The Gap Insurance After Total Loss: Real-Life Example and Payout Explanation

In today’s fast-paced world of auto financing, gap insurance stands as one of the most practical yet often overlooked safeguards for new-car buyers. When life throws an unexpected curve—such as a serious accident that results in a total loss—standard comprehensive and collision coverage pays only the actual cash value (ACV) of your vehicle at the time of the incident. If you still owe more on your auto loan than that amount, you could be left with a painful financial gap.

Protect Yourself from Gap Loss – Call Now!

This article walks you through exactly how gap insurance after total loss works, using a realistic, real-life-style example based on current market realities. You’ll see the numbers, the emotional impact, and the clear protection it provides. By the end, you’ll understand why this coverage delivers genuine reassurance and financial security when it matters most.

Understanding Gap Insurance: Your Safety Net Against Negative Equity

Gap insurance, also known as Guaranteed Asset Protection, is designed specifically to cover the difference between what you owe on your car loan or lease and the actual cash value your primary insurer pays after a total loss or theft.

Unlike regular auto insurance, which focuses on repairing or replacing the vehicle’s market value, gap insurance steps in to eliminate negative equity—the situation where your loan balance exceeds the car’s worth. This gap often appears quickly because vehicles depreciate fastest in the first few years, while loan balances decline more slowly, especially with low down payments or extended terms.

Rest assured, gap insurance is not complicated. It activates only when your vehicle is declared a total loss, ensuring you walk away without owing money on a car you can no longer drive. Insurance professionals recommend it as standard best practice for most financed or leased vehicles.

Why New-Car Owners Face the Greatest Risk

Modern vehicles carry higher sticker prices, and many buyers finance 80–100 % of the purchase with terms stretching 72–84 months. Rapid depreciation, combined with added fees rolled into the loan, creates a perfect storm for negative equity.

Without gap coverage, a driver could face thousands of dollars in out-of-pocket costs even after a total loss claim is settled. This is not theoretical—it happens daily to responsible drivers who simply lacked the extra layer of protection. Gap insurance removes that burden, giving you confidence on the road and peace of mind at claim time.

