The Business of Home: Insuring a Home-Based Business Under Your Personal Policy

The explosion of home-based businesses has been one of the most significant economic shifts of the past decade. Whether you’re running an e-commerce store from your spare bedroom, offering consulting services via Zoom, crafting handmade goods in the garage, or managing a growing freelance operation, your home is no longer just where you live—it’s your livelihood.

Don't Risk Your Side Hustle – Get BOP Coverage Today! Call Now

Yet here’s the uncomfortable truth most new business owners discover too late: your standard homeowners policy was never designed to protect a business.

At first glance, it seems like it should. After all, the property is the same roof, the same walls. But insurance policies are built on precise definitions, and the moment you begin operating a business from home, those definitions create dangerous gaps—gaps that can leave you personally exposed to devastating financial loss.

We see it every single week. A talented photographer loses $18,000 in camera equipment to a house fire and learns their homeowners policy caps business property at $2,500. A boutique owner has a customer slip on a package left by the front door and faces a liability claim their personal policy explicitly excludes. A software developer working from home discovers their $40,000 laptop and custom server setup are barely covered when a power surge hits.

These aren’t hypotheticals. These are real people who thought they were protected—until they weren’t.

The Coverage Gap Almost No One Talks About

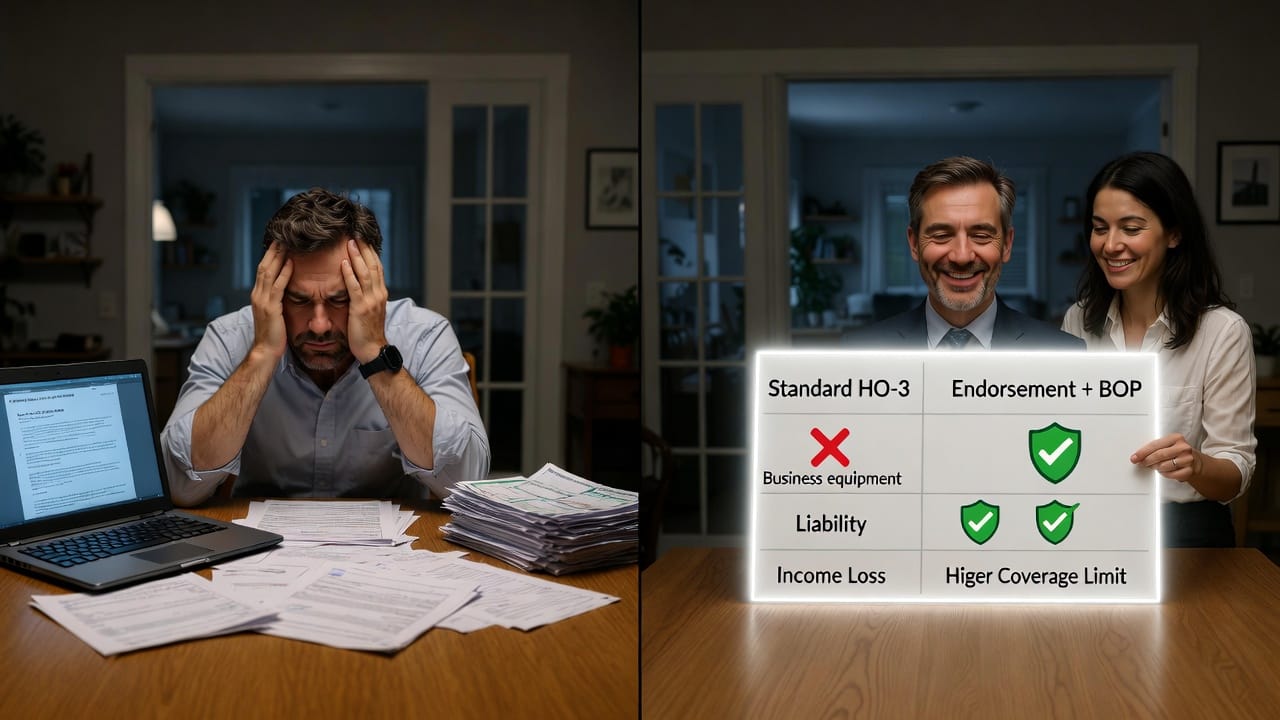

Most homeowners policies (the common HO-3 form) include very limited—or in many cases, zero—coverage for business-related activities. The insurance industry draws a clear line between personal use and commercial use, and once you cross that line, standard coverage shrinks dramatically.

Here’s what typically happens:

- Business personal property on the premises is often limited to $2,500–$10,000 total, regardless of actual value.

- Business property off-premises (samples at a trade show, inventory in your car) may be covered for as little as $500.

