Understanding Your Deductible: How This Critical Number Affects Your Premium and Your Claim Payout

When it comes to home insurance, one of the most pivotal elements influencing both your monthly costs and your peace of mind during a crisis is the deductible. This seemingly straightforward number represents the amount you agree to pay out-of-pocket before your insurance coverage kicks in for a claim. Understanding how your deductible works isn't just about crunching numbers—it's about tailoring your policy to fit your financial reality and protecting your home effectively. In this comprehensive guide, we'll explore the direct relationship between your deductible and your premium, break down real-world examples, and provide actionable advice to help you strike the perfect balance. Whether you're a first-time homeowner or reviewing your existing policy, rest assured that making informed choices can lead to significant savings and security.

Maximize Coverage, Minimize Costs – Call for a Free Review

What Is a Home Insurance Deductible?

At its core, a deductible is the threshold you must meet financially before your insurer steps in to cover the remaining costs of a covered loss. Think of it as your share of the risk in the insurance agreement. Most standard homeowners insurance policies include deductibles for perils like fire, theft, windstorms, and hail, though some events (such as earthquakes or floods) may require separate policies with their own deductibles.

There are two main types of deductibles to consider:

- Dollar-amount deductibles: A fixed sum, such as $1,000, that applies to most claims.

- Percentage-based deductibles: Common for high-risk areas prone to hurricanes or earthquakes, calculated as a percentage of your home's insured value (e.g., 2% of a $300,000 home equals a $6,000 deductible).

Choosing the right type and amount is crucial because it directly impacts your premium—the regular payment you make to keep your policy active. Higher deductibles typically mean lower premiums, as you're assuming more initial risk, which reduces the insurer's potential payout frequency and amount.

The Inverse Relationship: Deductibles and Premiums Explained

The connection between your deductible and premium is straightforward yet powerful: as one goes up, the other goes down. Insurers view a higher deductible as a sign that you're less likely to file small claims, which keeps their administrative and payout costs lower. In turn, they reward you with reduced premiums.

For instance, if you're insuring a $250,000 home with standard coverage:

- A low deductible of $500 might result in an annual premium around $1,200–$1,500, depending on your location, home age, and other factors.

- Bumping it to a higher deductible of $2,500 could slash that premium to $900–$1,100, potentially saving you $300–$400 per year.

This trade-off is reassuring because it empowers you to customize your policy. If you're in a stable financial position with emergency savings, opting for a higher deductible can free up budget for other priorities. Conversely, if unexpected expenses could strain your finances, a lower deductible provides a safety net, even if it means slightly higher monthly payments.

SEO Tip: Searching for "how deductibles affect home insurance premiums"? You're in the right place—let's dive deeper with examples.

Real-World Examples: Deductibles in Action

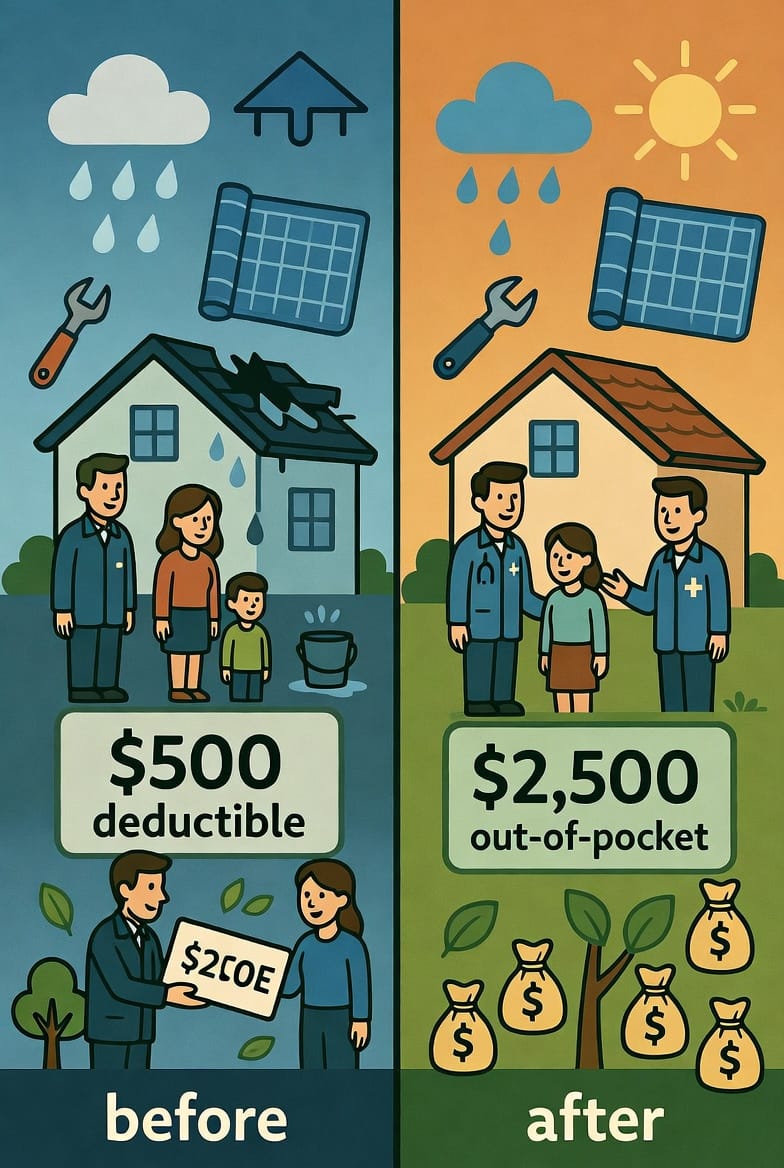

To illustrate the impact, let's examine a common scenario: a $10,000 claim for roof damage from a severe storm. We'll compare a $500 deductible versus a $2,500 deductible, assuming the same policy limits and coverage.

