The Rental Car Coverage: Using Your Personal Policy vs. Buying the Rental Company's Insurance

Renting a car opens the door to freedom and adventure, yet it often brings one pressing question at the counter: Should I rely on my existing personal auto policy or pay extra for the rental company’s insurance? This common dilemma leaves many travelers uncertain, weighing potential savings against the risk of unexpected expenses. At first glance, the rental company’s collision damage waiver (CDW) sounds like essential protection. However, your personal auto policy frequently extends coverage to rental vehicles, potentially saving hundreds of dollars per trip.

Know Your Rental Car Coverage – Call Now!

Understanding the nuances empowers you to make confident, cost-effective decisions. This comprehensive guide walks through exactly how your personal coverage works for rentals, its limits, and the precise moments when the rental company’s CDW becomes the smarter choice. With clear insights and practical steps, you can rent with peace of mind—knowing you’re protected without overpaying.

The Everyday Dilemma Drivers Face at the Rental Counter

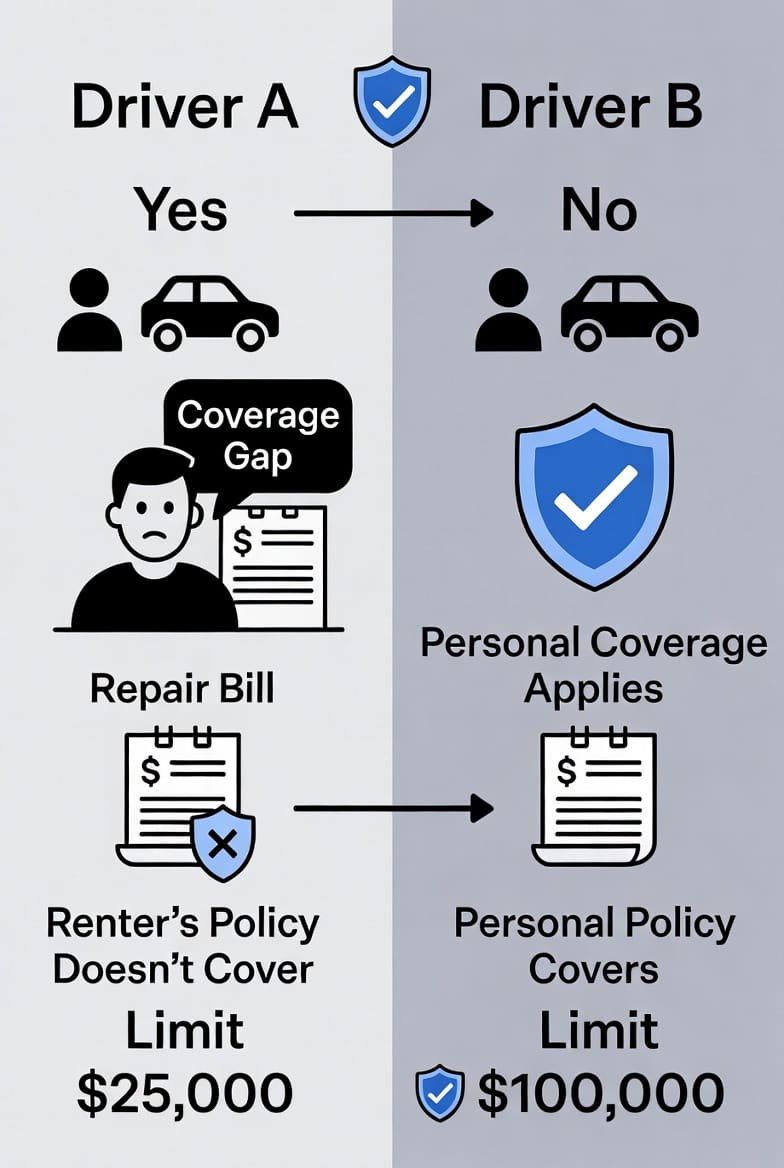

Picture this: you’ve just landed after a long flight, eager to hit the road. The rental agent slides the contract across the counter and asks if you want to add insurance for an extra $25–$45 per day. Many drivers feel pressured to say yes, fearing damage or theft could lead to thousands in out-of-pocket costs. Yet this decision often duplicates coverage you already carry through your personal auto policy.

The core issue stems from limited awareness. Most policyholders never review how their existing insurance applies to temporary vehicles. Rental companies design their offerings to appear comprehensive, but they frequently overlap with—or sit secondary to—your own protections. Recognizing this overlap prevents unnecessary spending while ensuring no dangerous gaps remain. Rest assured, a few minutes of preparation can transform this stressful moment into a straightforward, informed choice.

How Your Personal Auto Policy May Extend to Rental Cars

In the vast majority of cases, your personal auto policy does extend to rental cars when you are listed as a driver on the agreement. This extension typically includes two key components:

- Liability coverage – Protects you if you cause damage or injury to others while driving the rental.

- Physical damage coverage – Your comprehensive and collision portions often apply to the rental vehicle itself, subject to your policy’s deductibles.