- Business liability is usually completely excluded. If a client visits your home and gets injured, or if you’re sued for a product defect, your homeowners policy steps back.

- Business income and extra expense (lost revenue while you rebuild after a covered loss) is rarely included at all.

The result? You could lose everything you’ve built in a single incident that would have been fully covered if the same property and activities existed in a traditional commercial space.

This is not a flaw in the system. It’s by design. Homeowners insurance protects your residence as a personal asset. The moment it becomes a revenue-generating operation, different rules apply.

When “Incidental” Coverage Is Enough—And When It Isn’t

Many carriers offer an Incidental Business Pursuits Endorsement (sometimes called a Home Business Endorsement) that can be added to your existing homeowners policy. These endorsements are designed for side hustles and low-risk operations—think a part-time Etsy seller, a weekend consultant, or someone who occasionally sees clients at home.

What these endorsements typically provide:

- Increased limits on business property (often $10,000–$25,000)

- Some liability coverage for business activities (usually $300,000–$1 million)

- Limited coverage for business interruption

They are affordable—often just $50–$150 per year—and can be a smart solution for many home-based entrepreneurs.

But here’s the critical distinction: These endorsements have strict eligibility requirements and coverage limitations. If your business:

- Generates more than 20–30% of your household income

- Involves regular client traffic (more than 2–3 visitors per week)

- Stocks significant inventory

- Requires specialized equipment valued over $25,000

- Involves any food preparation, child care, or professional services with higher risk

…then an endorsement likely won’t be enough.

The Business Owners Policy (BOP): Your True Safety Net

When your home-based business has outgrown endorsement territory, the gold standard is a Business Owners Policy, or BOP.

A BOP is not just “more coverage.” It’s a completely different type of policy built specifically for small businesses. It combines:

- Commercial property insurance (your inventory, equipment, furniture, computers—at actual cash value or replacement cost)

- General liability insurance (protects against customer injuries, advertising injury, product liability)

- Business income and extra expense (pays you while you’re unable to operate after a covered loss)

- Optional add-ons like cyber liability, professional liability (E&O), and workers’ compensation

The advantages are substantial:

- Limits that actually match the value of your business (think $100,000, $250,000, or more in property coverage)

- True liability protection—even when clients come to your home

- Coverage for business interruption that can keep your income flowing during recovery

- Often includes valuable extensions like debris removal, pollutant cleanup, and utility service interruption

Most importantly: A BOP treats your home-based business with the same seriousness as a traditional storefront. Your insurer becomes your partner in protecting the enterprise you’ve built—not an afterthought tacked onto your personal homeowners policy.

How to Know Which Path Is Right for You

The question we ask every home-based business owner is simple but revealing:

“If your home burned down tomorrow, would your current insurance allow you to rebuild your business?”

If the answer is uncertain, it’s time to take a closer look.

Here are the key questions that determine whether you need more than an endorsement:

- Do clients or vendors regularly visit your home?

- Is your business your primary or significant source of income?

- Do you maintain more than $10,000–$15,000 in business equipment or inventory?

- Do you sell physical products that could cause harm (beauty products, supplements, children’s items)?

- Are you in a professional service that carries errors-and-omissions risk (consulting, financial advising, coaching)?

If you answered “yes” to two or more of these, a standalone BOP or a hybrid approach (endorsement plus separate liability) is almost certainly the smarter, safer choice.

The Cost of Being Underinsured vs. The Peace of Mind of Being Properly Covered

Many business owners hesitate because they worry about cost. Here’s what we tell them:

A properly structured BOP for a typical home-based business often costs between $500 and $1,800 per year—roughly the price of a nice dinner out each month. Compare that to the potential loss of $50,000 in uninsured equipment, a $100,000 liability judgment, or months of lost revenue.

The math is simple. The small premium you pay today prevents the catastrophic financial hit tomorrow.

And the best part? Many carriers now offer flexible BOPs specifically designed for home-based businesses, with no requirement for a separate commercial address. Your home qualifies.

Real Protection Starts With a Real Conversation

The most dangerous assumption you can make is that “it’ll never happen to me” or “my homeowners policy will handle it.”

We’ve helped hundreds of home-based business owners close these coverage gaps, and the relief we hear in their voices is always the same: “I had no idea how exposed I was.”

Don’t wait for a claim to find out.

Whether you’re just starting your side hustle or running a thriving full-time operation from home, the right insurance structure exists for you—and it’s simpler to put in place than you might think.

Let one of our home-based business insurance specialists review your current policy and show you exactly where you stand. In most cases, we can present options within 24 hours.

Your business deserves the same level of protection you’ve worked so hard to build.

Protect the business of home—before you need to.

Close the Home Business Coverage Gap – Free Review, Call Today