Discover the home business coverage gap that leaves most side hustles unprotected by standard homeowners insurance. Learn why liability, equipment, and inventory risks aren’t covered—and how simple endorsements or separate policies can safeguard your livelihood today.

Discover why standard homeowners insurance often denies claims for vacant homes after 30–60 days. Learn the hidden risks—vandalism, squatters, frozen pipes, undetected fires—and how vacant home insurance protects your investment when your house sits empty.Protect your property today.

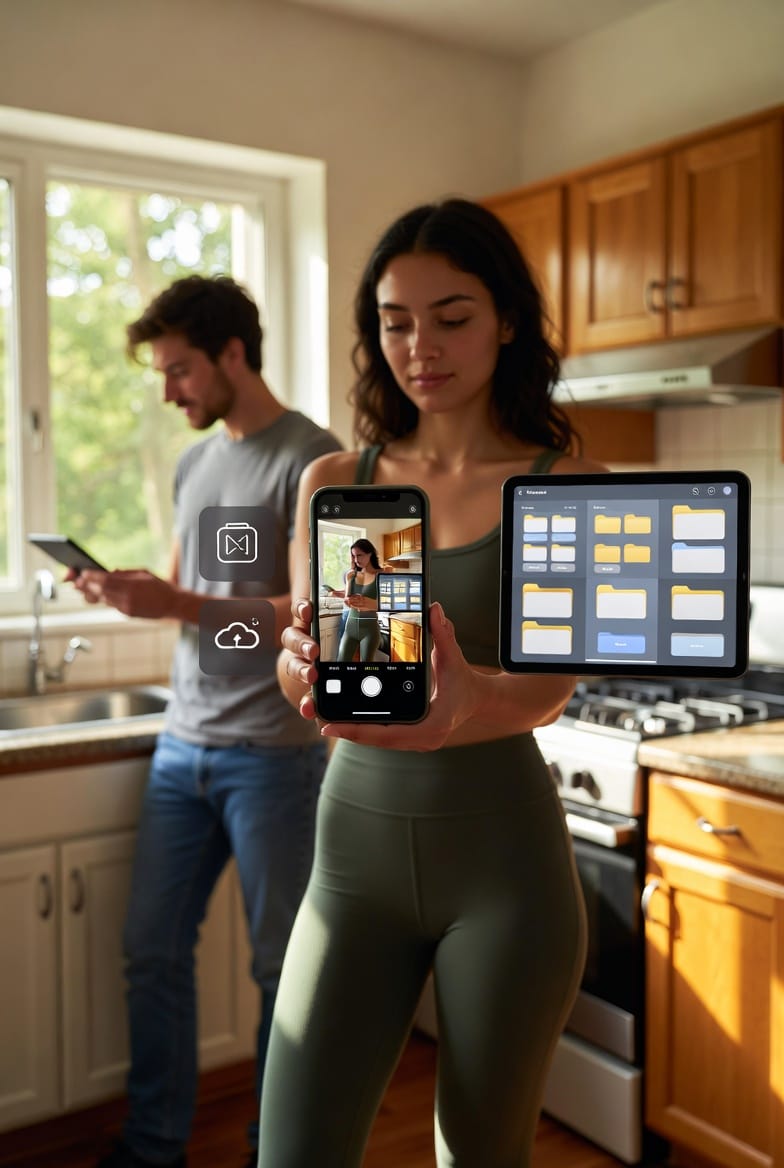

Protect your home and speed up insurance claims with a home inventory app! Use Encircle or Sortly to photograph belongings, add videos, categorize items, and store securely in the cloud. Document today for faster, fuller payouts tomorrow.

Most homeowners policies offer little to no coverage for home-based business equipment, inventory, or liability. Explore the gaps, Incidental Business endorsements, and why a Business Owners Policy (BOP) is often essential to protect your side hustle or full-time venture.

Discover why standard home and auto insurance limits ($300K) aren't enough for major lawsuits. Explore real cases—dog bites, pool accidents, serious crashes—and how a personal liability umbrella policy delivers affordable millions in extra protection to safeguard your assets and future.