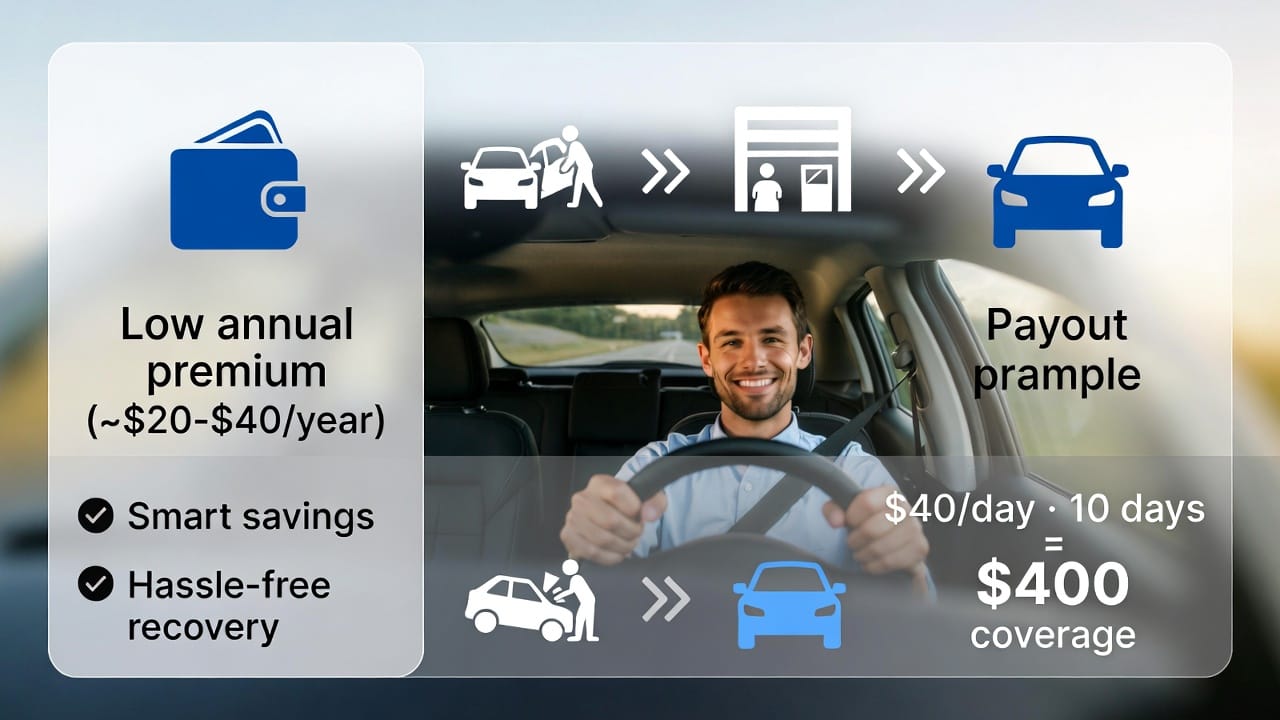

The True Cost: Minimal Premium for Maximum Convenience

Industry data shows rental reimbursement adds remarkably little to your premium:

- Average annual cost: $20–$60 per vehicle

- Often under $5/month

- Cheaper than one or two days of out-of-pocket rental fees

This small investment yields outsized returns. A single claim can reimburse $400–$1,000+, far exceeding the premium paid over years.

For households without backup vehicles, it's not just convenient—it's essential for maintaining financial stability and daily productivity.

Common Myths About Rental Reimbursement

Let's debunk a few misconceptions:

- Myth: "It's only for at-fault accidents."Fact: It applies to covered losses, including not-at-fault collisions.

- Myth: "My credit card covers rentals."Fact: Credit card benefits often exclude collision damage or have short durations—policy reimbursement is more comprehensive for repair scenarios.

- Myth: "It's too expensive."Fact: At pennies per day, it's one of the most cost-effective add-ons available.

Adding it during policy renewal or mid-term is simple and takes minutes.

When Rental Reimbursement Makes the Most Sense

This rider is particularly smart if you:

- Rely on a single vehicle

- Commute long distances or have inflexible schedules

- Live in areas with high rental car rates or limited public transit

- Own a vehicle prone to longer repair times (e.g., luxury, electric, or newer models)

Even multi-vehicle households benefit during simultaneous repairs or when one car is used primarily by a teen driver or spouse.

Final Thoughts: Protect Your Mobility for Pennies a Day

An accident disrupts life enough—don't compound it by losing your wheels. The rental reimbursement rider is a straightforward, low-cost way to stay mobile, avoid out-of-pocket expenses, and reduce stress during repairs.

For just a small addition to your premium, gain crucial peace of mind. Review your current policy today and consider upgrading your limits if needed.

Ready to add this essential coverage? Contact our team for a quick review and quote.

Don’t Let Repairs Leave You Without Wheels – Call Today