Real-Life Scenario: A $35,000 New Car Meets an Unexpected Total Loss

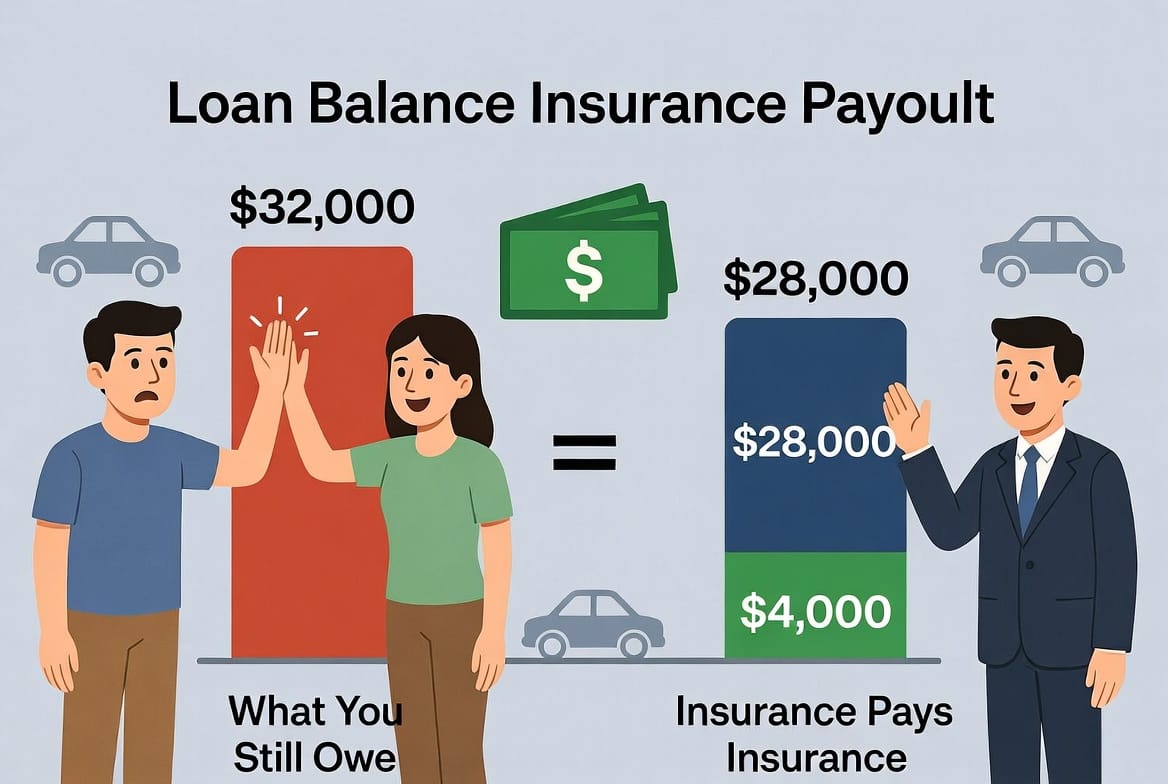

Meet Sarah and Mike, a young professional couple who purchased a new mid-size SUV for $35,000 exactly one year ago. They put down a modest $3,000 and financed the rest with a 72-month loan at a competitive rate. After twelve months of on-time payments, their outstanding loan balance stood at $32,000.

One rainy evening, another driver ran a red light and collided with their SUV. The damage was extensive. The insurance company promptly inspected the vehicle and declared it a total loss. Their primary auto policy paid the actual cash value of $28,000—a fair market amount reflecting one year of depreciation and mileage.

At first glance, the claim seemed settled. However, Sarah and Mike still owed $32,000 on a car they could no longer drive. That left a $4,000 shortfall. This is the exact moment gap insurance proved its worth. Their gap policy issued a check for the full $4,000 difference within days, bringing their loan balance to zero.

No more payments on a wrecked vehicle. No surprise balance due. Just closure and the ability to move forward—whether shopping for a replacement or adjusting their budget. This real-life example mirrors thousands of claims processed every month and shows why gap coverage is not an optional add-on but a smart financial decision.

How the Gap Insurance Payout Actually Works: Step-by-Step Breakdown

The process is straightforward and designed for speed:

- Total loss determination – Your primary insurer evaluates the repair cost versus the vehicle’s value and declares it totaled.

- ACV payout – They issue a check for the current actual cash value ($28,000 in our example).

- Gap calculation – Your gap provider compares the ACV against your current loan balance ($32,000).

- Coverage activation – The policy pays the exact difference ($4,000), satisfying the lender and closing the account.

This seamless coordination between your primary insurer and gap provider ensures you experience minimal stress during an already difficult time.

