Gaps in the Garage: How Ridesharing, Gig Work, and New Car Tech Affect Your Auto Coverage

In today's fast-paced world, your car isn't just a mode of transportation—it's a gateway to income, innovation, and independence. But as ridesharing, gig work, and cutting-edge vehicle technologies evolve, so do the risks to your auto coverage. Traditional personal auto policies, designed for everyday commuting, often fall short in addressing these modern realities. Whether you're ferrying passengers via Uber, delivering meals through DoorDash, or cruising in a leased electric vehicle (EV) equipped with advanced driver-assistance systems (ADAS), understanding the gaps in your garage is crucial. This guide explores how these elements impact your insurance, offering practical insights to keep you protected. Rest assured, with the right adjustments, your policy can adapt seamlessly to your lifestyle.

Rideshare, Delivery & Tech-Ready Insurance – Call Us

The Evolution of Driving in the Gig Economy

The gig economy has transformed how millions earn a living, with platforms like Lyft, Instacart, and Postmates turning personal vehicles into revenue generators. However, this shift introduces complexities that standard auto insurance might not anticipate. Personal policies typically cover recreational or commuting use, but when your car doubles as a business tool, coverage boundaries blur.

Consider the core scenarios:

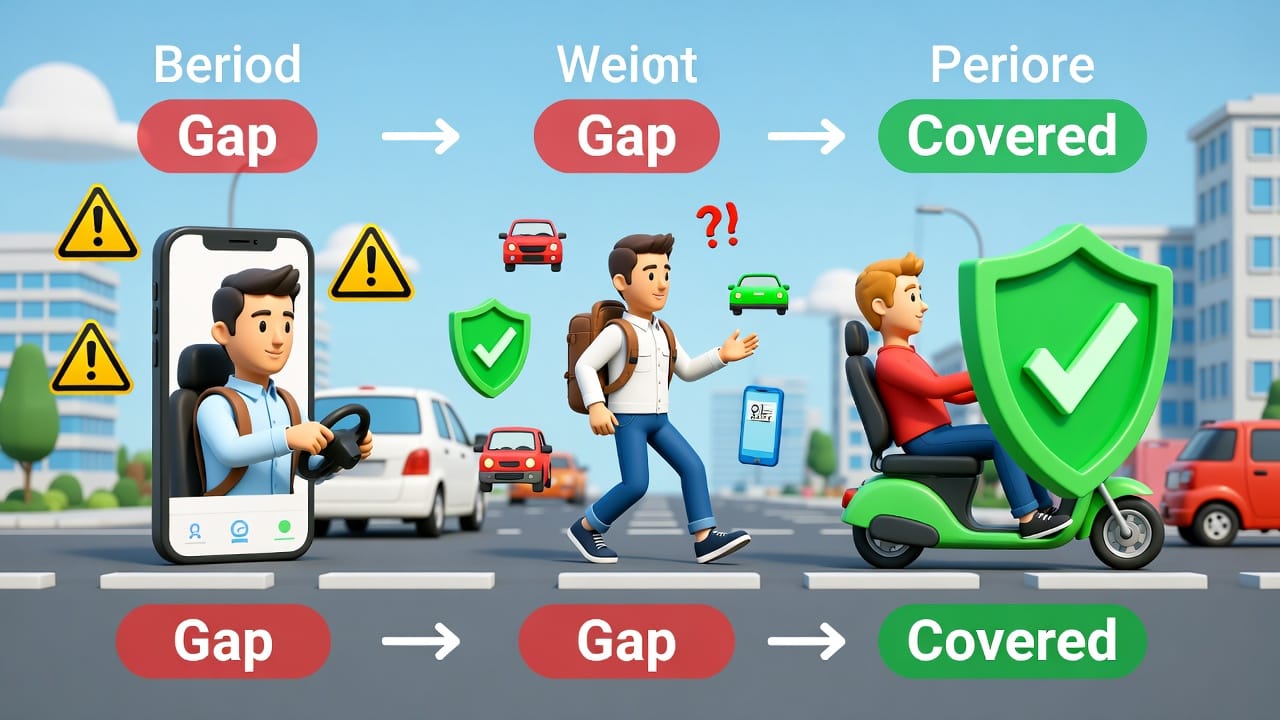

- Ridesharing Activities: Apps like Uber divide operations into three periods. Period 1 occurs when the app is off—your personal policy usually applies here as normal driving.

- Gig Delivery Driving: Similar to ridesharing, delivering packages or food involves periods of waiting and active transport, where personal coverage may lapse.

The key risk? Many drivers assume their existing policy suffices, only to discover exclusions during claims. But don't worry—specialized endorsements can bridge these divides, ensuring you're not left vulnerable.

Unpacking Ridesharing Coverage Periods

To navigate ridesharing insurance effectively, it's essential to break down the three distinct periods defined by most platforms:

- Period 1: App Off: This is your baseline personal driving time. Standard auto policies generally provide full liability, collision, and comprehensive coverage, treating it as non-commercial use.

