The Water Backup Coverage: Protecting Against Sewer and Sump Pump Failures

When heavy rains overwhelm your neighborhood or your sump pump suddenly stops working, the last thing you want is to discover that your standard homeowners insurance leaves you exposed. Water backup coverage stands as one of the most critical yet often overlooked endorsements you can add to your home insurance policy. It delivers targeted protection against the costly and disruptive damage caused by sewer line backups and sump pump failures—events that occur more frequently than most homeowners realize.

Protect Your Basement from Sewer & Sump Pump Failures – Call Now

At its core, this coverage bridges a dangerous gap that leaves thousands of families facing unexpected financial hardship every year. In this comprehensive guide, we explain exactly what water backup coverage includes, why it is excluded from standard policies, the typical limits available, and how it provides genuine peace of mind. Whether you own a newer home with a finished basement or an older property with aging sewer lines, understanding this endorsement empowers you to safeguard your biggest investment.

Water backup coverage is not optional luxury insurance; it is practical, essential protection that restores your home quickly and keeps your finances secure. Let’s walk through everything you need to know so you can make an informed decision with confidence.

Understanding Water Backup Coverage

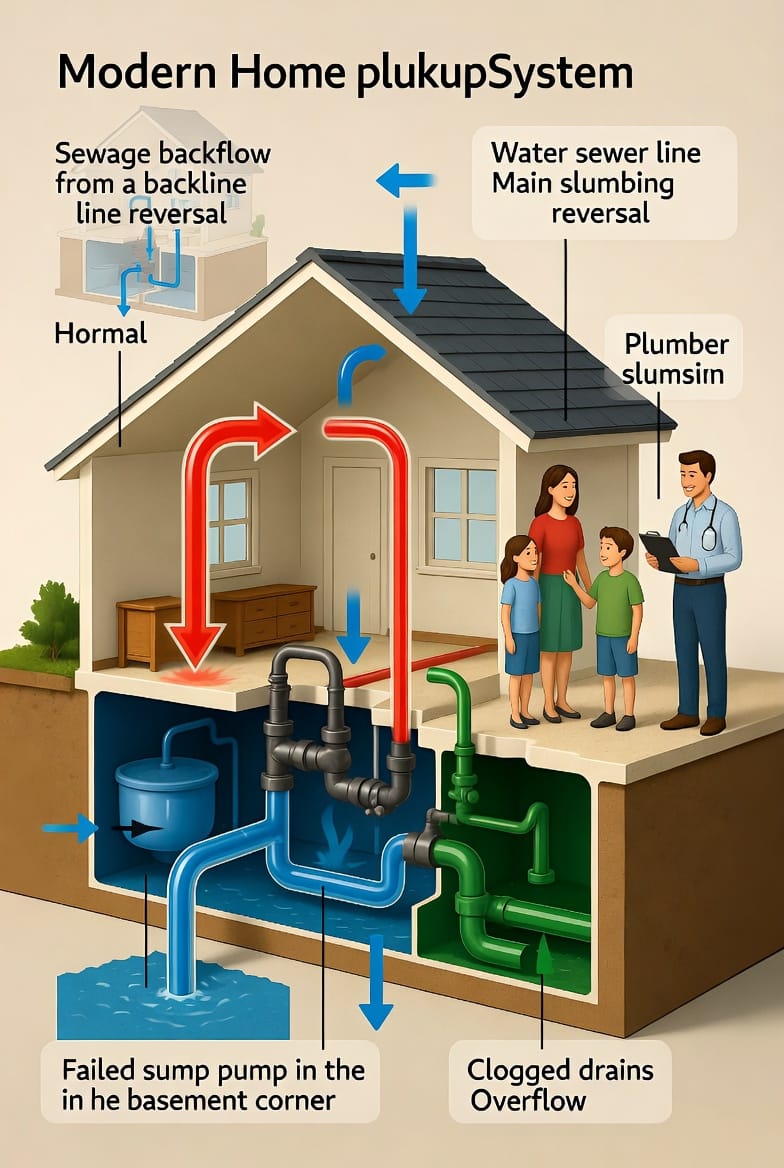

Water backup coverage is a specific endorsement you add to your existing homeowners insurance policy. It responds when water or sewage enters your home through the drain, sewer, or sump system rather than from external flooding or sudden internal plumbing leaks.

Unlike flood insurance, which addresses rising surface water from rivers or storms, water backup coverage focuses on the reverse flow of water already inside your property’s plumbing network. This distinction matters because many homeowners mistakenly believe their standard policy handles every water-related claim.

When you purchase this coverage, your insurer agrees to pay for repairs, cleanup, and replacement of damaged personal belongings up to the selected limit. The endorsement typically activates for sudden and accidental events such as a city sewer main clog forcing sewage into your basement or a mechanical sump pump failure during a power outage. Because the coverage is added by endorsement, you control the limit and deductible that best fit your budget and risk profile.

Homeowners who add water backup coverage report sleeping easier during storm season, knowing their policy stands ready to respond. The endorsement transforms a potentially devastating financial blow into a manageable insurance claim handled by professionals who prioritize your family’s safety and your home’s swift return to normal.

Why Standard Homeowners Policies Exclude It

Standard homeowners insurance policies are carefully designed to cover sudden and accidental perils such as fire, wind, or burst pipes inside your walls. However, they deliberately exclude sewer line backups and sump pump failures for two primary reasons.

First, these events often result from gradual wear, tree root intrusion, or municipal infrastructure issues beyond the homeowner’s control. Insurers classify them as “maintenance-related” or “external system failures” rather than sudden internal accidents. Second, the potential for widespread claims during heavy rainfall events makes these perils actuarially expensive without a separate rating and premium.