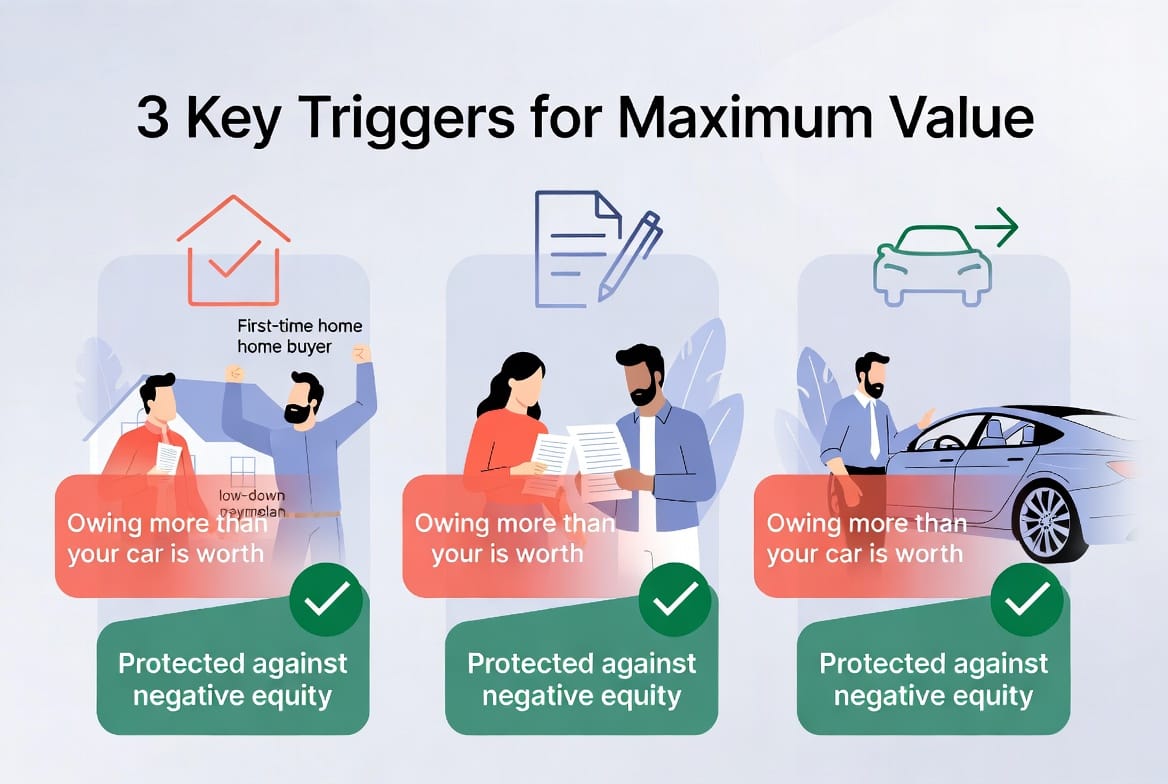

When Gap Insurance Delivers the Greatest Value

Gap coverage shines brightest in specific situations that create the largest potential shortfall. Consider these key scenarios:

- Low or zero down payment – When little equity is built upfront, the loan balance stays high even as the car depreciates.

- Long loan terms (60+ months) – Extended financing slows principal reduction while depreciation marches forward relentlessly.

- Rapidly depreciating models – Luxury vehicles, certain SUVs, and tech-loaded cars lose value fastest in the first 12–24 months.

- Purchases right off the lot – The steepest drop in value happens immediately after you drive away.

- Leased vehicles – Early termination fees plus residual value gaps make protection especially valuable.

In each case, gap insurance acts as the bridge that prevents financial hardship.

Additional Benefits and Smart Considerations

Beyond the financial payout, gap insurance offers intangible peace of mind. It lets you focus on recovery and family rather than spreadsheets. Many policies also cover your deductible or even temporary rental car expenses, adding extra layers of support.

When shopping, compare coverage limits and confirm whether the policy includes leased vehicles or has any exclusions. Reputable providers make the process simple and transparent.

Common Questions About Gap Insurance After Total Loss

Is gap insurance expensive?

Usually just a few dollars per month when added to your policy—far less than the potential thousands you could owe without it.

Can I buy it after purchase?

Yes, many insurers allow enrollment within the first 30–90 days, though adding it at financing is most convenient.

Does it replace my primary insurance?

No. Gap insurance works alongside your comprehensive and collision coverage, never instead of it.

Final Advice: Protect Yourself Before You Need It

Never risk owing money on a car you can no longer drive. A few moments of planning today can save you thousands and countless hours of stress tomorrow.

If you recently financed or leased a vehicle—or are about to—ask about gap insurance today. The team at our trusted partner is ready to review your situation and provide clear, personalized guidance.

Drive confidently knowing you’re fully protected. Gap insurance after total loss isn’t just smart—it’s the responsible choice that keeps your finances on track when life takes an unexpected turn.

Don’t Owe on a Totaled Car – Call for Gap Coverage