Important clarification: Coverage activates only when the rental is for personal use and matches the terms of your policy. For instance, if your policy covers standard sedans and SUVs, it will generally follow you into a similar rental class. This seamless extension means you carry the same limits and protections you already trust for your everyday vehicle.

Many policies treat the rental car as a “temporary substitute” vehicle. As long as the rental period stays within reasonable limits—typically 30 days or less—your insurer steps in exactly as it would for your own car. This built-in benefit provides continuity and eliminates the need to purchase redundant protection in routine domestic rentals.

- Your liability limits travel with you, shielding against lawsuits or medical claims from other parties.

- Comprehensive and collision cover theft, vandalism, or accidents you cause, minus your standard deductible.

- No additional premium is required; the protection is already part of your existing contract.

This extension delivers real value for frequent travelers. Instead of paying daily fees that can exceed $300 on a week-long rental, you simply present your insurance card if needed. The process feels familiar because it is familiar—your policy already knows you.

Coverage Limits and Potential Gaps You Must Know

While the extension sounds straightforward, important limitations exist. Your personal auto policy carries the same restrictions it does on your owned vehicle. Understanding these boundaries prevents unpleasant surprises.

Deductibles still apply. If your collision deductible is $1,000, you will pay that amount out of pocket before coverage kicks in for rental damage. Rental companies, by contrast, may offer zero-deductible options through their CDW.

Coverage applies only to authorized drivers. Anyone behind the wheel must be listed on both the rental agreement and your insurance policy. Additional drivers often require separate approval.

Exclusions can appear. Common exclusions include:

- Business-use rentals

- Certain high-value luxury or exotic vehicles

- International rentals in countries where your policy does not apply

- Off-road or recreational use

Geographic restrictions matter. Most U.S.-based policies cover rentals within the United States and Canada. Mexico and other destinations frequently fall outside standard coverage, requiring separate arrangements.

Policy type influences results. Drivers with liability-only policies receive far less protection than those carrying full comprehensive and collision coverage. In these cases, the rental company’s CDW fills critical gaps.

Rest assured, these limits are not hidden traps—they are simply the natural boundaries of any insurance contract. Reviewing your declaration page before travel reveals exactly what travels with you.

Comparing Personal Policy Protection with Rental Company Insurance

Rental companies offer several add-on products, but the collision damage waiver (CDW)—sometimes called loss damage waiver (LDW)—is the primary option replacing physical damage coverage. Importantly, CDW is not traditional insurance. It is a contractual waiver where the rental company agrees not to pursue you for damage to their vehicle.

Key differences include:

- Personal policy follows your existing limits and deductibles; CDW often provides zero-deductible protection for the rental period.

- CDW covers only the rental vehicle itself; it does not include liability to third parties.

- Personal coverage is usually secondary to any credit-card benefits you may carry, while CDW acts as primary for physical damage.

Many travelers combine options successfully. For example, using your personal auto policy for liability and a credit card’s secondary coverage can create robust protection without purchasing the rental company’s product. However, credit cards typically exclude certain vehicle classes and require you to decline the CDW upfront.

When to Buy the Rental Company’s Collision Damage Waiver (CDW)

Certain situations make the rental company’s CDW the clear, responsible choice. Consider purchasing it when:

- You are renting internationally. Many personal policies exclude or severely limit coverage outside the U.S. and Canada. CDW provides immediate, localized protection.

- You choose a luxury, exotic, or high-value vehicle. Standard policies often cap or exclude vehicles above a certain value or type.

- Your personal policy lacks comprehensive and collision coverage. Liability-only drivers face full financial exposure for any damage to the rental.

- You prefer zero deductible and primary coverage. CDW removes uncertainty and speeds up the claims process at the rental counter.

- You plan off-road or specialty use. These activities frequently void personal policy extensions.

In each scenario, the modest daily fee buys genuine peace of mind rather than duplication. Savvy travelers weigh the daily cost against their personal risk tolerance and policy details before deciding.

Practical Steps to Make the Right Decision Every Time

Follow this simple checklist before your next rental:

- Call your insurance agent or log into your policy portal to confirm rental car extensions.

- Review your declaration page for liability, comprehensive, and collision limits.

- Check any credit cards you plan to use for automatic secondary coverage.

- Compare the daily CDW cost against your deductible and risk level.

- Ask the rental agent to explain exactly what their waiver covers and excludes.

Taking these steps takes only minutes yet prevents costly mistakes. Knowledge truly is the best insurance.

Final Advice: Know Your Coverage Before You Rent

The choice between your personal auto policy and the rental company’s insurance ultimately comes down to understanding your existing protections and matching them to the specifics of your trip. In most domestic rentals with full coverage already in place, your personal policy provides reliable, cost-effective protection. When traveling abroad, driving luxury vehicles, or lacking certain coverages, the CDW offers smart supplemental security.

Know your coverage before you rent. Review your policy, ask questions, and choose the combination that gives you complete confidence on the road. For personalized guidance on how your current auto insurance interacts with rental cars, speak directly with an expert who can review your policy in minutes.

Get Clear Answers on Rental Insurance – Call Today