The Roof Age and Insurance: When Insurers Require Replacement

Roof age stands as one of the most critical yet often overlooked underwriting factors in home insurance policies across the United States. Insurers scrutinize it closely because an aging roof directly influences the risk of water damage, structural issues, and costly claims. If your roof is approaching or exceeding 15 to 20 years old, you may face stricter coverage requirements, higher premiums, or even policy non-renewal.

Get Your Roof Insurance-Ready – Call Now!

The good news? Understanding this factor empowers you to take proactive steps that protect both your home and your wallet. In this comprehensive guide, we explore exactly how roof age affects insurance availability, what underwriters evaluate, when replacement becomes necessary, and the incentives that make upgrading a smart move. Whether you are in Dallas, Texas, or anywhere else in the country, these insights will help you maintain reliable protection without surprises.

Understanding Roof Age as a Key Underwriting Factor

Every home insurance underwriter assesses multiple property characteristics, but few carry the weight of roof age. Why? Roofs serve as the primary barrier against the elements. Over time, exposure to wind, rain, hail, and UV rays causes natural deterioration. Insurers view older roofs as higher-risk because they are statistically more prone to failure during storms or heavy weather events.

Roof age is typically measured from the date of original installation or the last full replacement. It is not just a number on paper – it reflects real-world vulnerability. For homes with roofs 15 years or older, many carriers begin applying additional underwriting guidelines. This common practice helps insurers manage their exposure to large-scale claims, especially in regions prone to severe weather like Texas.

Homeowners often assume their existing policy will automatically cover any damage, but roof age can quietly change the terms. By recognizing this early, you position yourself to make informed decisions rather than reacting to a non-renewal notice.

How Older Roofs (15–20+ Years) Affect Coverage Availability and Premiums

Once a roof reaches the 15- to 20-year mark, the impact on your home insurance becomes noticeable. Here is what typically happens:

- Limited or conditional coverage: Some insurers will only offer actual cash value (ACV) coverage instead of full replacement cost value (RCV) for roofs beyond a certain age.

- Higher premiums: The increased risk translates into elevated rates – often 10–30% more depending on location and roof material.

- Non-renewal risk: Carriers may decline to renew the policy altogether if the roof is deemed too old without documented maintenance or recent replacement.

- Restricted wind/hail coverage: In high-risk areas, older roofs may exclude or limit protection against common perils like hailstorms.

These adjustments are not punitive; they reflect actuarial data showing that roofs older than 15–20 years file claims at significantly higher rates. Yet the situation remains fully manageable. Many homeowners successfully maintain or even improve their coverage by addressing the issue head-on.

Bold truth: Replacing an aging roof often pays for itself through lower premiums and broader protection within just a few years.

What Insurers Look For During Roof Evaluations

Insurance companies do not rely solely on the calendar. Their inspection process examines several key indicators to determine roof condition beyond simple age:

- Material type and quality: Asphalt shingles, metal, tile, or wood shake each have different life expectancies and performance records.

- Maintenance history: Documentation of repairs, cleaning, or preventive treatments can extend perceived roof life.

- Visible signs of wear: Missing granules, curling edges, cracked flashing, or sagging sections signal immediate concern.

- Installation date verification: Underwriters request proof such as permits, invoices, or previous insurance records.

- Local climate exposure: In Dallas and surrounding areas, intense sun and occasional hailstorms accelerate aging, so inspectors weigh regional factors heavily.

Professional roof inspections – ideally performed by licensed contractors – provide the documentation insurers need. A clean bill of health or a recent replacement can dramatically improve your options.