This exclusion surprises many policyholders at the worst possible moment. After a sump pump failure floods a finished basement containing family heirlooms and electronics, the claim denial letter arrives with a clear statement: “Damage from water backup or sewer overflow is not covered under your current policy.” The financial impact can reach tens of thousands of dollars in structural repairs, mold remediation, and lost belongings.

Fortunately, the insurance industry offers a straightforward solution. By adding the water backup coverage endorsement, you close this gap completely. The process is simple, the cost is reasonable, and the protection is immediate upon approval. You maintain full control while gaining the reassurance that your home—and your family’s financial future—remains protected.

Common Water Backup Scenarios

Understanding the most frequent triggers helps you recognize when water backup coverage becomes essential. Here are the top scenarios homeowners face:

- Sewer line reversal occurs when heavy rain overwhelms municipal systems, forcing sewage back through your home’s drains and into basements or ground-floor bathrooms.

- Sump pump failure strikes during power outages or when the pump motor burns out, allowing groundwater to rise unchecked through the sump pit.

- Drain overflow happens when leaves, grease, or debris clog interior lines, causing sinks, showers, or washing machines to back up and spill onto floors.

- Combined sewer and storm drain overload creates sudden pressure that pushes contaminated water into older homes lacking backflow preventers.

Each scenario shares one common thread: the water originates from within the plumbing or drainage system rather than outside the foundation. Without dedicated coverage, repair bills escalate quickly. Structural drying, flooring replacement, drywall removal, and professional mold treatment can easily exceed $15,000–$50,000 depending on the home’s size and finish level.

Water backup coverage responds efficiently in every case. Claims adjusters arrive promptly, authorize emergency mitigation within hours, and coordinate with trusted restoration contractors so your family returns to a safe, dry home as quickly as possible.

What Water Backup Coverage Typically Includes

When you activate water backup coverage, your policy responds with comprehensive benefits tailored to restore your home and belongings. Coverage usually pays for:

- Removal of contaminated water and sewage

- Professional cleaning and sanitizing of affected areas

- Replacement of damaged drywall, insulation, flooring, and cabinetry

- Repair or replacement of personal property damaged by the backup

- Temporary living expenses if your home becomes uninhabitable during restoration

- Prevention of secondary damage such as mold growth

Many insurers also include limited coverage for the cost to repair or replace the failed sump pump itself when the endorsement is active. This additional benefit prevents the same failure from recurring and demonstrates the policy’s focus on long-term protection.

Limits typically range from $5,000 to $100,000 or more, allowing you to match coverage to your home’s value and contents. Deductibles remain low—often $250 or $500—making claims accessible when you need them most. Because the endorsement is added to your existing policy, there is no separate application process or lengthy underwriting; most carriers approve it instantly for eligible homes.

Who Needs Water Backup Coverage Most?

Certain homes face elevated risk and benefit immediately from adding this endorsement. Consider these common profiles:

- Homes with finished basements containing bedrooms, home offices, or entertainment areas

- Properties built before 1980 with older sewer lines prone to root intrusion or collapse

- Residences equipped with sump pumps in areas with high water tables or frequent heavy rainfall

- Townhomes or properties sharing sewer laterals with neighbors

- Any home located in a region with aging municipal infrastructure

If your property matches any of these descriptions, water backup coverage is not optional—it is essential protection. The endorsement delivers confidence that a single storm or mechanical failure will not derail your family’s financial goals or force unwanted compromises.

Coverage Limits, Costs, and Options

Most carriers offer water backup coverage in increments of $10,000, $25,000, $50,000, or $100,000. Annual premiums typically range from $15 to $75 depending on your chosen limit, location, and home age. For many families, the cost equals less than a single monthly streaming subscription yet provides coverage worth tens of thousands of dollars.

You can increase limits at any policy renewal or mid-term if your needs change—such as after finishing a basement or installing a new sump pump. Some insurers also bundle water backup coverage with other valuable endorsements like service line protection or equipment breakdown coverage, creating a comprehensive shield at a competitive price.

The Peace of Mind and Financial Benefits

Choosing water backup coverage delivers more than financial reimbursement. It restores your sense of security during unpredictable weather. Claims are handled by experienced professionals who understand the urgency of water damage and prioritize health, safety, and speed. Families report that the endorsement turns a nightmare scenario into a manageable inconvenience resolved within days rather than months.

The long-term savings become evident when you compare the modest annual premium against the average $25,000+ cost of an uninsured backup claim. Protecting your equity, your health, and your family’s stability makes this one of the smartest insurance decisions a homeowner can make.

Preventive Measures That Complement Coverage

While water backup coverage stands ready when needed, smart homeowners also take these simple steps to reduce risk:

- Install battery backup systems for sump pumps

- Schedule annual sewer line camera inspections

- Keep trees away from underground sewer laterals

- Avoid flushing wipes or pouring grease down drains

- Test sump pumps monthly and replace aging units proactively

Combining prevention with proper insurance creates a powerful defense that keeps your home dry and your wallet protected.

Secure Your Home Against the Unexpected

Water backup coverage represents one of the most valuable endorsements available today. It addresses a critical exclusion in standard homeowners insurance, protects against sewer line backups and sump pump failures, and delivers fast, professional restoration when every minute counts.

Our licensed agents are ready to review your current policy, explain exact options for your home, and secure the protection you deserve—quickly, confidently, and at a price that fits your budget.

Your home is your sanctuary. Protect it completely with water backup coverage and enjoy peace of mind that only comes from knowing you are truly covered.

Avoid Costly Flood Damage – Add Water Backup Protection Now