- Period 2: App On, Waiting for a Ride: Here's where the coverage gap often emerges. With the app active but no passenger en route, you're in a limbo state. Personal auto policies typically exclude this phase, viewing it as commercial intent. Without a rideshare endorsement, an accident could result in denied claims, leaving you liable for damages, medical bills, or legal fees.

- Period 3: Passenger or Delivery in Progress: Once a ride or delivery is accepted, platform-provided insurance kicks in, often including higher liability limits. However, this doesn't negate the need for your own policy to fill in deductibles or additional protections.

Why does Period 2 pose such a threat? Insurers classify it as business use, which isn't covered under personal plans. According to industry data, accidents during this waiting phase account for a significant portion of uninsured claims among gig workers. The solution lies in adding a rideshare endorsement or hybrid policy, which extends coverage seamlessly across all periods. These affordable add-ons—often just $10-20 monthly—provide peace of mind, allowing you to focus on earning without fear.

Gig Work: Beyond Ridesharing to Deliveries and More

Gig work extends far beyond passenger transport. Food delivery, grocery runs, and even freelance courier services via apps like Amazon Flex rely on your vehicle. Yet, personal auto coverage rarely accounts for these activities. For instance, if you're en route to pick up an order (akin to Period 2), a fender-bender could expose you to out-of-pocket expenses.

Key considerations include:

- Vehicle Wear and Tear: Frequent stops and idling accelerate depreciation, which standard policies might not reimburse.

- Cargo Risks: Delivering valuables? Comprehensive coverage may exclude business-related theft or damage.

- Liability Exposure: Interacting with customers increases slip-and-fall or injury claims not covered personally.

Fortunately, options like business use endorsements or commercial auto policies tailored for gig workers can mitigate these. These ensure that whether you're dashing for DoorDash or shuttling for Shipt, your insurance aligns with your hustle. Always review your policy declarations page for exclusions—proactive steps like this empower you to drive confidently.

The Impact of Advanced Driver-Assistance Systems (ADAS)

As vehicles grow smarter, ADAS technologies—think lane-keeping assist, automatic emergency braking, and adaptive cruise control—promise safer roads. However, they also complicate auto insurance claims and repairs. Insurers must account for the high cost of recalibrating sensors post-accident, which can exceed $1,000 even for minor incidents.

Common challenges:

- Repair Costs: ADAS-equipped cars often require original equipment manufacturer (OEM) parts to maintain functionality. Aftermarket alternatives might void warranties or impair safety features, leading to denied claims.

- Liability Shifts: If an ADAS malfunction contributes to an accident, determining fault becomes tricky. Was it driver error, software glitch, or sensor failure?

- Premium Adjustments: Vehicles with ADAS may qualify for discounts (up to 10-15%) due to reduced accident risks, but only if your policy recognizes these features.

For leased vehicles, where you're not the owner, ensuring the policy covers replacement value is vital. Discuss with your agent about endorsements for ADAS repairs—these specify OEM usage and cover calibration, safeguarding your investment. Rest easy knowing that staying informed keeps your coverage as advanced as your car.

Electric Vehicles: Leasing and Specialized Coverage Needs

The surge in electric vehicles (EVs) brings eco-friendly perks, but leasing an EV introduces unique insurance nuances. Unlike traditional gas cars, EVs feature high-voltage batteries and specialized components that demand tailored protection.

Essential factors:

- Battery Coverage: Standard policies might not fully insure battery replacement, which can cost $5,000-$20,000. Look for EV-specific endorsements that include this.

- Charging Equipment: Home chargers or public station damages? Comprehensive coverage extensions can protect against theft, vandalism, or electrical surges.

- Leasing Gaps: Leased EVs often require gap insurance to cover the difference between depreciated value and lease payoff in total-loss scenarios.

- Range and Roadside Assistance: EVs' limited range heightens breakdown risks—enhanced towing coverage ensures you're not stranded.

With rising EV adoption, insurers are adapting, offering bundles that address these. For instance, some policies now include rental reimbursement for alternative transport during battery repairs. By opting for leased EV coverage, you align your policy with sustainable driving, minimizing financial shocks.

Questions to Ask Your Insurance Agent

To customize your policy, arm yourself with targeted inquiries. This proactive approach turns potential vulnerabilities into strengths:

- What rideshare or gig work endorsements are available to cover Period 2 gaps?

- Does my policy mandate OEM parts for ADAS repairs, and what calibration costs are included?

- For leased EVs, how does special EV coverage handle battery replacement and gap protection?

- Are there discounts for ADAS features or EV safety ratings?

- How can I add business use without switching to full commercial insurance?

These questions foster a dialogue that refines your coverage, ensuring it evolves with your needs.

Bridging the Gaps: Final Thoughts

Modern driving realities— from ridesharing and gig work to ADAS and leased EVs—demand agile auto insurance. By recognizing Period 2 exclusions, prioritizing OEM repairs, and securing EV-specific protections, you fortify your policy against unforeseen risks. Remember, insurance isn't static; it's a partner in your dynamic life. With expert guidance, you'll drive forward securely, no gaps in sight.

Keep Pace with Your Driving Life – Call Specialists Now