Scenario 1: $500 Deductible

- Out-of-pocket cost: You pay $500 upfront.

- Insurer payout: $9,500 (total claim minus deductible).

- Net to you: $9,500, allowing quick repairs with minimal financial hit.

- Premium implication: Higher ongoing costs, but ideal for those who prefer predictability.

Scenario 2: $2,500 Deductible

- Out-of-pocket cost: You cover $2,500.

- Insurer payout: $7,500.

- Net to you: $7,500, requiring more personal funds but offset by lower premiums over time.

- Premium implication: Savings of 20–30% on annual premiums, compounding to thousands over years.

In both cases, the claim is covered, but the choice affects your immediate cash flow. For a family facing a sudden roof leak, the lower deductible means faster recovery without dipping deeply into savings. However, if you've built a robust emergency fund, the higher option builds long-term savings on premiums—potentially enough to cover multiple deductibles if needed.

Consider this: Over five years, the premium savings from a $2,500 deductible might total $1,500–$2,000. If no claims occur, that's pure profit in your pocket. But if a claim hits, you're prepared because you've planned accordingly.

Factors Influencing Your Deductible Choice

Selecting the ideal deductible isn't one-size-fits-all—it's about aligning with your unique circumstances. Here are key considerations to guide you:

- Financial Stability: Assess your savings. If you have at least 3–6 months of expenses in an emergency fund, a higher deductible (e.g., $1,000–$5,000) can be a smart move to lower premiums.

- Claim History: Frequent small claims? A lower deductible minimizes out-of-pocket surprises. Infrequent claims? Go higher to save.

- Home Value and Location: In high-risk areas for natural disasters, percentage-based deductibles can spike costs—factor in local weather patterns.

- Policy Add-Ons: Some insurers offer deductible waivers for large claims or no-claim bonuses, softening the blow.

- Age and Condition of Home: Older homes may face more repairs, making a moderate deductible balanced.

By evaluating these, you can avoid common pitfalls like underinsuring (too high a deductible without savings) or overpaying (low deductible with unnecessary premiums).

Pros and Cons of Low vs. High Deductibles

To make it clearer, let's weigh the advantages and drawbacks:

Low Deductible (e.g., $500–$1,000)

- Pros:

- Lower out-of-pocket during claims.

- Easier budgeting for unexpected events.

- Peace of mind for risk-averse homeowners.

- Cons:

- Higher annual premiums.

- Potential for rate hikes if claims are filed often.

High Deductible (e.g., $2,500–$5,000+)

- Pros:

- Significant premium reductions.

- Encourages careful home maintenance to avoid small claims.

- Long-term savings for financially secure individuals.

- Cons:

- Larger upfront costs in emergencies.

- Risk of financial strain without adequate savings.

Ultimately, the "right" choice builds confidence in your coverage. Many homeowners find a sweet spot around $1,000–$2,000, offering a blend of affordability and protection.

How to Calculate Potential Savings and Risks

Armed with examples, you can project your own scenarios. Use this simple formula for a claim:

Net Payout = Claim Amount - Deductible

For premiums, request quotes from multiple insurers to compare. Tools like online calculators can estimate: Input your home details, and see how adjusting the deductible shifts costs. Remember, small premium savings add up—$200 yearly equals $2,000 in a decade.

Risk-wise, never set a deductible higher than you can comfortably afford. It's authoritative advice: Prioritize liquidity over savings if your budget is tight.

Common Myths About Deductibles Debunked

Misconceptions can lead to poor decisions—let's set the record straight:

- Myth: Higher deductibles mean less coverage. Fact: Coverage limits remain the same; only your initial share changes.

- Myth: Deductibles apply to every claim type. Fact: Some policies exclude certain perils or have separate deductibles.

- Myth: You can't change your deductible mid-policy. Fact: Most allow adjustments at renewal, often without penalties.

- Myth: Low deductibles are always safer. Fact: They can inflate premiums unnecessarily if you're low-risk.

Knowledge dispels fear—rest assured, understanding these empowers better protection.

Steps to Choose and Adjust Your Deductible

Ready to optimize? Follow this authoritative roadmap:

- Review Your Current Policy: Check your declarations page for existing deductible and premium.

- Assess Your Finances: Calculate affordable out-of-pocket maximums.

- Get Multiple Quotes: Compare from at least three insurers.

- Consult an Expert: Discuss with an agent for personalized insights.

- Monitor Annually: Life changes? Adjust accordingly.

This process ensures your home insurance evolves with you.

The Bigger Picture: Deductibles in Comprehensive Home Protection

Beyond numbers, your deductible fits into broader risk management. Pair it with preventive measures like home security systems or roof inspections to reduce claim likelihood, potentially qualifying for premium discounts. In high-risk zones, consider endorsements for specific deductibles.

Ultimately, a well-chosen deductible enhances resilience—turning potential disasters into manageable events.

Final Thoughts: Empower Your Insurance Decisions

Mastering your deductible is key to balancing costs and coverage in home insurance. With clear examples like the $10,000 roof claim, you see how $500 vs. $2,500 choices ripple through your finances. By aligning with your savings and risk tolerance, you gain control and confidence.

Balance Premiums & Payouts Perfectly – Call for Personalized Advice