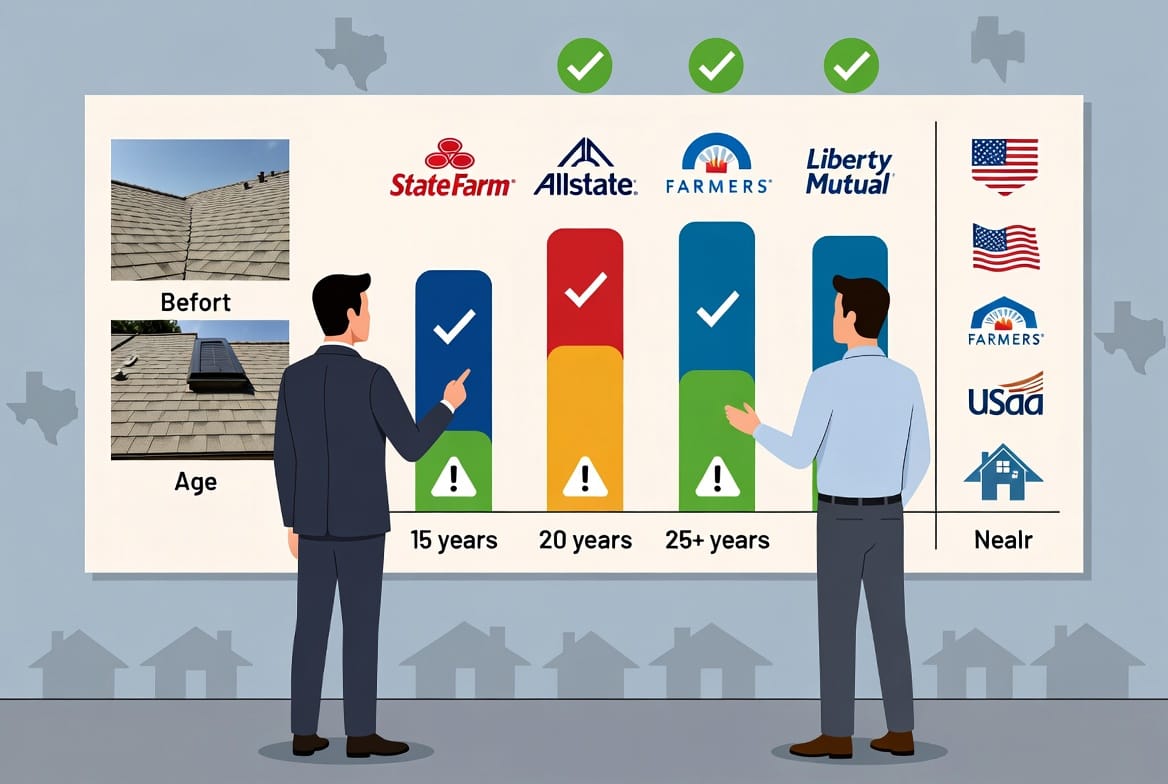

Roof Age Thresholds: Company-Specific Guidelines

Roof age thresholds vary by insurer, but clear patterns emerge across the industry.

Common benchmarks include:

- 15-year threshold: Several national carriers require replacement or ACV-only coverage for roofs 15 years and older.

- 20-year mark: Many standard policies shift terms or mandate upgrades at 20 years.

- 25+ years: Rare full RCV approval; non-renewal becomes highly likely without intervention.

These thresholds are not arbitrary. They stem from decades of claims data and help balance risk for both the insurer and the policyholder. Knowing your carrier’s specific stance allows you to plan accordingly rather than face unexpected changes at renewal time.

Premiums, Coverage Options, and Replacement Incentives

The financial picture looks brighter than many expect. While older roofs can raise premiums, a new roof installation frequently unlocks discounts of 5–15% or more. Insurers reward lower-risk properties with better rates and broader coverage.

Replacement incentives often include:

- Immediate premium reductions upon proof of installation.

- Expanded replacement cost coverage for the new roof (and sometimes the entire home).

- Enhanced wind and hail deductibles or protections in storm-prone regions.

- Eligibility for preferred policy tiers that were previously unavailable.

From an investment standpoint, a quality roof lasts 25–50 years depending on material. When you factor in insurance savings, energy efficiency gains, and increased home value, the return on investment is compelling.

Actual Cash Value vs. Replacement Cost: Critical Distinctions for Older Roofs

One of the most important considerations with an aging roof is the difference between actual cash value (ACV) and replacement cost value (RCV).

- ACV pays the depreciated value of the roof at the time of loss – often far less than the cost to replace it today.

- RCV covers the full expense of a new roof with like-kind materials, minus your deductible.

For roofs older than 15–20 years, many policies automatically convert to ACV. This shift can leave homeowners responsible for thousands of dollars out of pocket after a claim.

Understanding this distinction prevents unpleasant surprises. Proactive replacement restores RCV eligibility and delivers true peace of mind.

Real-World Benefits and Homeowner Experiences

Countless homeowners have transformed potential insurance headaches into opportunities. A Dallas-area family with a 18-year-old roof recently replaced it after their insurer flagged the age during renewal. Within weeks, they secured full RCV coverage and reduced their annual premium by nearly $400. Their new roof also improved energy efficiency and home resale value.

Stories like this repeat nationwide. The common thread? Early action. Waiting until a claim arises or a non-renewal letter arrives limits your options and increases stress.

Practical Steps to Protect Your Coverage

Taking control is straightforward. Follow these proven steps:

- Schedule a professional roof inspection today to establish current condition and age documentation.

- Review your current policy declarations for roof-related coverage details.

- Obtain multiple insurance quotes that specifically address your roof age.

- Consult licensed roofing contractors for replacement estimates and material recommendations.

- Compare total cost of ownership – including future premiums and potential claim payouts.

These actions demonstrate to insurers that you are a responsible homeowner committed to risk reduction.

Why Roof Replacement Delivers Lasting Value

Beyond insurance, a new roof enhances curb appeal, lowers utility bills through better insulation, and strengthens overall structural integrity. In today’s market, buyers and lenders alike view updated roofs as a major plus.

The reassuring reality is that roof age and insurance challenges are solvable. With the right information and timely action, you can secure the coverage your home deserves while enjoying the benefits of a modern, reliable roof.

Conclusion: Take Control of Your Roof and Insurance Today

Roof age need not compromise your home insurance protection. By understanding underwriting standards, recognizing age thresholds, and exploring replacement incentives, you stay ahead of potential issues and protect what matters most – your home and financial security.

Understand how your roof affects your insurance. Our experienced team provides clear guidance tailored to your property, helping you make confident decisions that safeguard your coverage for years to come.

Protect Your Coverage: Roof Review Today